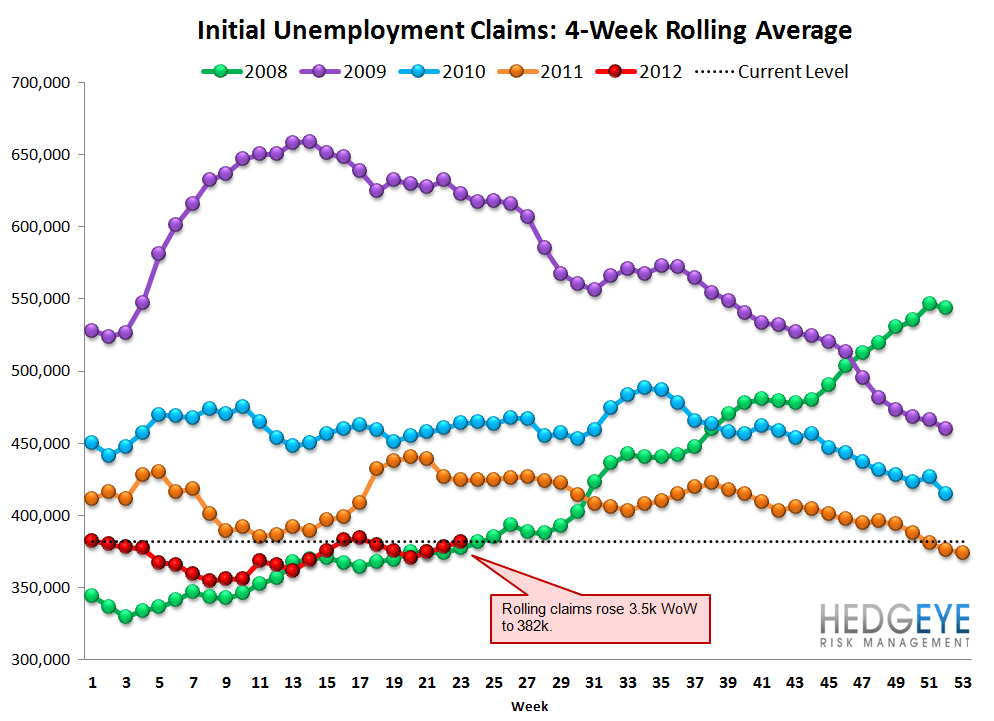

Claims Continue to March Higher

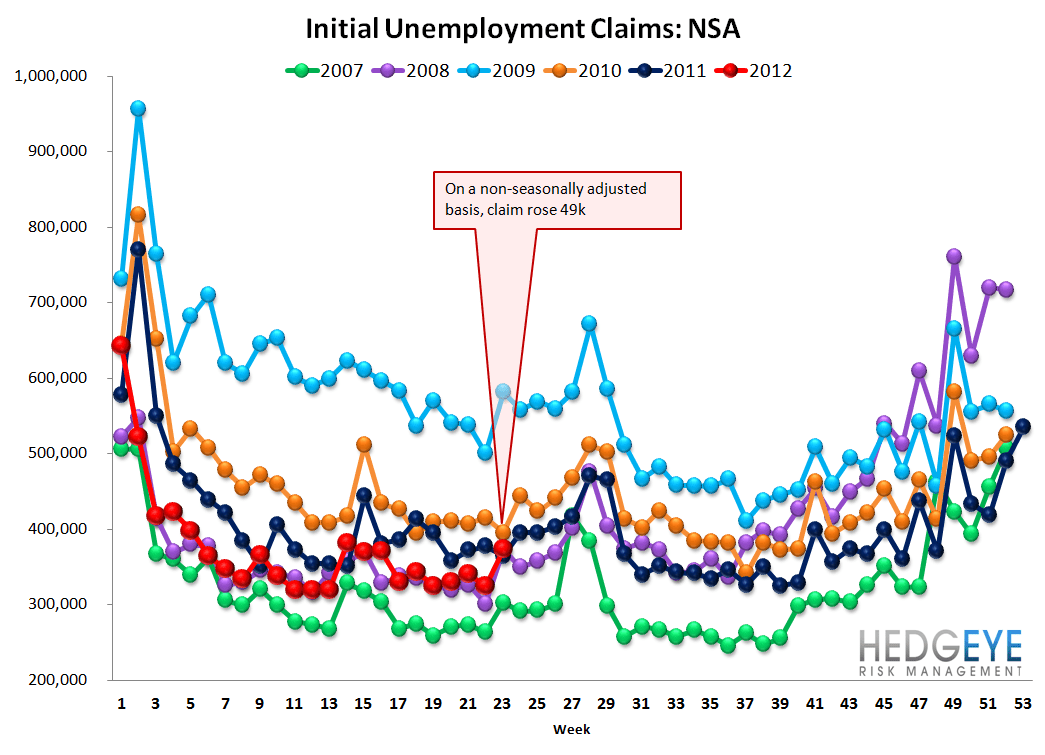

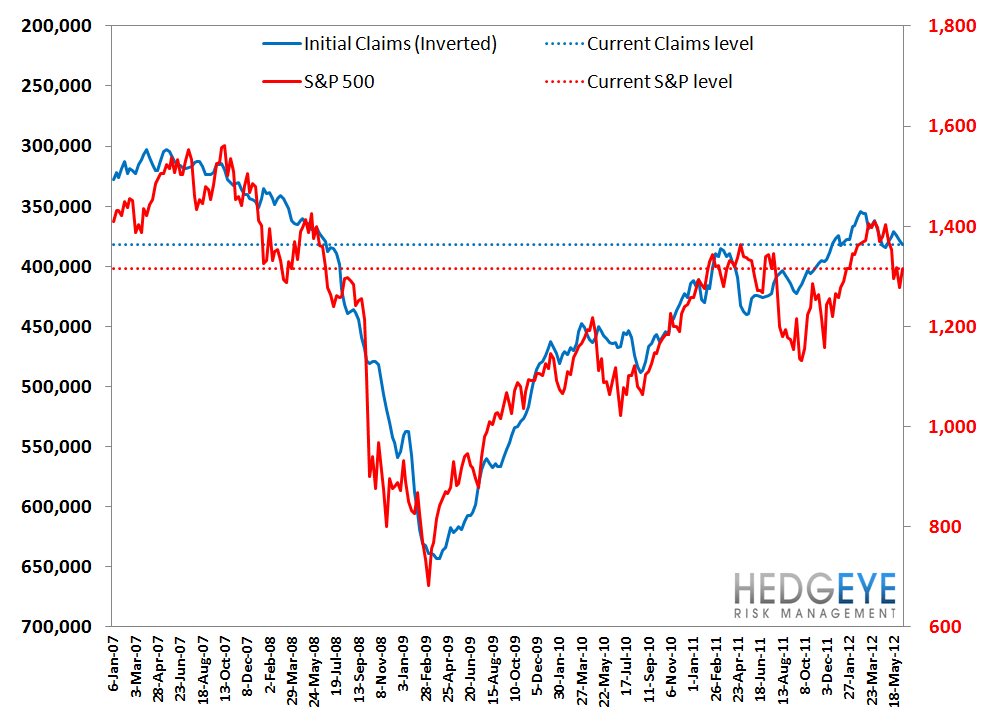

Claims move notably higher again this week, up 9k WoW to 386k. Excluding the normal weekly revisions, which this week were 3k, claims were higher by 6k (377k vs 380k). This data series continues to play out very consistently with our framework for thinking about the seasonal distortions taking place in the economic data. As a reminder, we think the data will continue to get worse for approximately two more months before starting to get better. Rolling claims rose 3.5k to 382k. On a non seasonally adjusted basis, claims were 9% lower YoY.

The Yield Curve Continues to Get Steamrolled

The 2-10 spread tightened another 10 bps last week to 130 bps as of yesterday. The ten-year yield decreased 6 bps to 160bps. To put this in perspective, if spreads hold where they are now, the 3Q12 sequential change will rival what we saw in 3Q11, an ominous sign for bank margins.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.