We added UA back into the Hedgeye Virtual Portfolio with the stock back down to its TRADE line of support on a downgrade this morning.

Here’s how we’re thinking about it on different durations...

With the stock up 100% since last August, we hardly think that getting into UA now is a ‘big call’. But in this market – one where our Macro team went to 100% cash and is thinking that the chances of a market crash are going up – we’ll look to be tactical around great growth stories like UA where the near-term qualitative framework marries up with the quant set-up.

Here Are Some Considerations on UA:

TAIL (3-years or Less): We think that UA will put up $3bn in revenue by 2014 – an impressive run given that it is coming off of a print of just under $1.5bn in 2011. That incremental top line breaks out as follows. a) $500mm in core apparel growth, b) $300mm in incremental footwear, c) $300mm in international apparel, d) $250mm in women’s apparel, e) $125mm in accessories (having brought hats and bags licenses in house). Our confidence here is greater than it is with most other companies given that UA clearly has invested (and will continue to invest) the capital in the right places to get the job done. One of the key points we look at is that it’s sitting at an EBIT margin of only 11% -- when it could be printing a margin number with a 2 if it wanted (but would otherwise jeopardize forward growth potential). It’s tough for us to find any name out there in retail -- -sans LULU – where we can build a consistent annual EBIT growth model in the 25-30% range.

TREND (3 Months or More): A key consideration is that we’re now anniversarying a period last year where inventories were up an average of 70% as UA battled through problems with it’s supply chain. Even with growth humming in the 30-40% range, 70% inventory growth was not exactly a confidence builder for anyone building a financial model. Since these problems, UA has made many changes in its management ranks, created new positions, and made key external hires to get its fulfillment to where it needs to be. The reality is that this happens to just about every company going through different stages of maturation. UA is no different. Where it is different is the speed at which it appears to be fixing the problems. The Punchline is that this is gross margin bullish for UA in the coming 3 quarters. Lastly, one interesting angle here is that UA has less than 5% of sales coming from outside the US. With a strengthening dollar, this creates a situation where its failure has actually turned into a near-term benefit relative to competitors that operate globally and need to translate profits to US$. That ‘benefit’ should wane in 2013 when we start to see the benefit of the new organization UA has put in place in Europe.

TRADE (3-Weeks or Less): There are some mixed message here.

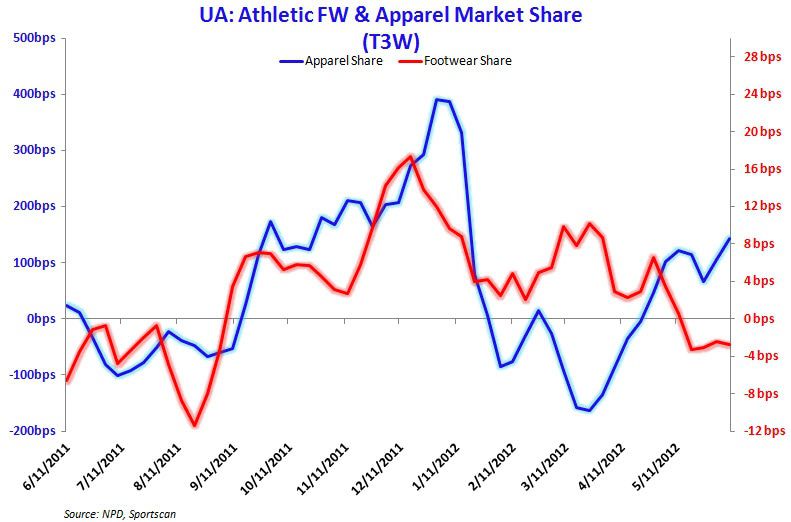

- On one hand, business appears stable, with the year/year change in apparel market share continuing on the uptrend. In addition, the Hedgeye Sentiment Monitor is sitting near the lowest levels in a year, and the company is about to execute a stock split. While we all know that this should not matter, the reality is that there are some people that will always think that a $50 stock is half as expensive as a $100 stock.

- On the flipside, footwear continues to do a whole lot of nothing. That supports the ‘where could we be wrong’ part of our longer-term call, is the potential for a capital infusion needed (hence lower margins) to amp up the footwear business to attain our revenue numbers. The marketing spend to support UA’s new Spine technology launch starting in July is expected to be its greatest yet after which the company then introduces its new basketball silhouette in time for back-to-school.

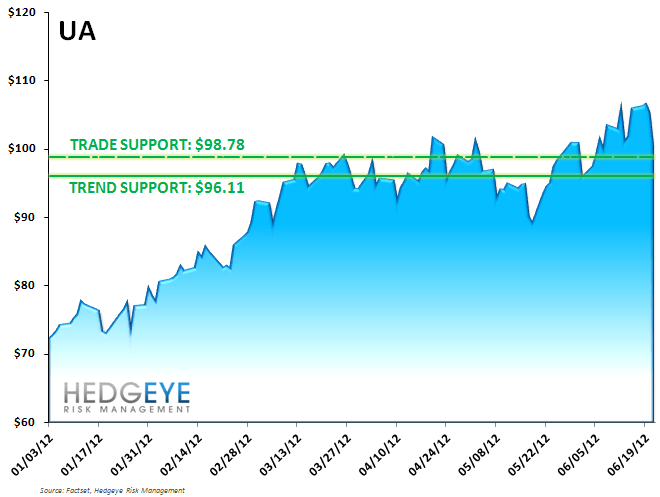

- The bottom line is that the stock is back down to the low-end of the trading range with our TRADE factors lending clear support at $98.78.

Just a quick point on valuation – something we think needs a bit of context with UA. By most metrics – pe, EBITDA, EV/Sales, UA is just flat out expensive. But if you went by those metrics over the past 3-years, you’d pretty much have been wrong on both the long and short side almost every time. We think the better metric is EV/Total Addressable Market. For UA, that equates to about 0.15x based on our math. That makes it the cheapest name around. LULU is 0.33x, RL 0.45x, NKE 0.60x. Will that matter on a day where the consensus freaks out because apparel sales miss by 2%? No. But that’s when we think we’ll be able to step in and make the most money on one of the best names in the space.

UA’s Apparel Market Share Continues to Rebound…Footwear Not So Much

HEDGEYE RISK MANAGEMENT LEVELS:

HEDGEYE SENTIMENT MONITOR HAS A BULLISH SETUP: