-- For specific questions on anything Europe, please contact me at to set up a call.

No Current European Positions in the Hedgeye Virtual Portfolio

Asset Class Performance:

- Equities: The STOXX Europe 600 closed down -3.05% week-over-week vs +1.5% last week. Bottom performers: Spain -7.3%; Romania -6.4%; Finland -5.0%; Germany -4.6%; Denmark -4.6%; Portugal -4.1%; Austria -3.7%. Top performers: Greece +3.4%; MICEX +1.4%; Poland +1.2%; Hungary +0.3%.

- FX: The EUR/USD is down -0.83% week-over-week vs -2.01% last week. W/W Divergences: RUB/EUR -4.12%, HUF/EUR -1.74%, CZK/EUR -1.56%, GBP/EUR -1.24%, NOK/EUR -1.06%, PLN/EUR -0.93%.

- Fixed Income: Another crazy week of swings in yields. Germany hit record lows on the 10YR at 1.17%!!! Greece’s 10YR climbed for yet another week (big surprise!), gaining +17bps week-over-week to 30.69%. Portugal gained +5bps to 11.98%. Belgium saw the biggest weekly decline at -17bps to 2.82%, followed by France -12bps to 2.26% and Italy -12bps to 5.74%, as Germany dropped -11bps. On a month-over-month basis, the Greek 10YR yield is up a monster +1038bps!, while France fell -71bps and Germany fell -49bps over the period.

He said, She said:

In recent weeks we’ve worked hard to contextualize the ever-changing and moving parts in Europe under the assumption that to size up potential outcomes for Europe one must recognize that what Eurocrats “should” do (from a economic policy perspective) may be very different from what they “will” do. We’d direct you to our recent European Monitors titled “On Why Greeks Shouldn’t Leave the Eurozone/EU” on 5/18 and “Hold Your Horses on Greek Exit” on 5/25 for our thinking on the larger issues surrounding a Greek exit. [Email me at if you need a copy].

Our main update for this week is to stress that we believe much hinges on the Greek elections on June 17th. [Note that our EUR/USD is updated below]. Given the runway until then, we expect more stoking of the rumor mill, plenty of political foot in mouth syndrome, and market swings over even the slightest of comments from key Eurocrats. We see—short of an overnight Greek bank-run—a strong likelihood that no concrete proposals (either Eurobonds, a Pan-European Deposit Guarantee facility, and/or another LTRO) will be issued before elections. We expect Eurocrats, directed by German Chancellor Merkel, to play the card that while fiscal consolidation targets may be grossly ambitious, an all-out rejection of austerity from a government is an unacceptable position, especially for a country like Greece that is receiving bailout money conditional to its austerity program. Therefore, the call is being put to the Greeks to vote in a pro-austerity party (likely a coalition of New Democracy) versus the anti-austerity camp of Syriza.

The latest collection of Greek party polls show a mixed picture, largely showing a single digit spread with both Syriza and New Democracy receiving the favor based on the poll. This mismatch is maybe best demonstrated by a poll out today from Kathimerini showing Syriza garnering 31.5% of the vote if held today versus 25.5% for New Democracy; however the poll also noted that 58% believe New Democracy will come in first and only 34% see Syriza winning. Go figure!

Importantly, it’s worth noting that the last Greek opinion poll will be this Sunday, June 3rd, and therefore we’ll largely be in the dark from a sentiment polling perspective ahead of June 17th.

As Greece remains in the crosshairs over the next weeks, we expect talks to heat up on the ESM, the €500B bailout packages expected to come online on July 1stand work in concert with the remaining EFSF, and in particular to discuss adding clauses that explicitly define how it can be used to recapitalize European banks.

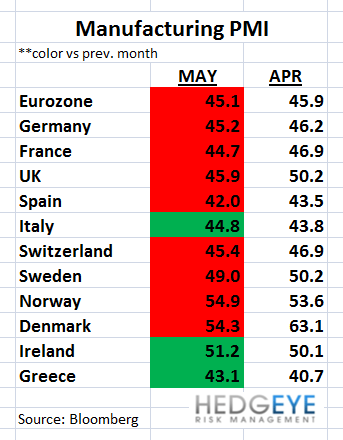

Meanwhile, we saw quite a week of weak data, namely in mostly bombed out PMI Manufacturing figures in MAY vs APR; weaker confidence figures across the region; Eurozone unemployment elevating to a 17 year high of 11.0%. One bright spot was CPI, which came in 20bps lower at 2.4% in May Y/Y versus 2.6% in April. (See the Data Dump section below for more).

