TODAY’S S&P 500 SET-UP – June 19, 2012

As we look at today’s set up for the S&P 500, the range is 24 points or -1.55% downside to 1324 and 0.24% upside to 1348.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/18 NYSE 539

- Down from the prior day’s trading of 1149

- VOLUME: on 6/18 NYSE 707.28

- Decrease versus prior day’s trading of -53.26%

- VIX: as of 6/18 was at 18.32

- Decrease versus most recent day’s trading of -13.22%

- Year-to-date decrease of -21.71%

- SPX PUT/CALL RATIO: as of 6/18 closed at 1.51

- Down from the day prior at 1.72

CREDIT/ECONOMIC MARKET LOOK:

TREASURIES – you can whip the manic equity guy around on no-volume (down -38% volume study yesterday was awful), but you can’t budge bonds. 10yr down again to 1.58% this morning and the Yield Spread is about to snap +130 wide again. Not good for the Financials – it wasn’t yesterday either.

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.57

- Unchanged from prior day’s trading

- YIELD CURVE: as of this morning 1.29

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates):

- 7:45am/8:55am: ICSC/Redbook weekly retail sales

- 8:30am: Housing Starts, May, est. 721k (prior 717k)

- 8:30am: Building Permits, May, est. 730k (prior 723k)

- 10am: JOLTs Job Openings, April, est. 3685 (prior 3737)

- 11am: Fed to buy $1.5b-$2b notes in 8/15/2018-2/15/2031 range

- 11:30 am: U.S. to sell 4-week bills

- 4:30pm: API inventories

- FOMC Meeting, Day 1

GOVERNMENT:

- U.S. Federal Open Market Committee policy makers begin two- day meeting in Washington to decide on interest rates, 10am

- Mexican President and G-20 summit host Felipe Calderon may hold late-afternoon press conference on meeting’s final day

- House, Senate in session

- Joint Economic Committee holds hearing on economic impact of ending funding for certain government data, 2:30pm

- Senate Finance hears from former White House Budget Director Alice Rivlin on looming fiscal crisis, 10am

- CFTC Commissioner Bart Chilton delivers keynote address at Mutual Fund Directors Forum policy conference, 7pm

WHAT TO WATCH:

- JPMorgan CEO Jamie Dimon testifies at House cmte hearing

- U.S. Federal Open Market Committee begins two-day meeting

- Greek parties to form group to renegotiate bailout terms; borrowing costs fall at 91-day bill auction

- Microsoft unveils Surface tablet computer, taking on IPad

- Oracle rises after earnings beat estimates on software sales

- German investor confidence dropped more than forecast in June

- G-20 leaders hold a 2nd day of meetings in Mexico, to urge euro-area govts to take all steps to protect currency union

- China leads 12 nations helping boost IMF’s firewall to $456b

- CBS billboard unit worth a look: Clear Channel Outdoor CEO

- Insight said to top $25.50/shr offer to buy Quest Software

- Danone cuts profitability goal on southern Europe, costs

- France plans 3% div. tax to be paid by cos., Les Echos says

- China said to order checks on maturing bonds to avoid defaults

EARNINGS:

- FedEx (FDX) 7:30am, $1.92

- John Wiley & Sons (JW/A) 8am, $0.73

- Jefferies Group (JEF) 8am, $0.27

- Discover Financial Services (DFS) 8:30am, $1.00

- Barnes & Noble (BKS) 8:30am, $(0.91)

- Jabil Circuit (JBL) 4:02pm, $0.64

- Adobe Systems (ADBE) 4:05pm, $0.59

- La-Z-Boy (LZB) 4:05pm, $0.26

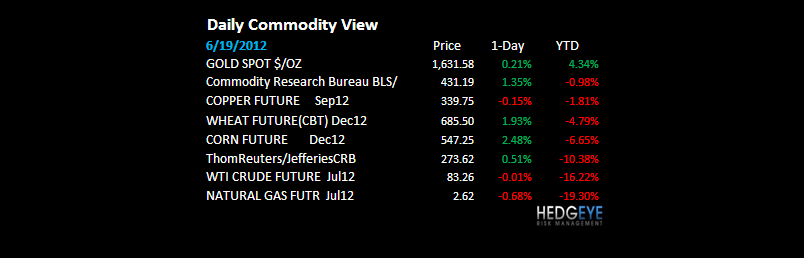

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

OIL - both WTIC and Brent act horribly ahead of what is supposed to be another Bernanke Bailout tomorrow; consensus better watch what they are begging for here as Dr Copper also disagrees (down -0.4% this morning and still in a Bearish Formation); Gold has had a good move front-running Fed expectations, but now bumps up against a wall of resistance at $1642.

- Rubber Glut Extends Bear Market as Bridgestone Wins: Commodities

- Corn Set for Biggest Two-Day Advance Since April on U.S. Weather

- Robusta Coffee Declines as Slowing Economies May Erode Demand

- Oil Declines for a Second Day on Europe Concern, Iranian Talks

- Copper Swings Between Gains and Declines as Spain Sells Debt

- Gold Seen Gaining an Eighth Day as Europe Crisis Spurs Demand

- Australia Sugar Exports at 3-Year High to Boost World Supply

- Korea Boosts Corn Imports From South America as Real Slumps

- Oil Supply Falls on Refinery Demand in Survey: Energy Markets

- Uralkali Rating to Pave Way for Debut Eurobonds: Russia Credit

- Australia to Boost Beef Supplies as Herd Climbs to 37-Year High

- Itochu Mirrors Xstrata in Trader to Miner Shift, Seeks Copper

- India’s Gold Imports Seen Lower as Record Price Cuts Demand

- Oil Supply Falls on Refinery Use in Survey

- GDF Suez Quits Europe as Belgium Plans to Shut Reactors: Energy

- BlackRock’s Hambro Says Mining Dividend Crusade Reaping Rewards

- Global Economy to Curb Wool Demand Even as China Boosts Supplies

CURRENCIES

EUROPEAN MARKETS

GERMANY – just an outright nasty ZEW (German expectations rpt) this morning at -16.9 for June (vs +10.8 in May) tells you all you need to know about #GrowthSlowing (at an accelerating rate) in one of the few remaining countries that didn’t have a big growth problem. Sold our German Bunds on green yesterday as growth tends to trump all other risk management factors at the turns.

ASIAN MARKETS

MIDDLE EAST

The Hedgeye Macro Team