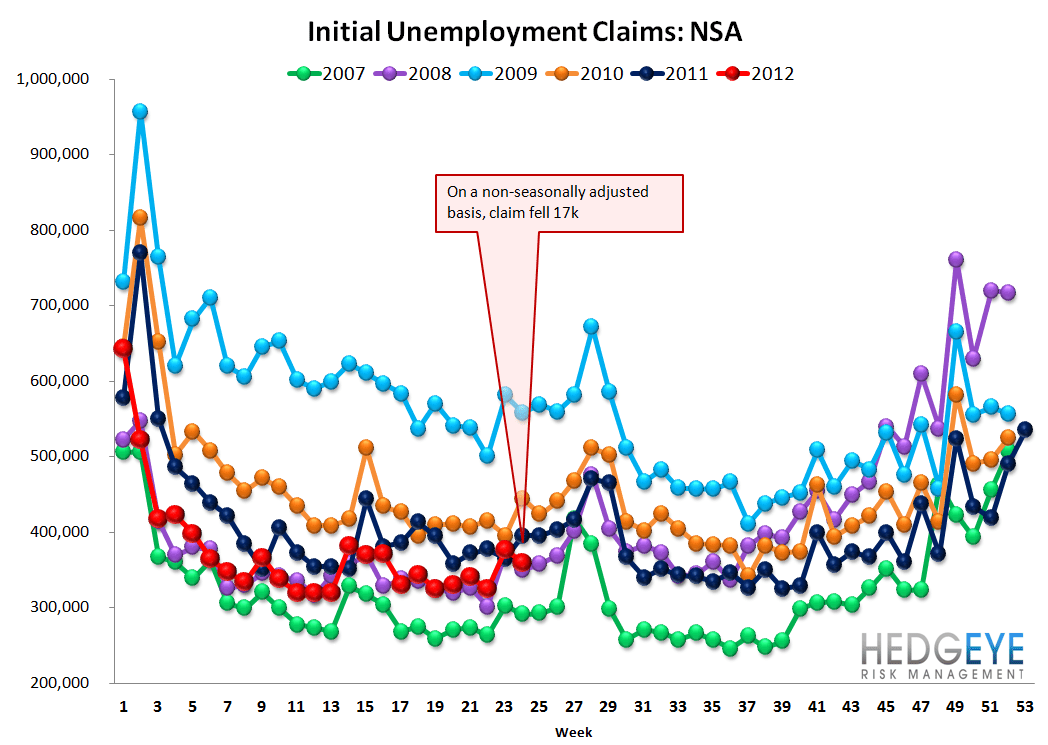

Claims Are Steadily, Predictably Moving Higher

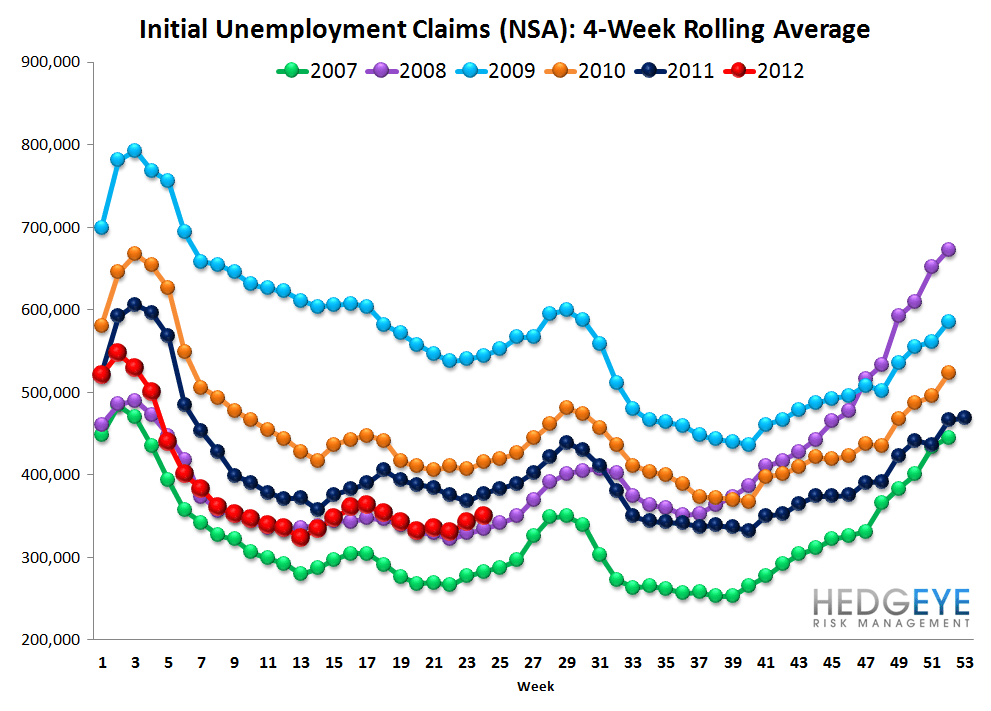

Initial Claims rose by 1k to 387k, As usual, the prior weeks print was upwardly revised by 3k. Incorporating this 3k upward revision to the prior week's data, claims were lower by 2k. Rolling claims also increased, rising 3.5k to 386k, a new YTD high. For reference, the last time rolling claims were higher was December 10, 2011 at 388k. On a non-seasonally adjusted basis, claims fell 17k to 360k.

Fundamental Deterioration on Top of Seasonal Distortion

Rolling NSA claims, our way of cutting through the seasonal distortions taking place in the data, were better this week by 8% YoY, which is less good