June GGR forecast of 17-22% YoY growth

Macau had another strong week, generating average daily table revenues of HK$756 million. Our full month June forecast is now for GGR of HK$23.5-24.5 billion or 17-22%. We believe YoY growth at this level should inspire investors following the single digit growth of May.

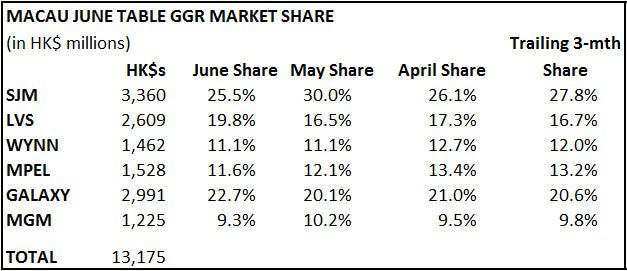

As we expected, LVS continues to gain market share. While 19.8% might not be sustainable over the near-term, it is representative of the longer term share we expect out of the company and certainly better than the 17% generated in the months prior and after the opening of Sands Cotai Central.