-- For specific questions on anything Europe, please contact me at to set up a call.

Positions in Europe: Short EUR/USD (FXE); Short Spain (EWP); Long German Bunds (BUNL)

Asset Class Performance:

- Equities: The STOXX Europe 600 closed up +0.9% week-over-week vs +2.9% last week and is down -0.1% year-to-date. Top performers: Cyprus +26.6%; Greece +13.7%; Ukraine +9.0%; Poland +3.1%; Russia (MICEX) +2.9%; Spain +2.5%; Romania +2.4%. Bottom performers: Finland -1.5%; Italy -0.4%; Czech Republic -0.1%.

- FX: The EUR/USD is up +0.93% week-over-week vs -0.58% last week. W/W Divergences: PLN/EUR +1.04%, SEK/EUR +1.01%, NOK/EUR +0.66%, HUF/EUR +0.43%, GBP/EUR +0.32%, DKK/EUR +0.02%, CHF/EUR +0.01%.

- Fixed Income: Yields swung around for yet another week. Greece saw the biggest move, falling -120bps week-over-week to 27.73% on increased bets that a coalition with the pro-austerity party New Democracy will win on Sunday. Portugal also saw large declines, falling -60bps to 10.58%. Spain powered higher, at +66bps to 6.88% and Italy gained +22bps to 6.00%, however dropped a full -25bps from Friday over Thursday. Germany also put on quite a move, bouncing +22bps to 1.50%.

60/40:

We’ll keep it short this week. We’re assigning a 60/40 probability in favor of a victory of pro-austerity party New Democracy in the Greek election on Sunday. Anti-austerity Syriza party head Alexis Tsipras has been very vocal this week stressing that he wants to “keep Greece in the Eurozone and restore growth”, however based on recent opinion polls we’re still behind the opinion that Greeks identify their future “prosperity” bound with membership in the Eurozone, and not removed with the Drachma, and we think Greeks are uncertain Tsipras can deliver.

That said, we view the timing of Spain’s €100B banking credit line as incredibility inept. Leading up to Saturday’s announcement, Troika was playing a relatively strong hand of cards, positioning the vote in Greece along the lines: vote New Democracy and stay in the Eurozone, or vote Syriza and default and exit the Eurozone. Saturday’s Spanish bailout folded a number of those strategic cards and encouraged the view that Troika will remain an unconditional backstop, regardless of who wins. To this end, Syriza could make this a very tight race. Yet in our opinion the pop in Greek equities this week (+13.7% w/w) is baking in a ND win.

The first exit polls are likely to be published at 5pm GMT on Sunday with the first official projections due out a few hours later. However, we may have to wait until late Sunday night or Monday morning for conclusive results.

Either way, the winner will most likely need to form a coalition government and will get 3 days to get this accomplished. If that fails, it passes to the 2nd place party for 3 days, and then to the 3rd place party.

The political set-up appears to simply be wait-and-see what happens in the Greek elections. Eurozone ministers have already said that they’ll hold a conference call on Sunday to discuss the outcome of elections. The wild card remains just what the outcome will be and what goalposts Eurocrats could decide to move on Sunday. However, we’d expect a bounce from equity markets and the EUR/USD on a New Democracy victory; and conversely, a sell off should Syriza poll ahead of ND, or if either party struggles to form a decisive coalition.

Don’t forget that Eurocrats mostly tread slowly; it’s the market participants and the media that want a resolution from Europe yesterday. As we said many times, given the constrained and conflicted nature of the Union of such uneven states under one monetary policy, Eurocrats have a long road to travel to save the region’s current fabric, if they can at all.

In a thick calendar for June we see a high likelihood that no firm policy action comes from the meetings this month. Monday starts the G20 Summit in Mexico; the Eurogroup and EcoFin meet on June 20-21; and the EU Summit convenes in Brussels on June 28-29. The main topics of discussion will include:

- Fiscal Compact

- Pan-European Deposit Insurance

- Eurobonds

- European Redemption Fund

- ESM (and EFSF)

- European Financial Transactions Tax

We continue to view Ms. Merkel as the Eurozone’s paymaster, the lead horse pulling the Eurozone cart along. We see Germany pushing the fiscal compact route, the initial building block should Germany even decide to sign off on Eurobonds or a pan-European deposit insurance facility. That said, we see agreement on a fiscal union over the near term as incredibly challenged as countries are unwilling to part with their fiscal sovereignty.

