Darden reports 4QFY12 earnings on Friday the 22nd of June at 7:00 am. The earnings call begins at 08:30 am. We have adopted a stance of “casual dining caution” since April 20th as sales trends and underlying macro fundamentals for the casual dining group seemed to be softening. Darden's stock has long been considered the bellwether of casual dining but, beyond our concerns about the broader group’s outlook, we believe there are additional company-specific factors working against Darden as we move into FY2013. We believe that besides initial FY13 guidance, commentary on Olive Garden – specifically traffic trends and additional guidance on the remodel program – will be the primary focus for investors when the earnings release hits the tape. We would not be buyers of the stock ahead of earnings.

Consensus estimates for 4QFY12 have declined by roughly $0.02 over the past month but expectations for FY13 have remained unchanged, suggesting that the Street expects the company to push through the recent slowdown in sales. Any deviation from this narrative, on the part of the company, will likely cause the stock to sell off. Excluding one-time items that the Street may not traditionally pay for (like cutting G&A), there is still a chance the company misses $1.15 4QFY12 EPS expectations. Overall, we believe that the company is in "investment mode", attempting to bolster its appeal to customers at all of its concepts.

Casual Dining Backdrop

Below, we show the Hedgeye Casual Dining Index versus Initial Claims (inverted) and also Darden versus Initial Claims (on the right). The soft employment backdrop is negative for both casual dining and Darden; we expect management to allude to this during the conference call.

3QFY12 Recap and Look Ahead

Macro: Management referred to the "choppy" environment during the earnings call on March 23rd. At that time, according to the company, improving employment was being offset by the impact of rising gas prices. Given that employment trends have softened since March, and gas prices peaked in early April, it will be interesting to hear which of these management weighs more heavily in its outlook for the rest of the calendar year. In late April, CFO Branford Richmond, speaking at a conference, stated that “that’s [the broader industry] really driven … by job creation.” We expect the tone to be negative if/when management touches on the macro environment as the employment picture has deteriorated since the most recently reported quarter.

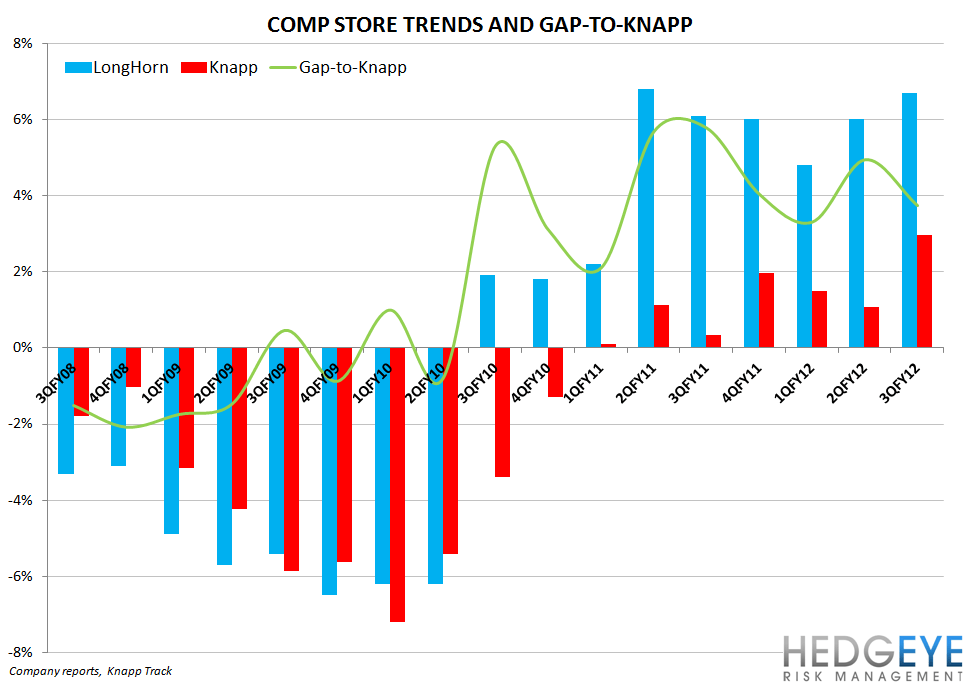

Olive Garden: Weak traffic trends at Olive Garden are a concern for investors and will be one of the first numbers we look for when the press release hits on Friday morning. Although promotions helped Olive Garden to narrow the Gap-to-Knapp during 3QFY12, we expect the sequentially weakening industry sales (Knapp Track) to weigh on Olive Garden trends.

According to Consensus Metrix, the Street is anticipating Olive Garden’s 4QFY12 comps to come in at 0.48%, which would imply a two-year average trend of 0.2% versus 1.0% in 3QFY12. While this two-year average decline would be a negative, we estimate that 0.48% would imply a sequential improvement in the Gap-to-Knapp metric: we estimate that it would imply +0.8% versus Knapp Track. Olive Garden has underperformed Knapp for six consecutive quarters and, while the gap has been closing, we do not think that the pace at which the gap narrowed during 3QFY12 continued into 4Q. The promotions offered during 3QFY12 at Olive Garden compared very favorably to the 3QFY11 promotional offerings which performed poorly. We think that the Street is overly optimistic in expecting 0.48% same-restaurant sales growth at Olive Garden in 4QFY12.

Red Lobster: Red Lobster posted a 6% same-restaurant sales growth number for 3QFY12, as preannounced, which benefitted by 480 basis points due to an earlier start to Lent 2012 versus 2011. According to Consensus Metrix, the Street is expecting 1.28% same-restaurant sales growth in 4QFY12 as the Lent benefit reverses. This implies a two-year average decline in comps of 60 basis points and sequential decline, we estimate, versus Knapp Track. During the most recent earnings call, management stated that “Red Lobster's fourth quarter same-restaurant sales will be adversely affected because of the shift forward in Lent and Lobsterfest.”

LongHorn Steakhouse: LongHorn remains a key focus for the company; the chain has been growing comps in the mid-single digit range for six consecutive quarters and new LongHorn units continue to exceed sales and earnings targets set by the company. LongHorn is likely to continue to perform strongly. While the chain is important for the longer-term TAIL story, we see Olive Garden and Red Lobster as being more important for the stocks near-term TRADE and intermediate term TREND price action.

A note on weather: Looking at top line trends for Darden’s restaurants versus 3QFY12, we see a risk that the street underestimates the boost that weather provided to the company during the winter months. As we wrote on 2/22 in a post titled “WINTER WONDERLAND”, the state of Texas was heavily impacted by the adverse weather conditions for an entire week in February in 2011. A year later, there was little-to-no snow in the Southern Region of the United States, according to data from the National Operational Hydrologic Remote Sensing Center. According to a New York Times article of 2/4/11 titled, “Snow and Ice Paralyze Texas From Rio Grande to Oklahoma Border”, a snow storm on that morning hit much of Texas and created chaos for travelers traveling ahead of the Superbowl that Sunday. During a conference on 4/24/12, Darden’s management team included Texas as a state that does not "traditionally see much of a weather impact", the implication being that the market there had improved its sales during 3QFY12 without any significant boost from weather, as occurred in the North East during January and February of 2012. We think that the weather data and media reports suggest otherwise. In light of the dramatic year-over-year change in weather conditions within Texas (a state with 148 of Darden’s 1,849 restaurants), we think that 3QFY12 comps may have been helped aided by weather more than management has implied.

Howard Penney

Managing Director

Rory Green

Analyst