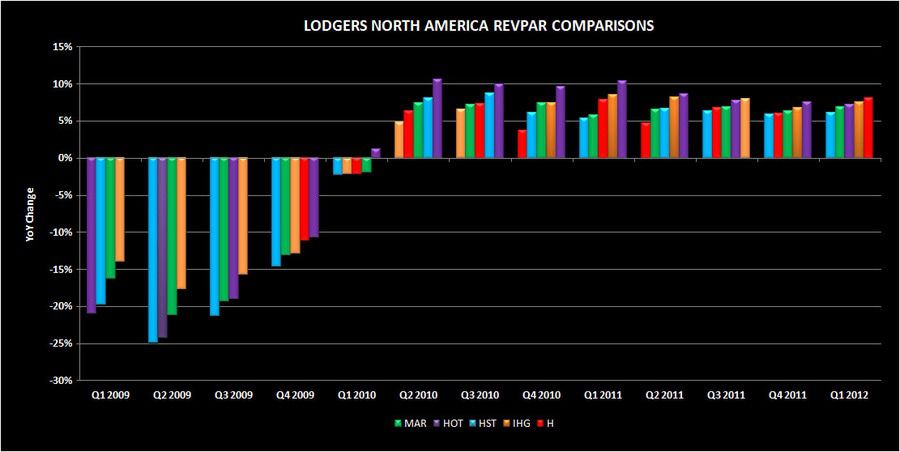

- Since Q1 2011, IHG and HOT have been leading the pack in North America REVPAR. IHG may have benefited from a reverse FX impact.

- Hyatt is looking like they are finally seeing the fruits of their renovation programs

- Marriott is a laggard due to the higher concentration of group business which lags transient – they also have bigger boxes and an out-sized exposure to D.C.

- The standard deviation among the lodgers' performance in North America has narrowed considerably