This note was originally published at 8am on May 22, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Organisms that treat threats as more urgent than opportunities have a better chance to survive.”

-Daniel Kahneman

If you only have time to read one chapter of Dan Kahneman’s Thinking, Fast and Slow this summer, I’d go with Chapter 26, Prospect Theory. It helped me bridge some gaps between the fractal dimensions in our models (math) and behavorial factors.

Prospect Theory is a behavioral economic framework that will be much more relevant to the next generation of economists than this one. It will take time to pound the Keynesianism out of our system. Sadly, seeing centrally planned economic systems in Europe and Japan (maybe at some point in the USA) fail, will be the only way to expedite this evolution.

On pages 282-283 of Kahneman’s latest book, you’ll get Prospect Theory both with a simple picture and three bullet points of prose:

1. “Evaluation is relative to a neutral reference point.”

2. “A principle of diminishing sensitivity applies to both sensory dimensions and the evaluation of changes in wealth.”

3. “The third principle is loss aversion… losses loom larger than gains.”

And that brings me right back to the top of this morning’s Early Look quote, to the bottom of your gut feeling at Friday’s lows, and back again to yesterday’s biggest market rip in 2 months. Your Prospects of Survival in this business depend on your process.

Back to the Global Macro Grind …

Losing other people’s money isn’t cool. Losing your own money is even less cool. If you are doing both at the same time, my sense about the matter doesn’t really matter – where your emotions fit on the slope of the loss aversion curve does.

That’s why we bought red on Friday and sold green into yesterday’s close. When it comes to your decisions to buy or sell something, there really are no rules about reversing everything you did in the prior day. I am not Warren Buffett. I am your Risk Manager. The only rules in our profession are self imposed by the institutions who think they are managing our risk.

But what is risk? What are these institutional investing styles? Why are either measures relevant to what’s happening in your portfolio today as opposed to risk measurements and style factors you may have used in 2005-2007?

There are many more questions here than answers. My goal, at the top of every risk management morning, is to Embrace Uncertainty and have markets pick me. The more I try to pick markets, the more risk I impose on myself. What is supposed to work, rarely works. And what shouldn’t happen, usually happens. Either accept that, or whine about it – it’s reality.

I sold my SP500 (SPY) long position yesterday – here’s why:

- Immediate-term TRADE upside resistance into the close = 1329 (so I only had 1% upside left)

- Immediate-term TRADE downside support into the close = 1288 (2% downside makes my risk vs reward 2:1)

- Immediate-term RANGE of risk (3 day probability model) = 89 S&P points (that means volatility will be real)

- US Equity Volatility (VIX) was down -12.3% on the day but holding my TRADE and TREND lines of support

- US Equity Volume was down -17% versus the average volume of last week’s down days

- US Equity Correlation Risk to the US Dollar Index remains wacky elevated at -0.96 (USD vs SPY)

Multi-factor, Multi-duration Risk Management – that’s how I roll. On the immediate-term TRADE duration (3 weeks or less), those were the 6 glaringly obvious reasons to be at least a lot less net long. Catalyst wise, I gave you my calendar ones in yesterday’s note.

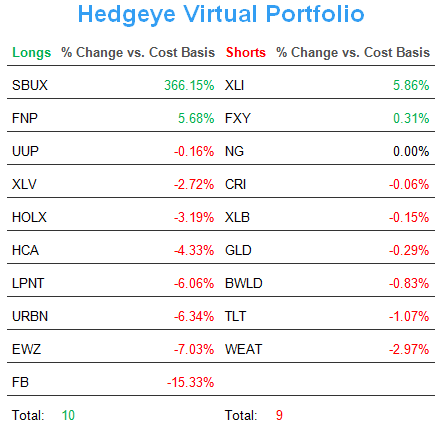

In the Hedgeye Portfolio, we opened the day with 16 LONGS, 4 SHORTS and closed the day with 10 LONGS, 8 SHORTS. That’s easily the most aggressive 1-day swing in what can be considered a proxy for my “net” exposure in 2012.

But was it aggressive? Or wasn’t it aggressive enough? Maybe I should have sold everything and gone to 100% Cash. Maybe I should have shifted to net short. Maybe I shouldn’t have done anything at all.

Maybe I should just stick with the process and take the high probability cut at the ball, and live with it.

And I will.

With the US Dollar Index down for the 2ndday in a row, we bought that long position back yesterday on red. That position is one we have been pounding the pavement on with clients as the most asymmetric long-term long idea in Global Macro (email Sales@Hedgeye.com for Theme #3 in our Q2 Macro Themes called “Asymmetric Risks” and you’ll see the long-term mean reversion case for Strong Dollar).

In addition to the aforementioned Correlation Risk of staying long the SP500 (SPY) in the face of a -0.96 USD/SPY correlation this morning, here’s a refresh of the other big immediate-term USD correlations jumping off the page:

- Commodities (CRB Index) = -0.92

- Euro Stoxx600 = -0.97

- Gold = -0.89

That’s why I re-shorted Gold (GLD) yesterday too.

There’s rain in Connecticut, but Prospects of Survival out there this morning look better than bad.

My immediate-term support and resistance ranges for Gold, Oil (WTIC), US Dollar, EUR/USD, and the SP500 are now $1573-1618, $90.57-94.12, $80.82-81.97, $1.26-1.28, and 1288-1330, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer