“A jelly donut is a yummy mid-afternoon energy boost.”

-David Einhorn

On a flight to Dallas, Texas yesterday, I was reviewing My Pile and re-read David Einhorn’s Op-Ed from May 3rd, 2012 in the Huffington Post titled “The Fed’s Jelly Donut Policy.” Loved it.

I love donuts, burgers, and beers too. What I don’t love is pretty clear – Ben Bernanke’s post 2009 Policies To Inflate rank right up there at the top of my no-love list alongside listening to Giraldo Rivera and watching figure skating.

What I also love is the debate. I love to argue; particularly with people that don’t. How else do we hold these charlatans accountable? How else are we going to challenge the perceived wisdoms of their economic policies? How else are we going to evolve and progress?

Alongside Ray Dalio (Bridgewater Associates) and Seth Klarman (Baupost Group), I consider David Einhorn (Greenlight Capital) one of the thought leaders of Wall St 2.0. Stylistically, while Einhorn is often compared to Warren Buffett (“value guys”), I think he’s currently evolving his investment process at a much faster pace. Einhorn does macro – he shorts things too.

Einhorn isn’t politically polarized like Buffett has become. He is able to evaluate macro risks objectively (what the Fed should do and balance that with his opposing thoughts of what the Fed will do). He’s embraced Behavioral Finance, writing openly about fear and greed. He also understands that the stock market is not the economy, and that “valuation” is not a panacea.

On Bernanke’s failed policies, here’s my abbreviated version of Einhorn’s Op-Ed:

“The blame lies in his misunderstanding of human nature. The textbooks presume that easier money will always result in a stronger economy, but that’s a bad assumption… it is simply misguided thinking that persists among the Fed Chairman and other government ivory tower thinkers. They do not understand or relate to the prime component of capitalism and a free market: greed.”

“The Fed does not understand investor psychology: if you want to get people to sell bonds and buy stocks, the best way to do that is to show them that bond prices can, and do, fail… there is nothing that slows the economy faster than rising oil prices… In light of this, I cannot understand why we are even discussing let alone hoping, for Qe3.”

Agreed, Mr. Einhorn. Agreed. Hope is not a risk management process. Neither is doing more of what didn’t work. Enough of the yummy intraday stock market rallies on iQe4 upgrade rumors already. After 3 of these suckers, Americans have a “tummy ache.”

Back to the Global Macro Grind…

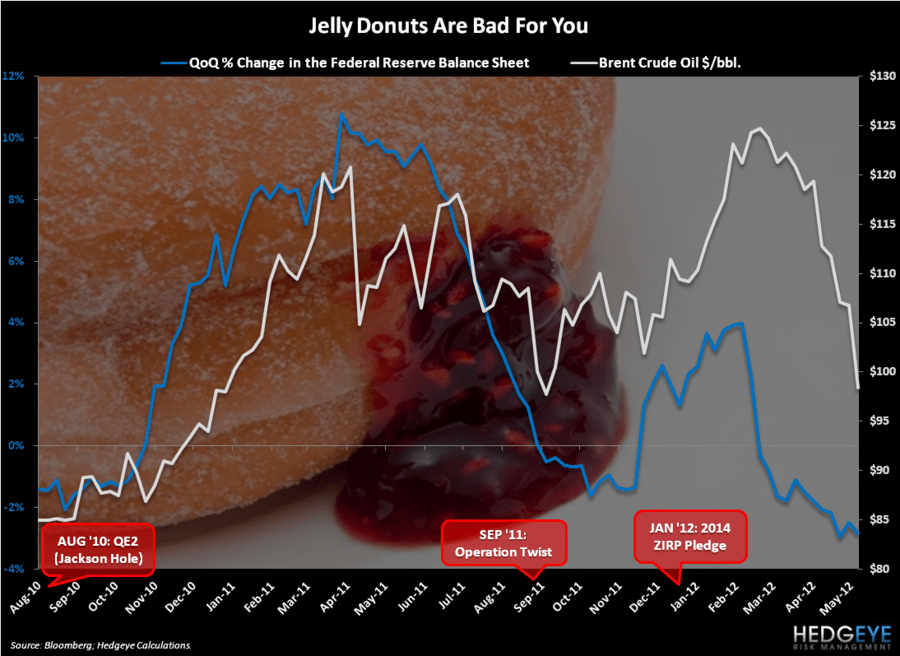

Strong Dollar = Deflates The Inflation = Stronger Consumption. That remains our bull case for not only the US and Global Economy, but for their Equity market multiples.

Yesterday’s US Services ISM report (May) was one of the most constructive we have seen on the Prices Paid front since December:

- US Services ISM of 53.7 (May) vs 53.5 (April) stopped slowing – that’s better than bad

- Prices Paid (within the ISM Services report) dropped -7.1% month-over-month to 49.8 (vs 53.6)

- Employment dropped -6.2% month-over-month to 50.8 vs 54.2

So, employment is bad and getting worse. But A) you know that B) so does the bond market and C) employment is a lagging (as opposed to a leading), indicator. Real-time market prices are also leading indicators.

In other words, if you are begging for Bernanke’s iQe4 Upgrade this morning, you are begging for prices paid to go back up at the pump – and you are begging for the leading indicator on real (inflation adjusted) economic growth to continue to slow.

Begging isn’t leadership. It’s un-American.

Our process hasn’t changed in scoring how the real world works. Unfortunately, neither has the Washington and Old Wall Street consensus. These people don’t have a risk management process. This is what they do. So it will be very interesting to see how the political pressure for Bernanke to bailout everything from Europe to Morgan Stanley looks in the coming days and months.

Bailing out Europe through the Washington, DC based (and US tax payer backed) IMF? Yep, I’m thinking Einhorn will lead from the front and have a few things to say about that too.

In the meantime, the SP500 recapturing our long-term TAIL line of support (1283) yesterday should be as bullishly received as it was bearish when it snapped on the downside.

Yes, “risk” changes faster than you can bang back another Jelly Donut. That is the game we are in, so play it.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar, EUR/USD, and the SP500 are now $1, $96.21-103.11, $82.03-83.35, $1.22-1.25, and 1, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer