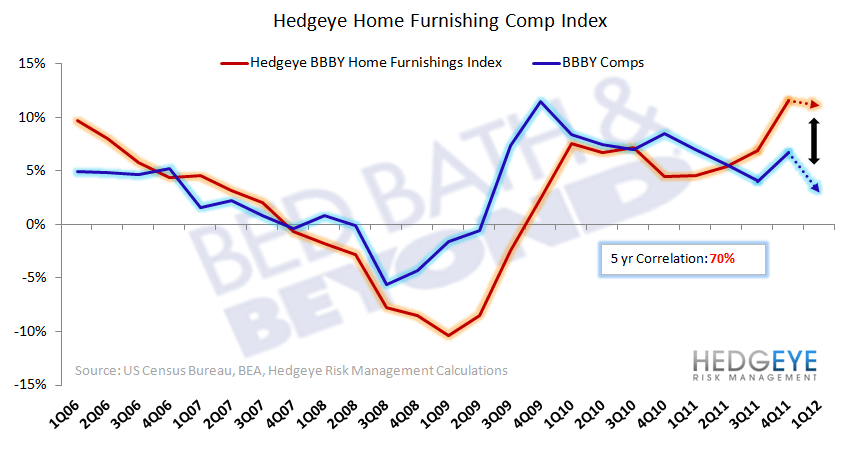

BBBY showed its TAIL risk after the close with comps decelerating nearly 400bps sequentially, producing the greatest negative deviation relative to our home furnishings index we’ve seen since its inception. On top of 2 non-core acquisitions over a 1 month time period this is a complete validation of every concern we’ve had for BBBY.

Our Home furnishings index, which we use as a leading indicator for BBBY comps, implied a +6.5% comp. The +3% print was simply a massive miss. Our model is based in large part on Personal Consumption and Retail Sales for different home goods products. It’s proven to be extremely accurate over time, with a 0.75x correlation, and if you ex-out the period when it was putting Linens ‘n Things out of business (and posted outsized comps) the correlation is closer to 0.90x. Directionally, something went very wrong this quarter. Yes, there’s definitely the on-line share loss factor , but it’s also no mistake that this is happening in conjunction with BBBY’s headquarter move. The margin of error there is too great to ignore – especially with the company integrating two acquisitions.

We’ve remained negative on the intermediate term TREND and long term TAIL and are reiterating our stance. Consider the Following:

- After adjusting for the $0.06 tax benefit, BBBY 1Q12 EPS came in a penny below expectations driven by light revenue growth (+5.1% vs. +6.4E) and weak gross margins (-65bps vs. -25E)

- The Gross Margin decline in the quarter was driven by both an increase in coupon redemptions & redemption amount as well as the continued shift to lower margin product categories. In light of BBBY citing AUR as a driver of the +3% comps, the shift to lower margin product categories suggests the pricing mix may also be shifting upwards, driving a greater coupon redemption dollar amount. Notably, per our in store AMZN/BBBY sku overlap analysis (see chart below), AMZN has 10-15% lower prices in higher ASP product categories suggesting a shift to higher price point categories could keep BBBY at risk of additional couponing or online attrition pressuring margins further.

- The sales to inventory spread declined 5 points sequentially to -1% in Q1 after having popped into positive territory last quarter. This creates a somewhat bearish gross margin setup over the intermediate term TREND especially given the incremental coupon use at a time when PIR highlighted a balance in full price and promotional selling with no major negative change in the discounting environment relative to last year.

- BBBY said that it remains focused on enhancing its omni channel experience and expects its new 800,000 square foot e-commerce fulfillment center to be operational in 2H12. Today, e-commerce accounts for ~1% of total sales and has been declining over the past 3 years. Customer demographics continue to be a key issue here. 65% of BBBY’s current online consumers are above the age of 35. Industry data suggests that BBBY’s exposure to the 55 & up demographic increased nearly 300bps in 2011 vs. 2010 to 26% putting BBBY 9th in terms of the most exposed to the older demographic relative to the 95 companies we’ve analyzed. It is nearly impossible for e-commerce to really gain traction without investing and while not a direct comp, WSM’s omni channel model currently boasts e-commerce nearing 40% of sales.

- Although BBBY reiterated its full year EPS growth of HSD-LDD and comp of +2-4%, operating margins are now expected to be down vs. flat to down slightly previously. Despite the net negative change in outlook on the margin, this still seems aggressive. At a minimum, it seems like the time where we can all give them a free pass on beating guidance is gone.

- BBBY has leveraged operating expenses nearly 200bps over each of the last 3 years with operating expenses up only ~1% in Q1 and down 2.2% on a per square foot basis. BBBY had originally guided advertising activities to remain flat in F12 however if BBBY expects a reacceleration in the business and traction online, they will have to spend to get it.

We remain bearish here – not because of what happened, but because of what the quarter and recent strategic actions signify. The company’s model remains exposed to the online threat (with a 93% direct sku overlap with amazon.com) with its competitive advantage remaining in its in-store experience. Though it seems demand is slowing (per our Home Furnishings Index below) BBBY’s current share is slipping for the first time in many years -- which will require incremental investments back into the business following 3 years of opex leverage. Not good with BBBY sitting at peak ~17% operating margins. We remain negative on the long term TAIL call here.

Matt Darula

Analyst