McDonald’s will release May sales results on Friday before the market open. The price action in the stock is indicating a degree of investor skepticism heading into the summer months. With price running at 3%, it will be a tall order for the company to maintain the impressive traffic growth that the company has produced over the last year or so.

McDonald’s was one of our favorite names in the restaurant space in during 2011 (from April onward, before that we were bearish and wrong). On April 24th, 2012, we wrote that “we see plenty to be concerned about” regarding the top line going forward and that our “conviction on the top-line continuing to meet consensus is tenuous at best”. Following the April sales release, growing risks to the top line heightened our concern and we think that the May sales release will once again disappoint investors. With price running at roughly 3% in the United States and 2-3% in Europe, the company will need to drive substantial gains in traffic to meet consensus estimates and we lack confidence that the pipeline of promotions for the summer months is sufficient. Beverage promotions over the past two years have been instrumental in driving traffic yet management has been placing far less emphasis on beverages in their recent communications with Wall Street (earnings calls) than in years prior.

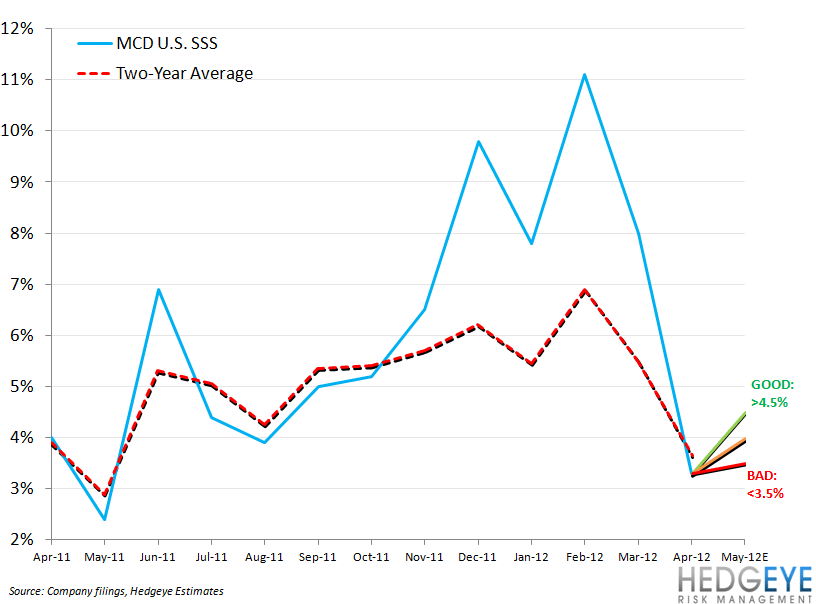

Below we go through our take on what comparable restaurant sales numbers will be received as good, bad, and neutral by investors. For comparison purposes, we have adjusted for historical calendar and trading day impacts (but not weather).

Compared to May 2011, May 2012 had one additional Wednesday, one additional Thursday, one less Monday, and one less Sunday. As a result, we expect a slightly negative calendar shift to impact the headline number.

U.S. - facing a relatively easy compare of 2.4%, including a calendar shift of between -1.5% and +0.5%, varying by area of the world:

GOOD: A print of higher than 4.5% would be received as a strong result by investors as it would imply a sequential acceleration in the calendar-adjusted two-year average trend as well as 1.5% of mix/traffic growth on top of the 3% of price that the U.S. business is running. With growth slowing globally and economic uncertainty mounting in the U.S., we think that this would be a strong result given the current environment and lack of promotions that can replicate what frappes and smoothies achieved last year. We are anticipating a print of 4% for U.S. comparable store sales growth in May.

NEUTRAL: A print of between 3.5% and 4.5% would be considered neutral by investors, in our view, as it would imply two-year average trends that are roughly flat on a calendar-adjusted basis.

BAD: A result of less than 3.5% would imply a significant slowdown in two-year average trends and would likely cause the stock to sell off further. While we do believe that McDonald’s sales trends are slowing, we do not think a number as low as 3% is likely.

Europe - facing a relatively easy compare of 2.3%, including a calendar shift of between -1.5% and +0.5%, varying by area of the world:

GOOD: A print of more than 5% would be considered a strong result as it would imply two-year average trends level with those seen in April on a calendar-adjusted basis. Given the weakness in MCD’s Europe business in recent months, and the ongoing crisis there, we are not holding Europe to a high standard.

NEUTRAL: A print of between 4% and 5% would be received as neutral by investors, in our view, as it would imply some stabilization in two-year average trends.

BAD: A number below 4% would imply a substantial deceleration in two-year average trends.

APMEA - facing a compare of 4.3%, including a calendar shift of between -1.5% and +0.5%, varying by area of the world:

GOOD: A result of 4% or higher would be received as positive by investors as it would imply a significant acceleration in two-year average trends. Yum Brands has been trading poorly in recent days on fears of a slowdown in China sparked by a disappointing PMI number for May. We are still holding APMEA to a high standard given that slowdowns in this metric do not necessarily correspond to a top line deceleration for McDonald’s.

NEUTRAL: A print between 3% and 4% would be received as neutral by investors as it would imply two-year average trends roughly in line or slightly better than those seen in April.

BAD: Comparable restaurant sales growth of less than 3% for the McDonald’s APMEA division would imply a continuation of sluggish two-year average trends.

Howard Penney

Managing Director

Rory Green

Analyst