Nobody expenses ‘em like LVS.

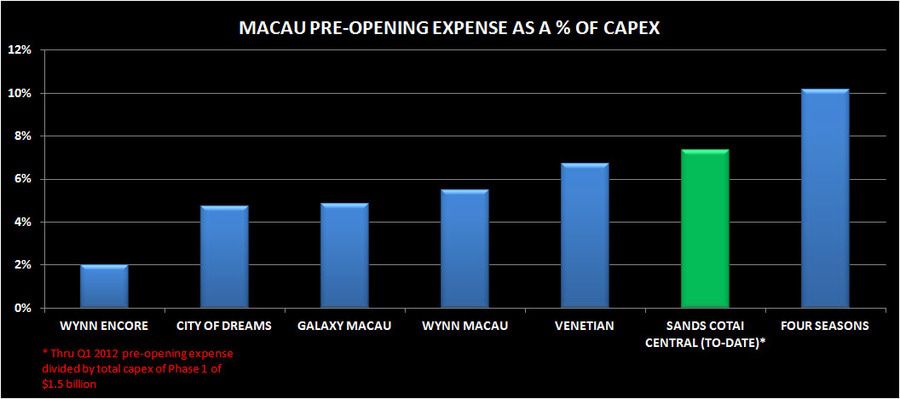

Q2 is likely to tell us little about the ongoing cost structure of Sands Cotai Central (SCC) and LVS’s combined Macau operations. As can be seen in the chart below, LVS has been aggressive in the past, to say the least, in terms of expensing costs into the convenient pre-opening expense line. While some of pre-opening costs are inevitably recurring, companies and analysts exclude them from ongoing operations.

With a very disappointing post-SCC top line, one would expect very weak margins. However, given the flexibility with the pre-opening bucket, the only clear takeaway on future margins from the Q2 earnings release will be that there is no clear takeaway. We are projecting only a net $45 million YoY increase in Macau property EBITDA for LVS in Q2, despite almost a full quarter contribution from the $1.5 billion SCC. Moreover, over $30 million of that increase was at Four Seasons. Given the additional investment, our overall Q2 Macau margin falls from 33.0% to 29.2%. Of course, we have no idea how much LVS will allocate to pre-opening so the margin could be higher.

The chart below shows that pre-opening as a % of total capex has already exceeded Venetian and we haven’t even included the Q2 expense. Obviously, there is precedent for an additional 3% to get to the level of Four Seasons which would imply an additional $40-45 million in pre-opening costs.