Interestingly, there have been mixed messages on the Germans’ position on the potential of a €2.3T European redemption fund that would essentially take over the excess sovereign debt of all countries that exceed the EU’s Growth and Stability Pact’s 60% debt to GDP limit in exchange for stricter economic oversight. This, however, especially in its initial discussion, seems out of character for the Germans who don’t want to signal they’re taking on the bulk of Europe’s risk (debt) – even though they’re carrying the lion’s share— and it also goes against their positioning that the member countries should do more for themselves (at least initially) to sort their fiscal houses before big brother Germany or Troika has to jump in.

As a reminder there will also be final round of parliamentary elections in France this weekend; the Socialists under PM Hollande look set to gain control.

For more on the impact of Spain’s €100B bank credit line see our note on 6/11 titled “Spain’s Cracked Credibility and Europe’s Bailout Messaging”.

EUR-USD:

Keith shorted the EUR/USD today in the Hedgeye Virtual Portfolio. Below is an updated EUR/USD price level chart. Our immediate term TRADE support is $1.24 and resistance is $1.27. Our intermediate term TREND support level remains at $1.23 and resistance is $1.29. Our call is that if $1.23 breaks, look out below! We’re not EUR parity folks because we see Eurocrats stepping in to prevent it. As we said above, we think the cross bounces on a New Democracy win and falls on a Syriza victory or any stumbles in coalition formation. That said, the wild card remains just how Eurocrats will responds on their Sunday conference call to the elections. Eurocrats, after all, can suspend gravity longer than you can remain solvent.

Call Outs:

Spain: El Mundo reported on Wednesday that loans made under the €100B bank bailout for Spain will have to be repaid in 15 years. The paper added that Spain will have to start repaying the loans in 2017, giving it a five-year grace period.

Germany's bailout bill continues to rise: The WSJ noted that the Spanish bank bailout will raise Germany's exposure to financially troubled Eurozone countries by as much as €25B. According to Credit Suisse, Germany's total commitment to crisis-fighting programs currently amounts to €113B, or 4.4% of German GDP. The firm also said that if the entire resources of the EFSF and ESM are eventually called upon, Germany's exposure to these facilities would be €401B. In addition, Germany has indirect exposure to the crisis via the ECB of €57B of the central bank's €212B holdings of peripheral sovereign debt, while its share of the €660B Target2 liabilities of Greece, Ireland, Italy, Portugal, and Spain is €179B. According to Credit Suisse, added together all the potential German exposure accumulates to €671B, or 25% of German GDP.

Italian tax increases back fire: Value-added tax receipts have declined since raised by 1 percentage point in Sept. as the economy was slipping into recession, government data released June 5 showed.

Germany: The government and opposition parties failed on Wednesday to resolve a row holding up parliamentary ratification of both the EU's new fiscal treaty and the euro zone's permanent rescue fund (ESM), and will resume talks next week. The ESM is meant to start working from July 1 but cannot do so without the approval of Germany. Merkel wants parliament to approve the two items at the same time, but needs opposition support for the fiscal treaty.

Spanish banks borrowed new record high from ECB in May: Bank of Spain noted that Spanish banks borrowed a new record high of €324.6B from the ECB in May, up from €316.9B in April. It added that total net borrowing was €287.8B in May, up from €263.5B in April.

Spain: ABC reports that Oliver Wyman & Roland Berger have set the capital needs for Spanish Banks at ~ €60-65 billion according to a draft report of the audit.

