TODAY’S S&P 500 SET-UP – June 21, 2012

As we look at today’s set up for the S&P 500, the range is 29 points or -1.67% downside to 1333 and 0.47% upside to 1362.

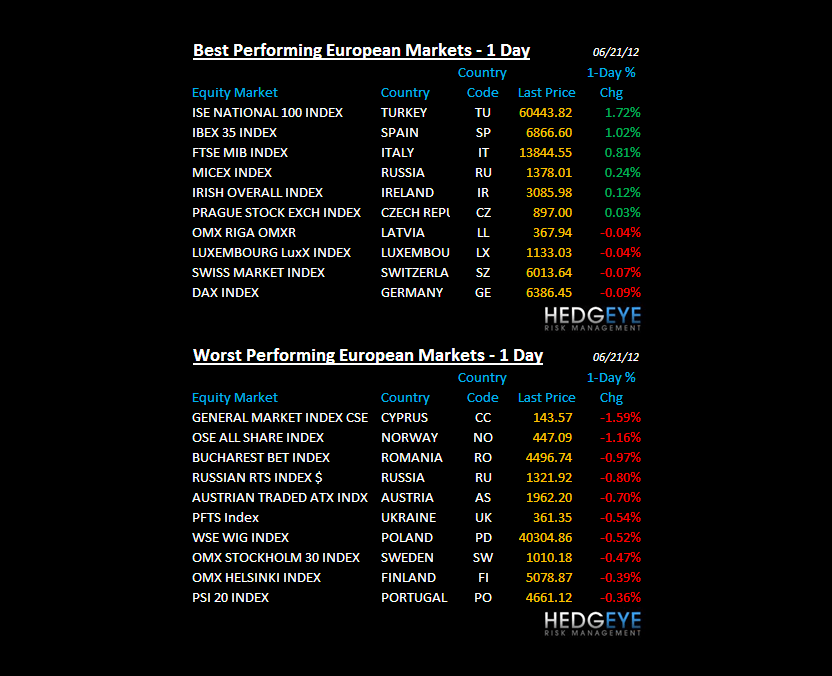

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/20 NYSE 10

- Down from the prior day’s trading of 2074

- VOLUME: on 6/20 NYSE 751.15

- Decrease versus prior day’s trading of -2.71%

- VIX: as of 6/20 was at 17.24

- Decrease versus most recent day’s trading of -6.20%

- Year-to-date decrease of -26.32%

- SPX PUT/CALL RATIO: as of 6/20 closed at 1.90

- Up from the day prior at 1.54

CREDIT/ECONOMIC MARKET LOOK:

2YR – this came up last night; we talked about it as the leading indicator for the US Fiscal Cliff; this morning, the 2yr popped above our intermediate-term TREND line of resistance of 0.30%. This will be very interesting to watch as US GDP Growth continues to slow (the denominator in deficit/GDP drives the #1 fundamental risk ratio higher).

- TED SPREAD: as of this morning 39

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.64

- Decrease from prior day’s trading at 1.66

- YIELD CURVE: as of this morning 1.34

- Down from prior day’s trading at 1.35

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30 am: Initial Jobless Claims, June 16, est. 383k (prior 386K)

- 8:30 am: Continuing Claims, June 9, est. 3278k (prior 3278k)

- 9:45 am: Bloomberg Consumer Comfort, June 17 (prior -36.4)

- 9:45 am: Bloomberg Economic Expectations, June (prior -1)

- 10am: Philadelphia Fed, June, est. 0.0 (prior -5.8)

- 10am: Existing Home Sales, May, est. 4.57m (prior 4.62m)

- 10am: House Price Index M/m, April, 0.4% (prior 1.8%)

- 10am: Leading Indicators, May, 0.1% (prior -0.1%)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural gas change

- 11am: Fed to purchase $4.25b-$5.25b notes in 6/30/2018-5/15/2020 range

- 1pm: U.S. to sell $7b 30-yr TIPS (reopening)

