Now that the pro-bailout party in Greece has effectively “saved” the European Union from an official meltdown, people are breathing a sigh of relief. But should they? We certainly don’t think so.

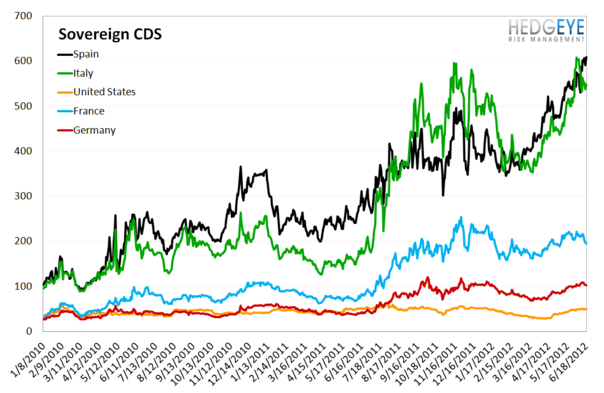

Credit default swaps on Spain and Italy widened over the weekend by several percentage points. That means investors are scared that they’re next in line for a default – or in this case, a bailout. Spanish and Italian banks are effectively the next institutions in line to come running to the International Monetary Fund for a bailout. As we’ve noted before (and will reiterate again): there is no trust in the markets.

One only need at the chart below, courtesy of Hedgeye Financials Sector Head Josh Steiner. While the U.S., France and Germany are in the clear for now, it’s become clear that time has run its course for Spain and Italy. After all, you can only kick the can down the road for so long.