Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email .

Key Takeaways:

* The Greek election. New Democracy, the pro-bailout/pro-austerity party, received the plurality of the vote on Sunday with 29.7%, eclipsing Syriza by roughly 2.5%. PASOK, the center-left party, took 12.3% of the total vote, which means New Democracy and PASOK together should be able to clear the 151-seat hurdle necessary to hold a majority of the legislature. Recall that in the May 6 election they fell short of the 151-vote threshold by 2 votes. As such, a Greek exit of the Eurozone has been delayed, and some measure of relief rally should be expected.

That said, Spanish and Italian CDS widened, rising 5.3% (+31 bps) and 3.0% (+16 bps), respectively. So, while Greece's election was viewed as a potential downside catalyst, it hasn't changed the negative reality facing either Spain or Italy's economy, or Greece's for that matter. While expectations are now high for austerity terms on Greece to be eased, the current rate of contraction in the Greek economy will make it all but impossible to comply with even reduced terms in the intermediate to long-term.

If you’d like to discuss recent developments in Europe, from the political to financial to social, please let me know and we can set up a call.

Matthew Hedrick

Senior Analyst

(o)

-------------

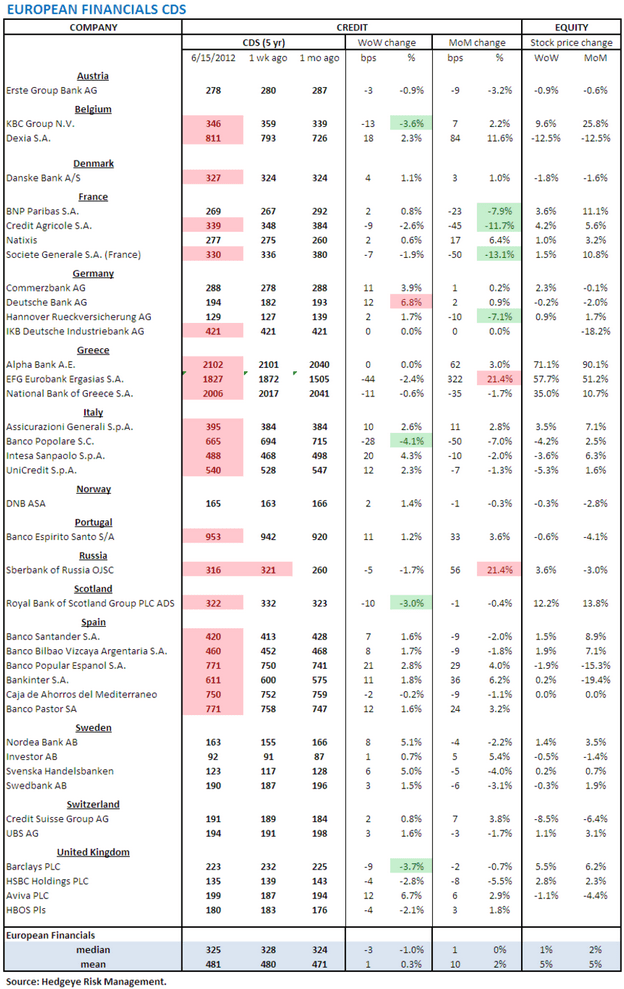

European Financials CDS Monitor – 26 of the 39 reference entities we track showed spreads widening across Europe last week. To be clear, these results are from last Friday, a few days before the Greek Election.

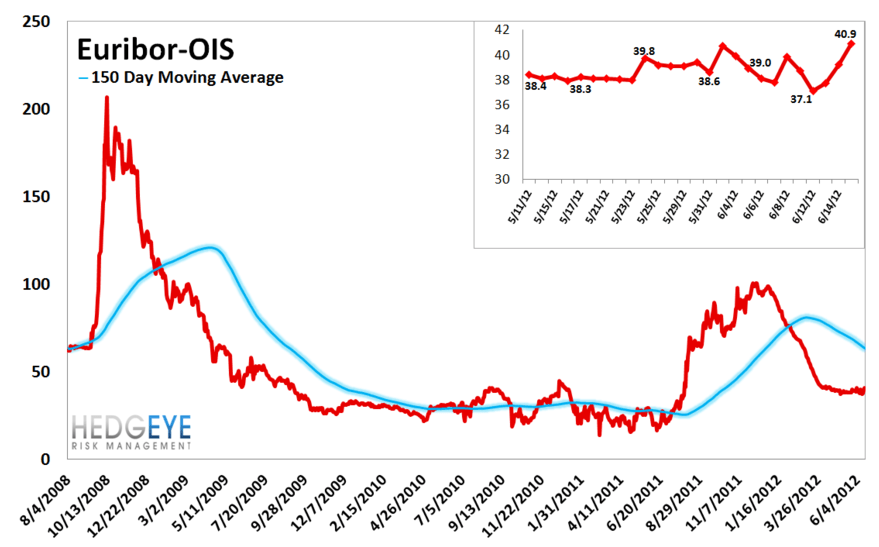

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread widened by 2 bps to 41 bps.

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis. The latest overnight reading is €741.2B.

Security Market Program – For the fourteenth straight week the ECB's secondary sovereign bond purchasing program, the Securities Market Program (SMP), purchased no sovereign paper for the latest week ended 6/15, to take the total program to €210.5 Billion.