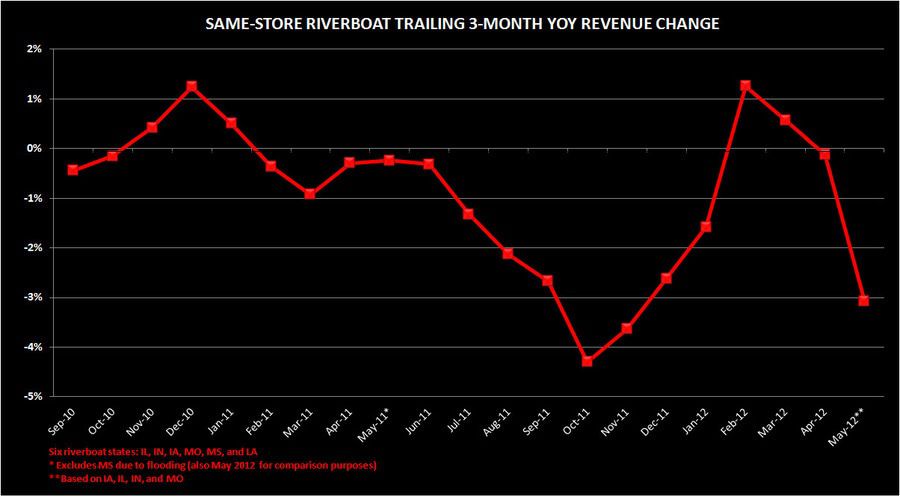

Hedgeye Gaming, Lodging and Leisure Sector Head Todd Jordan has released a chart that will make anyone who was long traditional gaming think twice.

The truth of the matter is that established domestic gaming markets are under severe pressure due to multiple factors. They include the faltering economy, an aging customer base and of course, new competition. May is looking really ugly for the five regional gaming states. Same store sales are expected to take a hit of 3%, as indicated on the chart. The upturn that occurred in February is considered to be cyclical as the economy heavily influences this market.