Positions in Europe: Long German Bunds (BUNL); Short EUR/USD (FXE)

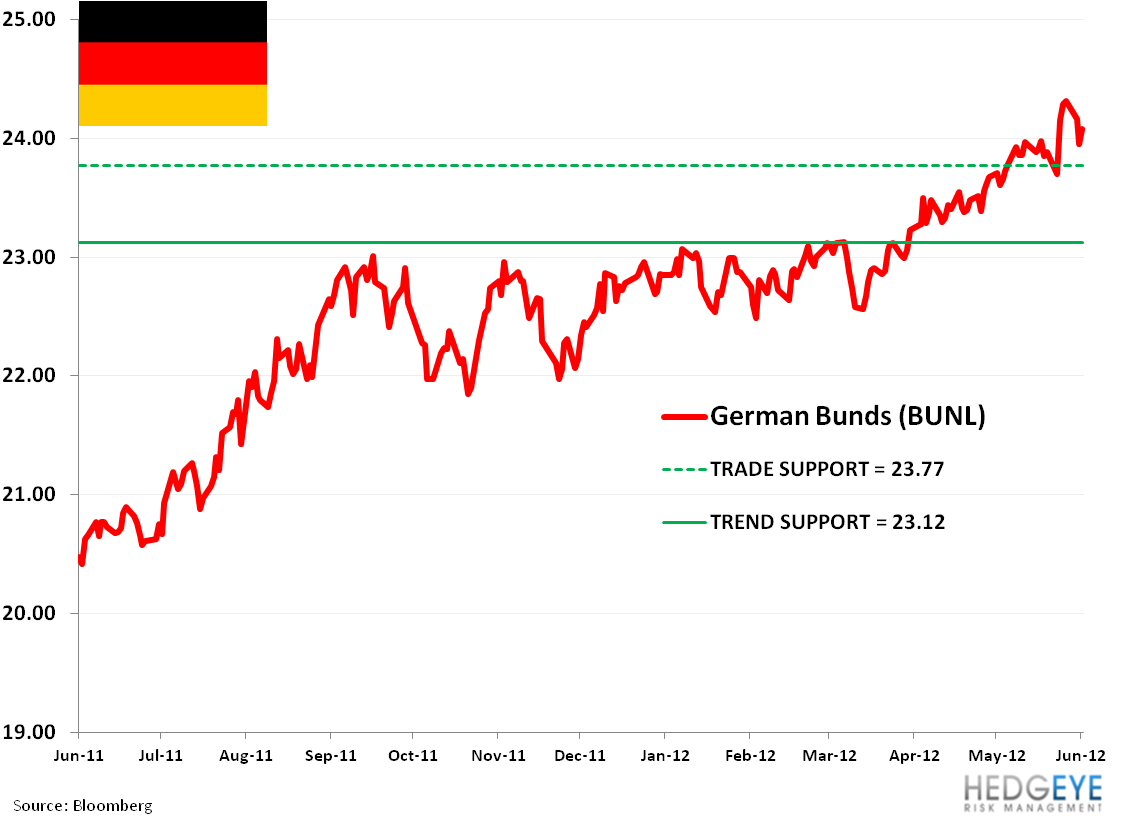

Keith bought German Bunds via the etf BUNL in the Hedgeye Virtual Portfolio today. The etf is in a bullish formation, meaning the current price is above its immediate term TRADE and intermediate term TREND levels (see chart below). Buying BUNL takes our Fixed Income asset allocation to 12% versus 0% at the start of the week. We do expect German fixed income to remain a bet on safety. A threat to this positioning would be any indication from Chancellor Merkel of a softening line or full acceptance of Eurobonds.

Our thinking about investing in Europe hasn’t changed: there’s a relative advantage to playing the capital markets of the stronger countries on the long side and weaker countries on the short side, at a price. We’re highly sensitive to price and well aware that there’s no simple equation to pair or hedge risk in Europe: political headline risk, even from the tiniest of countries in Europe, can roil country equity indices and influence yields across the continent.

However, from a political timing perspective, we expect Eurocrats to evaluate the outcome of Greek elections on 17. June before embarking on deeper discussions around a fiscal union, Eurobonds, and a Pan-European deposit insurance, topics that should be central at the EU Summit on June 28-29.

Matthew Hedrick

Senior Analyst