TODAY’S S&P 500 SET-UP – June 8, 2012

As we look at today’s set up for the S&P 500, the range is 49 points or -2.43% downside to 1283 and 1.29% upside to 1332.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/7 NYSE: -252

- Versus prior trading day +2305

- VOLUME: on 6/7 NYSE 854.61

- Versus prior trading day 711.57

- VIX: as of 6/7 was at 22.16

- Change versus prior trading day of -2%

- Year-to-date change of -7.2%

- SPX PUT/CALL RATIO: as of 6/7 1.41

- Versus prior trading day 1.74

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning: 38.7

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year yield: as of this morning 1.67

- Versus prior trading day 1.65

- YIELD CURVE: as of this morning 1.30

- Versus prior trading day 1.37

TODAY’S U.S. ECONOMIC EVENTS

- 8:30 am: Trade Balance, April, est. -$49.5b (prior -$51.8b)

- 10am: Wholesale Inventories, April, est. 0.4% (prior 0.3%)

- Fed to purchase $1b-$1.5b note in 2/15/2036 to 5/15/2042 range

- 1pm: Baker Hughes rig count

- 8pm: Fed’s Kocherlakota to speak on economic theory in Michigan

GOVERNMENT

- American Bankers Association issues economic forecast. 10am

- President Obama holds bilateral meeting with Philippines President Benigno Aquino. 2pm

- House in session

- House Ways and Means subcommittee holds hearing on tax extenders. 9:30am

WHAT TO WATCH

- U.S. moves ahead with implementing global bank capital rules

- Chesapeake Energy holds annual meeting; Chesapeake shareholders seen to challenge directors’ CEO review

- Olympus to cut 2,700 jobs, ~7% of its workforce, may consider an alliance to boost capital

- Google co-founders Larry Page, Sergey Brin said to be slated for questioning by U.S. antitrust regulators

- U.S. trade deficit likely shrank in April on falling oil prices

- Morgan Stanley, other global banks undergoing credit review by Moody’s; decision expected by end of month

- NYSE opposition to Nasdaq’s proposed remedy to Facebook’s botched IPO could delay Facebook compensation plan

- Spanish Prime Minister Mariano Rajoy holds bank talks with EU leaders as Fitch cuts Spain

- CA said has begun succession planning for CEO Bill McCracken, who turns 70 this yr

- Apple’s move to block Samsung Galaxy phone placed on fast track

- Federal Housing Administration to boost sale of delinquent loans to investors: WSJ

- McDonald’s releases monthly sales

- Nomura apologizes for multiple insider trading cases

- Watch for update on GlaxoSmithKline’s $13-shr hostile bid for Human Genome; tender deadline was yday

- Russell Index rebalancing after the close

- U.S. Inflation, Apple, OPEC, Egypt Votes: Week Ahead June 9-16

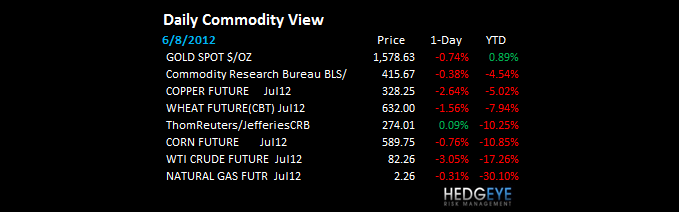

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Copper Trade Most Bullish Since March as China Cuts: Commodities

