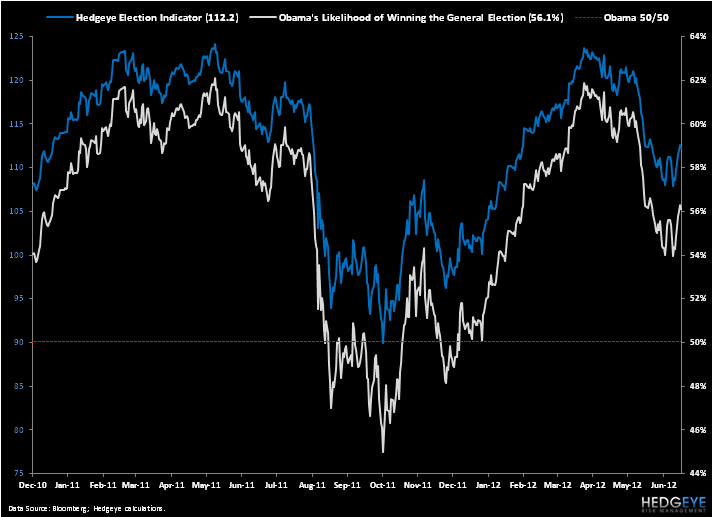

President Obama’s reelection chances improved to 56.1%, the highest level in nearly a month, thanks largely to a strong performance by the US stock market, according to the Hedgeye Election Indicator (HEI). It also marks the first time since late April that the President’s reelection chances improved on a week-on-week basis, according to the HEI.

Hedgeye developed the HEI to understand the relationship between key market and economic data and the US Presidential Election. After rigorous back testing, Hedgeye has determined that there are a short list of real time market-based indicators, that move ahead of President Obama’s position in conventional polls or other measures of sentiment.

Based on our analysis, market prices will adjust in real-time ahead of economic conditions, which will ultimately shape voters’ perception of the Obama Presidency, the Republican candidates and influence the probability of an Obama reelection. The model assumes that the Presidential election would be held today against any Republican candidate. Our model is indifferent toward who the Republican candidate is as the sentiment for Obama and for any Republican opponent is imputed in the market prices that determine the HEI. The HEI is based on a scale of 0 – 200, with 100 equating to a 50% probability that President Obama would win or lose if the election were held today.

President Obama’s reelection chances reached a peak of 62.3% on March 26, according to the HEI. Hedgeye will release the HEI every Tuesday at 7am ET until election day November 6.