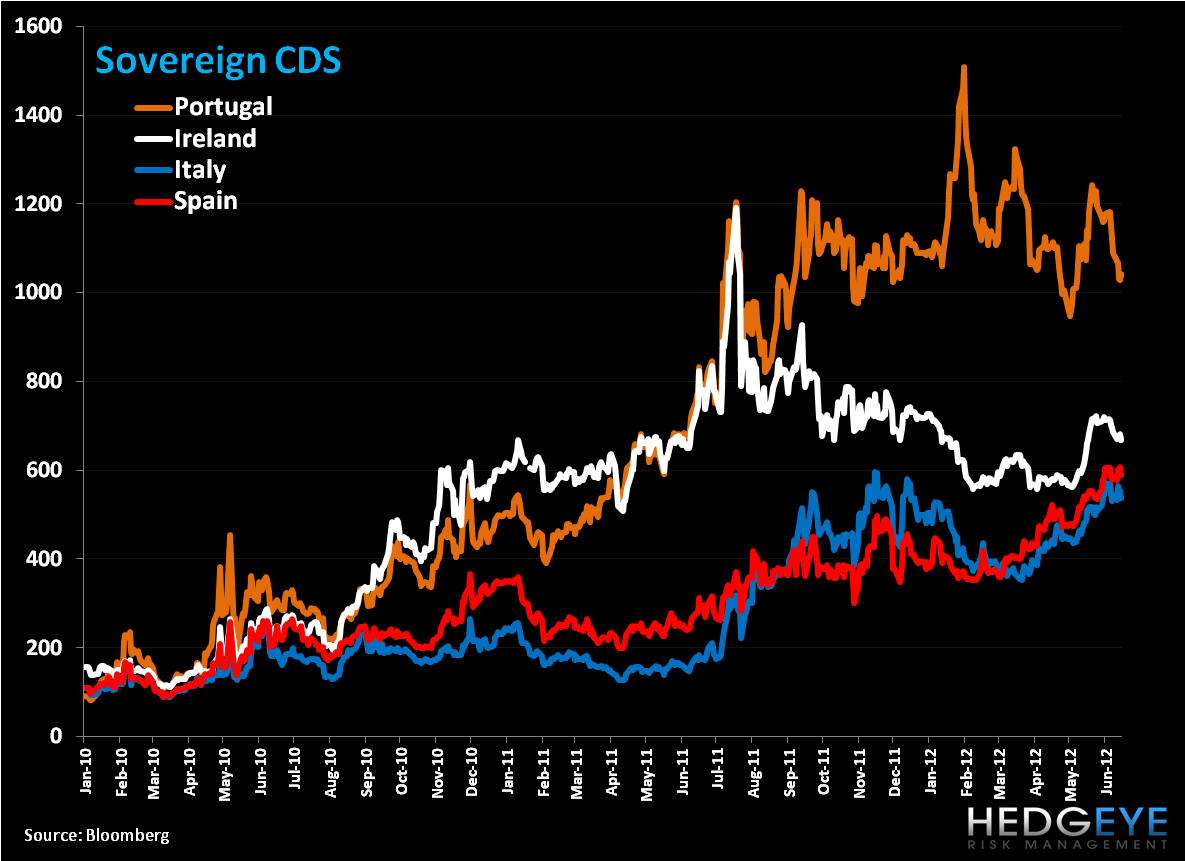

CDS Risk Monitor:

Week-over-week CDS were largely down. Portugal saw the largest declines in CDS w/w at -47bps to 1042bps, followed by Ireland -17bps to 669bps, and France -16bps to 197bps. Of the countries we track Spain saw a notable gain on the week of +4bps to 590bps.

Data Dump:

Eurozone CPI 2.4% MAY Y/Y vs 2.4% APR

Eurozone Labor Costs 2.0% in Q1 Y/Y vs 2.8% in Q4

Eurozone Industrial Production -2.3% APR Y/Y (exp. -2.7%) vs -1.5% MAR [-0.8% APR M/M (exp. -1.2%) vs -0.1% MAR]

EU 25 New Car Registrations -8.7% MAY Y/Y vs -6.9% APR

Germany CPI 2.2% MAY Final Y/Y vs pre vest 2.1%

Germany Wholesale Price Index 1.7% MAY Y/Y vs 2.4% APR

France CPI 2.3% MAY Y/Y vs 2.4% APR

France Industrial Production 0.9% APR Y/Y (exp. -0.3%) vs -1% MAR

France Manufacturing Production -1.4% APR (exp. -0.9%) vs -0.4% MAR

France Non-Farm Payroll 0.1% in Q1 Q/Q [UNCH vs prev. est.]