GOVERNMENT:

- Supreme Court issues decisions today

- CFTC holds open meeting on regulation of swaps, derivatives

- House, Senate in session

- Senate Banking hears from SEC Chairman Schapiro on proposals to overhaul money market mutual funds, 10am

- House Financial Services panel holds hearing on supervision of money services businesses, 9:30am

WHAT TO WATCH:

- Samaras to name new Greek govt., Vassilios Rapanos, chairman of National Bank of Greece, to become finance minister

- WTI crude oil falls below $80 for first time since Oct.

- Spain 2014 bonds avg yield 4.706% vs 2.069% in March sale

- Sales of previously owned U.S. homes probably fell in May

- U.K. retail sales rose 1.4%, beating est. 1.2%

- SEC said to depose SAC’s Cohen in insider-trading probe

- Philip Morris cuts 2012 EPS forecast on currency swings

- Onyx wins FDA advisory panel backing for blood-cancer drug

- Invensys says it’s no longer in any discussions after approach by Emerson

- BlueMountain said to help unwind JPMorgan’s losing trades

- MSCI puts Greece on review for potential reclassification as Emerging Market

- China manufacturing may shrink for an eighth month in June

- EMA expected to make drug-safety/approval decisions today/tmw

- UPS to begin offer in $6.5b TNT Express takeover tomorrow

- New Zealand GDP rises 1.1% Q/q, fastest in five years

- Euro-area finance ministers meet in Luxembourg to discuss financial transaction and energy taxes and the debt crisis

EARNINGS:

- Rite Aid (RAD) 7am, $(0.04)

- ConAgra Foods (CAG) 7:30am, $0.50

- CarMax (KMX) 7:35am, $0.53

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG

OIL – is it a bird, a plane, or demand? Or is it the Dollar? Or supply? The crash in oil (WTIC -26% from $108) is highly correlated to the USD. Currently, on a 2-mth duration, USD/WTIC = -0.94. Get the Dollar right, you get oil right. Immediate-term TRADE oversold lines for WTIC and Brent at $80.57 and $91.20. Sell all bounces. It’s a Bernanke Bubble.

- Founder of $125 Billion Gold ETPs Stymied on Copper: Commodities

- Oil Drops Below $80 to Eight-Month Low on U.S. Supply, Europe

- Commodities Slump to 19-Month Low as U.S. Growth Outlook Weakens

- Copper Reaches One-Week Low on China Index and Fed Forecast Cut

- Gold Drops for Third Day as Fed Opts to Extend Operation Twist

- Sugar Falls as Rains May Ease in Top Grower Brazil; Coffee Drops

- Corn Drops as Slowing U.S. Economic Growth May Cut Ethanol Use

- Marcellus Gas Cuts Price Premiums to Decade Lows: Energy Markets

- Gazprom Bond Sale Biggest Since ’09 as Yields Dip: Russia Credit

- China Looks to Build Rare-Earths Reserves to Stabilize Prices

- Coffee Harvest in India Seen Falling From Record on Dry Weather

- Subsidies Boost Ambani With Record Diesel Sales: Corporate India

- China’s Hungry Pigs Lead to Surfeit of Soy Oil: Chart of the Day

- Crude Drops Below $80 to Eight-Month Low

- Bauxite, Nickel-Ore Imports by China Climb to Record in May

- Palm Oil Declines From Three-Week High on Fed’s Operation Twist

- Chinese Seek Duty on U.S. Silicon Expanding Trade Fight: Energy

CURRENCIES

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – down another -1.4% last night after another bad PMI number and ongoing #GrowthSlowing signals on the East side of the world. Germany’s PMI print of 44.7 for June reflects this global slowing; so does the long end of the UST curve. It’s only a matter of time before Equities mean revert lower.

MIDDLE EAST

The Hedgeye Macro Team