This note was originally published at 8am on May 24, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“You come home, and you party. But after that, you get a hangover. Everything about that is negative.”

-Mike Tyson

Yesterday Keith, myself, and our head of consulting, Michael Lintell, had a meeting with one of our long term subscribers in our New Haven office. Not only does this client have a great long term track record in their respective market (which happens to be Europe), but they are massively outperforming this year as well. I won’t get into the intricacies of our discussion, but at the end of the meeting we all collectively agreed that this is not the type of market that you want to trade with a hangover.

For those that have never had a hangover before, Wikipedia defines a hangover as follows:

“A hangover is the experience of various unpleasant physiological effects following heavy consumption of alcoholic beverages. The most commonly reported characteristics of a hangover include headache, nausea, sensitivity to light and noise, lethargy, dysphoria, diarrhea, and thirst, typically after the intoxicating effect of the alcohol begins to wear off. While a hangover can be experienced at any time, generally speaking a hangover is experienced the morning after a night of heavy drinking. In addition to the physical symptoms, a hangover may also induce psychological symptoms including heightened feelings of depression and anxiety."

Arguably the way the market is trading currently, with the SP500 down 5.7% for month to date, it is creating feelings of depression and anxiety in many stock market operators. In effect, a market hangover over that is akin to taking down too many Jägerbombs the night before (for you old timers a Jägerbomb involves dropping a shot of Jägermeister into a glass of Red Bull and then chugging it).

The last five days of trading are prime examples as to why you need all of your wits about you. Yes, some investors with true long term duration don’t have to adjust exposures and worry about monthly or quarterly performance, but the reality is that most of us do have to worry about short term performance. In a market like this, the only way to really capture marginal performance, especially when correlations are heightened, is to “buy ‘em” when other people are selling and “sell ‘em” when other people are buying.

In the Chart of the Day, we emphasize the volatility of the last week. The SP500 started the period at 1,328 then traded down to 1,295 then ripped up to 1,331 and then dropped back to 1,300. Much like a hangover, that kind of short term volatility can be nauseating. We actually look at it in a positive light and use it as an opportunity to adjust exposures accordingly, and gain performance edge. While everyone’s strategy is unique, email our head of consulting at mlintell@hedgeye.com if you want some help developing a more proactive risk management strategy for your portfolio.

Obviously the key driver of recent volatility in equities is Europe. This morning we are getting more of the same. On one hand European equities are at the highs of the day and respecting yesterday’s late day rip in U.S. equities. On the other hand, there remains little chance of resolution to the sovereign debt mess in Europe, especially given the shifting politics.

Currently, the positive sentiment is centered on increased chances of Euro-area deposit insurances and the growing likelihood of Eurobonds that were supposedly discussed at yesterday’s summit. In reality, though, no new progress was made and the next summit is not until June 28th. Frankly, European Central Bank President Mario Draghi probably summarized it best yesterday when he said:

“Euro bonds make sense when you have a fiscal union, otherwise they don't make sense. They are the first step towards a fiscal union.”

We have said it many times, a monetary union is no union at all without a strong political and fiscal union. Until that occurs, the Euro is doomed to fail.

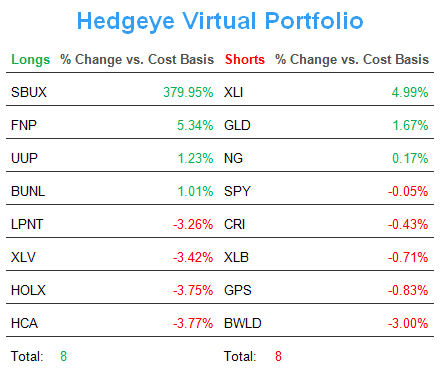

The one global macro market that is slowly shifting from being in hangover mode to recovery mode is natural gas. In our best ideas call yesterday, we emphasized our shift from being long term natural gas bears to getting more constructive on natty. Some of the key reasons are as follows:

1. Bottoms are processes, not points. And after a 3.5 year bear market in gas that saw the front-month NYMEX contract fall 80%, we think that bottoming process is in motion; front-month gas has bounced convincingly off the $2/Mcf level, gaining 30% in a month to trade over $2.60/Mcf, and has regained its TRADE and TREND lines on our quantitative model.

2. Production growth is slowing, and will continue to slow. Gas production is already slowing on the margin: +4% YoY in early May versus +9% in 4Q11. We see that decline accelerating as oil prices move lower. Our research indicates that the average full-cycle cost to produce 1 Mcf of gas in North America is ~$5.50/Mcf ($2 cash cost and $3.50 PD FD&A cost), which suggests that producers in aggregate are well below breakeven.

3. Demand from the power sector is surging and won’t stop. The U.S. power sector has responded to the low gas price by increasing consumption 44%, or 7.5 Bcf/d, YoY in the first week of May, taking market share away from coal, nuclear, and hydro in a short amount of time.

4. The 2012 storage issue is priced-in. We will hit storage capacity this fall. That is probably the most consensus opinion on natural gas there is in the market right now. In fact, in an April 2012 survey of investors and industry professionals, 78% said that we will hit storage capacity this year.

5. From a long-term perspective, sentiment is still bearish on natural gas. From 1995 – 2006, non-commercial traders (hedge funds, mutual funds, etc.) were net neutral on natural gas. Only since 2007 have non-commercial traders been heavily, consistently, and correctly short the commodity.

Just like real hangovers, most hung over markets will eventually recover. We believe natural gas is one of those markets.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research