Conclusion: The results from Wisconsin tonight will be an important leading indicator for President Obama’s chance of winning that State. More broadly, the weak economy continues to lower Obama’s probability of re-election. In our view, a Romney Presidency will be bullish for the U.S. dollar.

Not surprisingly, the Wisconsin election to recall Governor Scott Walker is not without controversy. The current rumor coming from the Democratic Party in Wisconsin is that calls are going to voters from Walker supporters telling prospective voters they do not have to vote if they signed the recall. In fact, Milwaukee County Democratic Chair Sachin Chheda was very explicit in this accusation of cheating and said earlier today:

“This latest lowlife sleaze comes on the heels of countless reports from around the state of various Republican dirty tricks on behalf of Walker. For instance, reports surfaced last weekend that Walker supporters are paying homeowners to post Walker signs on their lawns."

Dirty tricks or not, it appears almost certain that Governor Walker will win the recall vote. According to InTrade, the electronic prediction market, the probability that Walker will get re-elected is at 93%. As the chart below outlines, this is up dramatically since early May when the probability was floating around 50%.

The latest polls from Wisconsin have also validated the InTrade contract. The Real Clear Politics aggregate has Walker +6.7 and the most recent poll from WeAskAmerica has Walker up +12. If these numbers hold, then Walker is poised to beat Barrett by more than the +5 margin he won by in 2010.

From an analytical perspective, Walker’s ability to gain margin in two years can obviously be attributed to his much deeper funding that his competitor. By most estimates, Walker will have outspent Barrett by margin of 8 – 1. But while funding certainly helps, much of the electorate in Wisconsin actually considers itself increasingly conservative, which is leading to more support at the polls for Walker. This shift is in part due to their support of Walker’s key mandate, which is fiscal reform in Wisconsin via limiting the collective bargaining rights of government unions.

As it relates to the broad national sentiment, it is difficult to tell at this juncture what the implications of a victory by a Republican in Wisconsin mean, but certainly if Governor Walker wins by a broader margin, it is an ominous sign for Obama in Wisconsin this fall. Currently Wisconsin represents 10 electoral votes, which will be critical in a tight Presidential race. Wisconsin has typically been considered a safe state for Democrats as Democratic Presidential candidates have won the state every election going back to 1984.

On some level, even if Walker’s victory in Wisconsin isn’t a leading indicator for the national Presidential race, it certainly appears coincident with Romney’s odds improving and Obama’s odds decreasing. According to our Hedgeye Election Index (HEI), President Obama’s re-election chances are down to 54.1%. This is Obama’s lowest reading in five months.

The reading on our proprietary index is consistent with InTrade. Currently President Obama’s probability of getting re-elected on InTrade is down to 53%. This was his lowest reading since February 2012. The most recent precipitous drop occurred in conjunction with the employment report last Friday that showed nonfarm payrolls had added a mere 69,000 jobs in May.

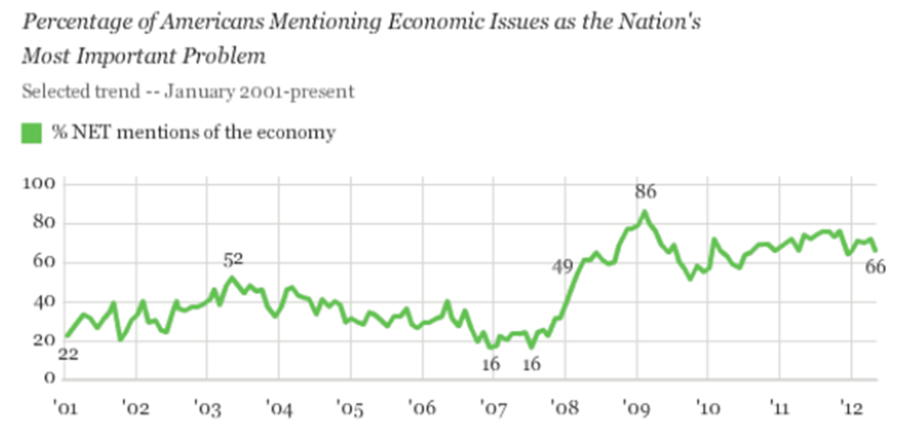

A weak economy is never positive for an incumbent President and, as the data shows, is not good for Obama. In the chart below, we highlight a series of polls from Gallup that highlight that the economy is front and center in the minds of the electorate. This chart shows that over the last four months more than 66% of those polled have highlighted the economy as the most important problem.

To date, President Obama has blamed the current economic woes on former President George W. Bush. Based on a recent Washington Post / ABC poll, 49% of those polled say they blame President Bush and 34% of those polled say they blame Obama. So, on some level the electorate agrees with Obama that it is Bush’s fault. That said, the same poll indicated that 55% of those polled disapproved of the way Obama has handled the economy.

Ultimately this election, as they always are, will be an evaluation of the current administration and not the former one. Base on his broad approval ratings, the Obama administration’s handling of the economy is keeping President Obama’s approval ratings at a level that makes re-election increasingly questionable. The table below highlights the average approval rating of past incumbents in the May of their re-election years. Obama most closely parallels Bush in 2004 and Ford in 1976. In 2004, Bush won the popular vote 50.7% to 48.3% and in 1976 Ford lost 50.1% to 48.0%.

As always, as it relates to the Presidential election, it remains the economy that matters.

Daryl G. Jones

Director of Research