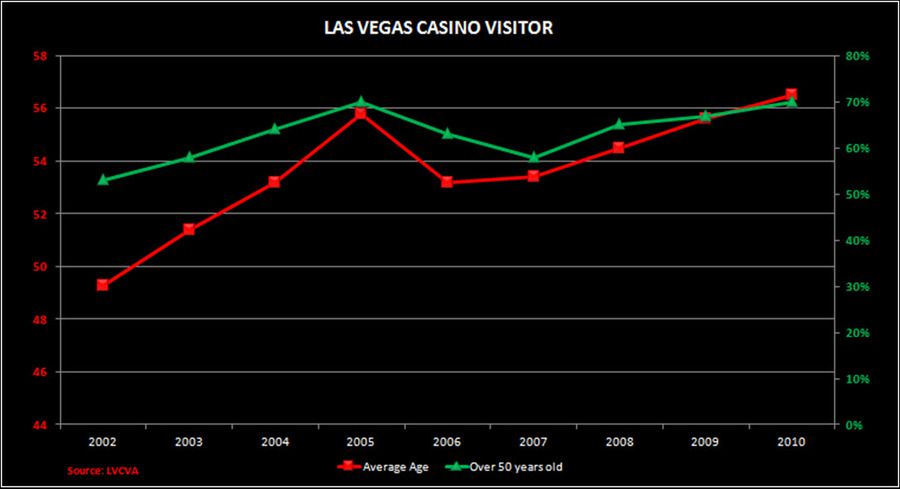

- Younger generations aren't gambling as much

- Casinos and slot makers have been trying for years to attract sub-Baby Boomer generations, to no avail

- Baby Boomers can’t live forever

By joining our email marketing list you agree to receive marketing emails from Hedgeye. You may unsubscribe at any time by clicking the unsubscribe link in one of the emails.