TODAY’S S&P 500 SET-UP – June 4, 2012

As we look at today’s set up for the S&P 500, the range is 32 points or -0.79% downside to 1268 and 1.72% upside to 1300.

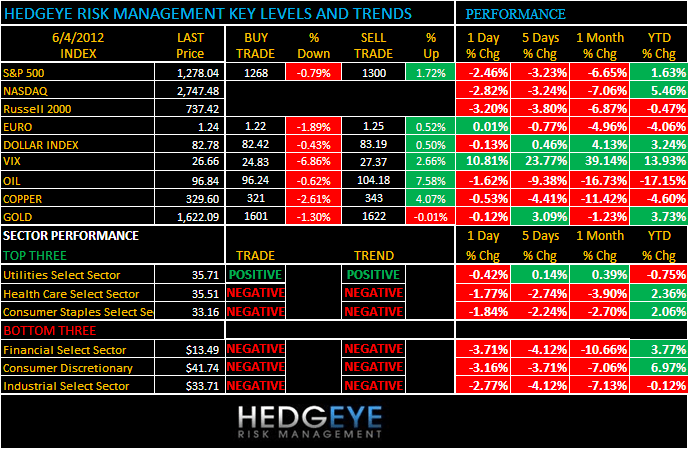

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 6/01NYSE -2193

- Down from the prior day’s trading of -124

- VOLUME: on 6/01 NYSE 999.49

- Decrease versus prior day’s trading of -24.72%

- VIX: as of 6/01 was at 26.66

- Increase versus most recent day’s trading of 10.81%

- Year-to-date increase of 13.93%

- SPX PUT/CALL RATIO: as of 6/01 closed at 2.64

- Up from the day prior at 1.74

CREDIT/ECONOMIC MARKET LOOK:

USA – futures have gone from down 10 to down 3 and, more importantly, bond yields stopped falling – the 10yr is already up 5bps this morning vs Friday’s smack-down close; yield spread 5bps wider on that, which this market direly needs.

- TED SPREAD: as of this morning 41

- 3-MONTH T-BILL YIELD: as of this morning 0.06%

- 10-Year: as of this morning 1.49

- Increase from prior day’s trading at 1.45

- YIELD CURVE: as of this morning 1.24

- Up from prior day’s trading at 1.21

MACRO DATA POINTS (Bloomberg Estimates):

- 9:45am: ISM New York, May (prior 61.2)

- 10am: Factory Orders, Apr. est. 0.2% (prior rev. -1.9%)

GOVERNMENT:

- Pres. Obama attends fundraisers in New York with Bill Clinton

- House, Senate in session

- CFTC adopts Swap Dealer and Major Swap Participant Recordkeeping, Reporting and Duty rules

WHAT TO WATCH:

- EU said to prepare start of perm. bailout fund for July 9

- ASCO conference continues; Conference preview

- Spain calls on Merkel to further protect banks

- Walgreen, Express Scripts agreed to dismiss contract claims

- China non-manufacturing industries expand at slowest pace since March 2011

- ISS recommends AOL shareholders vote for 2 Starboard Value nominees, 6 AOL nominees, as directors

- Wal-Mart to release vote totals after all 16 board members were re-elected on Fri.

- Yahoo, Facebook in talks to end patent disputes: AllThingsD

- EFG-Hermes rejects $1.1b bid to pursue QInvest venture

- Service industries probably kept growing: U.S. econ. preview

EARNINGS:

- Conn’s (CONN) 7am, $0.33

- Dollar General (DG) 4:05pm, $0.60

- Shuffle Master (SHFL) 4:05pm, $0.20

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Hedge Funds in Longest Rout Since Global Recession: Commodities

- Copper Drops to Five-Month Low in New York After Data From China

- Gold Drops as Investors Seek Cash on Equities, Commodities Slump

- Commodities Drop to 18-Month Low as Slowdown Concern Deepens

- China’s Gold Imports From Hong Kong Climb to Record in April

- Speculators Cut Bullish Oil Wagers Before Plunge: Energy Markets

- Natural Gas Rebounds in New York After Drop on Cooler Weather

- Palm Oil Slumps to Seven-Month Low Over Global Growth Concern

- Waterway Petroleum Said to Buy ONGC Naphtha for Loading in June

- Burundi in Talks With Foreign Investors to Boost Power Output

- BP Exit From Russia Venture Seen Risking Investor Return: Energy

- Commodities Slumping as China Sees Weaker Yuan: Chart of the Day

- Nickel May Drop 3.7 Percent on Retracement: Technical Analysis

- Funds in Longest Rout Since World Recession

- Cotton Falls to 31-Month Low on Concern Global Glut Set to Swell

- China’s Easing Grip on Gas Opening Door to North America Exports

- Vitol Said to Buy July-Loading Gasoil From Mangalore Refiners

CURRENCIES

EUROPEAN MARKETS

EUROPE – shorting Spain and Italy on Friday didn’t work – both are green this morning; again, markets discount reality and these markets have been crashing for months, so be careful on the short side until we get the bounces; then study those. IBEX +1.7% this morning and the Euro actually has not moved at 1.24.

ASIAN MARKETS

ASIA – Asian stocks have been going down since Feb/Mar, so last night was more of an immediate-term capitulation more than anything else (Japan down -1.7% = down -19.1% from its March top); interesting that India almost closed flat (given that it was the 1st market to stop going up, it was the 1st to stop going down – for a day).

MIDDLE EAST

The Hedgeye Macro Team