Italy Q1 GDP Final -0.8% Q/Q (UNCH) [-1.4% Y/Y vs prev est. -1.3%]

Italy Consumer Confidence 61 MAY vs 62.5 APR

Italy CPI 3.5% MAY Final Y/Y [unch]

Spain House Transactions -9.9% APR Y/Y vs -22.7% MAR

Spain CPI 1.9% MAY Final Y/Y [unch]

Spain Home Prices -12.6% in Q1 Y/Y vs -11.2% in Q4

UK Industrial Production -1% APR Y/Y vs -2.6% MAR

UK Manufacturing Production -0.3% APR Y/Y vs -0.9% MAR

Switzerland Producer and Import Prices -2.3% MAY Y/Y vs -2.3% APR

Portugal CPI 2.7% MAY Y/Y vs 2.9% APR

Norway CPI 0.5% MAY Y/Y (inline) vs 0.3% APR

Norway Producer Prices incl. oil 2.5% MAY Y/Y vs 2.5% APR

Finland CPI 3.1% MAY Y/Y vs 3.1% APR

Sweden CPI 1.0% MAY Y/Y vs 1.3% APR

Greece Unemployment Rate 22.6% in Q1 vs 20.7% in Q4

Malta CPI 3.7% MAY Y/Y vs 3.8% APR

Latvia Unemployment Rate 12.3% MAY vs 12.9% APR

Hungary CPI 5.3% MAY Y/Y vs 5.7% APR

Hungary Industrial Production -3.1% APR Final Y/Y [unch vs prev. est]

Slovakia CPI 3.4% MAY Y/Y vs 3.6% APR

Interest Rate Decisions:

(6/14) SNB 3-Month Libor Target Rate UNCH at 0.00%

(6/15) Russia Overnight Deposit Rate UNCH 4.00%

(6/15) Russia Overnight Auction-Based Repo UNCH 5.25%

(6/15) Russia Refinancing Rate UNCH 8.00%

The Week Ahead:

Sunday: Greek Elections; parliamentary elections in France; May UK Rightmove House Prices

Monday: G20 Summit in Los Cabos, Mexico; May UK Nationwide Consumer Confidence (Jun. 18-22)

Tuesday: Apr. Eurozone Construction Output; Jun. Germany Zew Survey; May UK CPI, Retail Price Index; Apr. UK ONS House Price; Jun. France Own-Company Production Outlook, Business Confidence Indicator, Production Outlook Indicator

Wednesday: Eurogroup Meeting, Ecofin Meeting in Luxembourg (Jun. 20-21); May Germany Producer Prices; BoE Minutes; May UK Claimant Count, Jobless Claims Change; Apr. UK Average Weekly Earnings, ILO Unemployment Rate, Employment Change; Apr. Spain Trade Balance; Apr. Italy Industrial Orders, Industrial Sales, Current Account

Thursday: Jun. Eurozone Consumer Confidence – Advance, PMI Composite – Advance, PMI Manufacturing and Services - Advance; Apr. Eurozone BoP Current Account, ECB Current Account; Jun. Germany PMI Manufacturing and Services – Advance; Jun. UK CBI Trends Total Orders, CBI Trends Selling Prices; May UK Retail Sales; Jun. France PMI Manufacturing and Services – Preliminary; Apr. Spain Mortgages-Capital Loaned, Mortgages on Houses; 1Q Netherlands GDP - Final

Friday: Jun. Germany IFO - Business Climate, Current Assessment, Expectations; 1Q France Wages – Final; Jun. Italy Consumer Confidence Indicator; Greek T-Bill Redemption for €1.3B; Apr. Greece Current Account

Extended Calendar Call-Outs:

18-19 June: G20 Summit in Los Cabos, Mexico

20-21 June: Eurogroup Meeting; Ecofin Meeting in Luxembourg

22 June: Greek T-Bill Redemption for 1.3 Billion EUR

28-29 June: EU Summit in Brussels, aim to formally sign off on growth proposals; EC meets to discuss Institutional Affairs

30 June: Deadline for EU Banks to meet €106B capital target/the 9% Tier 1 capital ratio, Iceland – Presidential election

JULY: France – extraordinary session of parliament in July is due to re-draft the 2013 budget

1 July: ESM to come into force

5 July: ECB governing council meeting

19 July: ECB governing council meeting

18-19 October: Summit of EU Leaders

Matthew Hedrick

Senior Analyst