- Oil Heads for Longest Run of Weekly Losses in More Than 13 Years

- Commodities Head for Longest Weekly Losing Streak in 11 Years

- Copper Falls Most in Eight Weeks Without Fed Stimulus Signal

- Gold Drops in London as Bernanke Dampens Stimulus Expectations

- Coffee Falls on Speculation Slower Growth Will Curb Consumption

- Palm Oil Set for 20-Month Low as Mistry Sees Demand Slowdown

- Jiangxi Copper Considers Halting LME Exports as Prices Decline

- Barclays, BNP Japan Commodity Sales Heads Leave as Banks Cut

- Cooking Oil Demand in India Poised to Climb 29% as Income Rises

- Palm Oil Seen Extending Drop on Falling Biofuel Appeal, Fry Says

- LNG Sellers Bet on Oil-Link Amid U.S. Shale Boom: Energy Markets

- Kingsman Raises 2012-13 World Sugar Surplus By 63% on Plantings

- Copper Trade Most Bullish Since March

- Copper Stockpiles in Shanghai Decline for Ninth Week

- Merchant Commodity Hedge Fund Said to Drop 7.5% Last Month

- Rubber Declines for Fifth Week as Bernanke Holds Off Stimulus

CURRENCIES

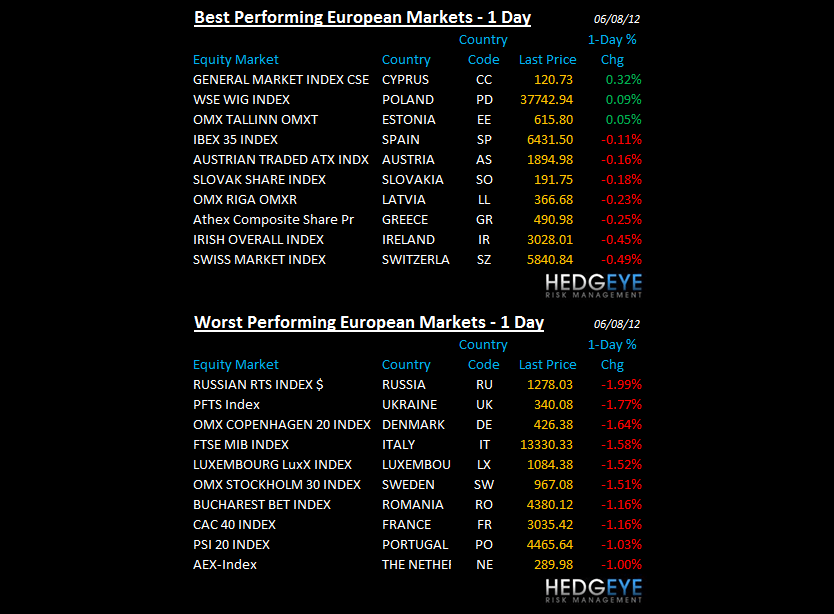

EUROPEAN MARKETS

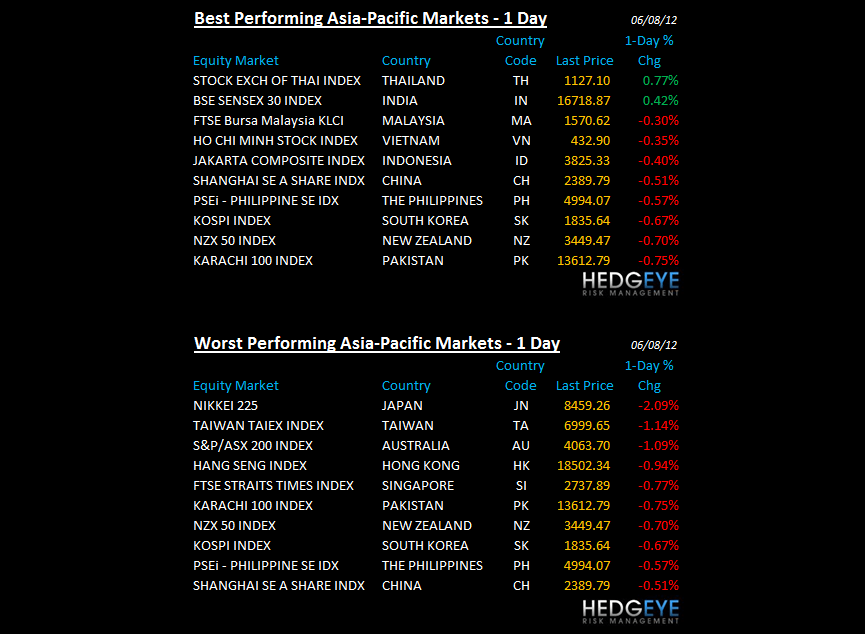

ASIAN MARKETS

MIDDLE EAST (HEADLINES FROM BLOOMBERG)

- Steepest Global Slide Since Recession Pushes Central Bank Cuts

- Oil Heads for Longest Weekly Losing Streak in More Than 13 Years

- Stocks Decline With Oil as Bernanke Damps Stimulus Speculation

- Malaysia Sukuk Gain a 5th Week on 15-Year Debut: Islamic Finance

- Mizuho Ousts WestLB as Japanese Boost Lending: Turkey Credit

- LNG Sellers Bet on Oil-Link Amid U.S. Shale Boom: Energy Markets

- Oil May Climb as OPEC Meets, U.S. Supplies Shrink, Survey Shows

- Iran’s LNG Company Says Sanctions Won’t Deter Production in 2013

- GCC Sales Set for Record First Half as Costs Drop: Arab Credit

- Bernanke Anxieties Embodied as Bond Sales Tumble: Credit Markets

- Rajoy Bid to Avoid Full Bailout Risks Falling Short: Euro Credit

- U.S. Inflation, Apple, OPEC, Egypt Votes: Week Ahead June 9-16

The Hedgeye Macro Team