than the 10% and 9% YoY rates of improvement we've seen over the last few months, suggesting that beyond the seasonal distortions there is some fundamental softening taking place as well.

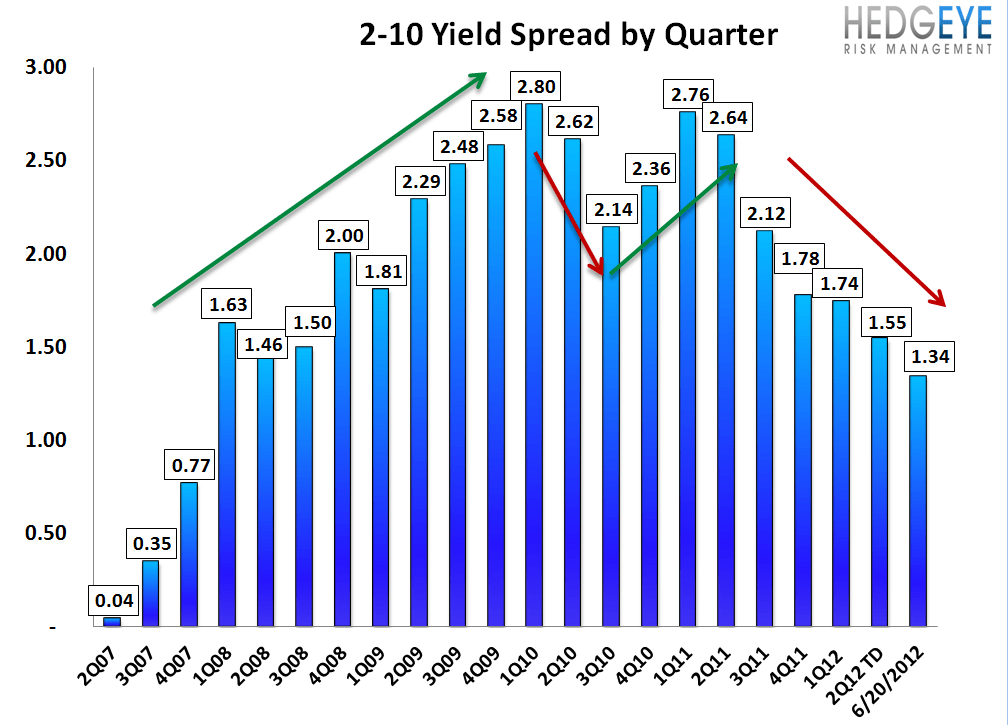

Operation Twist Extended

The 2-10 spread widened 5 bps versus last week to 134 bps as of yesterday. The ten-year bond yield increased 6 bps to 165 bps. While there was some relief this week, if spreads continue to sit a these low levels, the 3Q12 sequential change will rival what we saw in 3Q11 when banks across the board saw their margins flatten. The extension of Operation Twist yesterday will continue to put pressure on the long end of the curve.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.