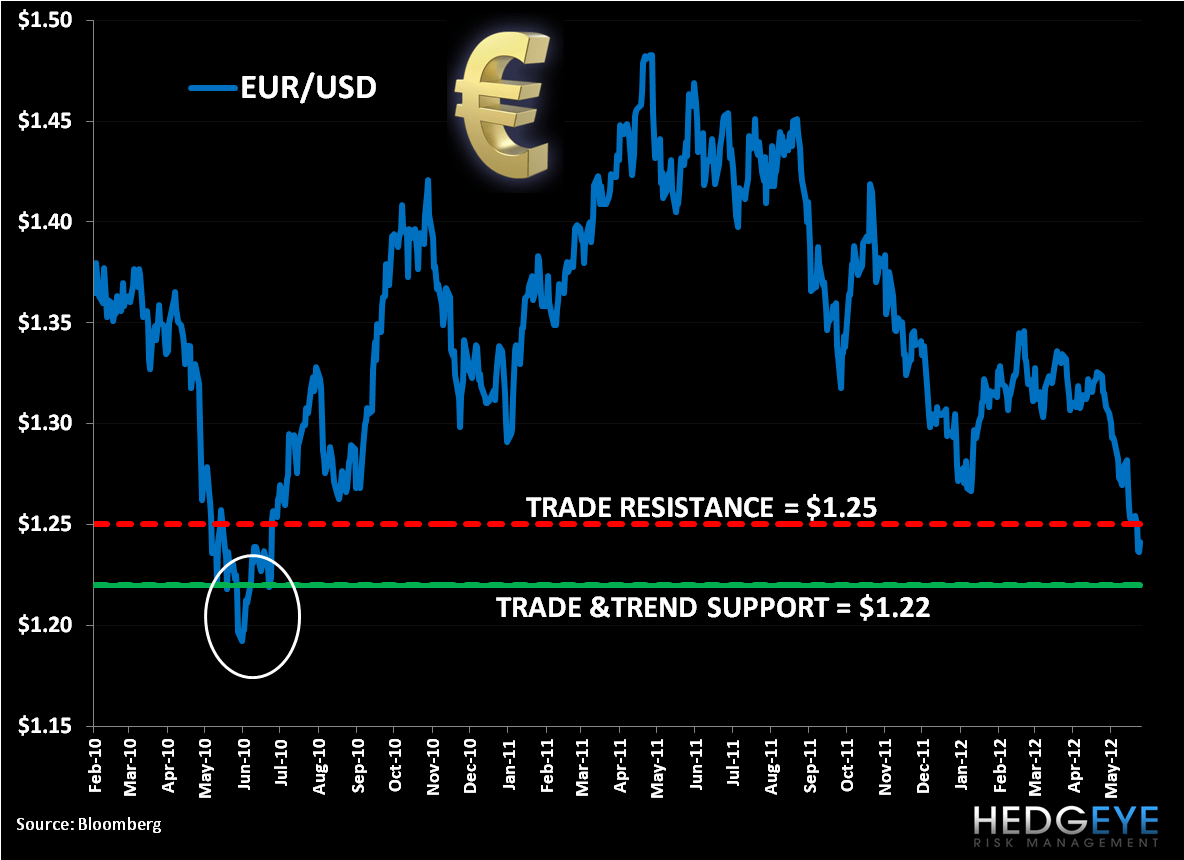

EUR-USD:

Below is an updated EUR/USD price level chart. Our immediate term TRADE and intermediate term TREND levels of support are both at $1.22. Our TRADE resistance level is $1.25. Our call remains that if $1.22 breaks, look out below! We’re not EUR parity folks because we see Eurocrats stepping in to prevent it, however the runway of uncertainty until June 17thelections puts significant downside risk in play. However, we’re well cognizant that the pair could see a bounce on any optimism around discussions concerning any number of proposals on the table, including: Eurobonds, a Pan-European Deposit Guarantee facility, another LTRO, and the ESM.

Call Outs:

Finland anti Eurobonds - Finnish Prime Minister Jyrki Katainen said in a speech that he was against taking on a bigger financial burden to help address the sovereign debt crisis in Europe. He noted that the government's stance on Eurobonds has been "extremely critical or negative".

Irish say Yes - Ireland approves the Fiscal Compact by a vote of 60.2% to 39.8%.

ECB and LTRO - ECB Governing Council member Ignazio Visco said that the central bank has not ruled out a third longer-term refinancing operation. However, he added that another LTRO is not necessary at the moment given that there is no liquidity problem. Visco, like ECB President Draghi, also argued that the ESM should be allowed to directly recapitalize troubled banks.

Greece - Euler Hermes, the world’s biggest credit insurer, said it will no longer cover new shipments of goods to Greece due to concerns about the country leaving the euro and customers defaulting on payments, which raises the prospect that certain goods will no longer reach Greek companies and stores. Recall Austria’s OeKB Versicherung said earlier this week that it will also drop coverage of new shipments to Greece, while Coface of France said it is only doing business with “the healthiest Greek companies.”

Rehn and Eurobonds - EU Economic and Monetary Affairs Commissioner Olli Rehn told a conference that the euro needs to be underpinned by closer cooperation between member countries to survive and prosper. However, he added that going straight to a discussion about Eurobonds would be a "false debate", as countries first need to bring budgetary policies more into line and move towards a fiscal union.

Draghi on the Eurozone - ECB President Mario Draghi urged Eurozone leaders to intensify their efforts to combat the crisis, noting that the central bank cannot fill the vacuum of the lack of action by national governments on fiscal growth, nor can it fill the vacuum of their lack of action on structural problems. On the banking front, Draghi said a banking union would need to be supervised centrally and require the introduction of a European deposit scheme and resolution fund. He also said that when it comes to recapitalizations, "it is better to err by too much in the very beginning rather than by too little

Eurozone Club Membership - The European Central Bank (ECB) has said that none of the eight countries that are supposed to join the euro are ready yet. The countries include: Bulgaria, the Czech Republic, Latvia, Lithuania, Hungary, Poland, Romania, and Sweden.

CDS Risk Monitor:

Week-over-week CDS were largely up. Spain saw the largest gain in CDS w/w at +70bps to 606bps, followed by Italy +63bps to 571bps, France +15bps to 219bps. Portugal was the sole decliner of the countries we track at -18bps to 1177bps.

Data Dump:

Eurozone Unemployment Rate 11% APR [17 year high] vs 10.9% MAR revised to 11%

Eurozone Business Climate Indicator -0.77 MAY (exp. -0.67) vs -0.51 APR

Eurozone Consumer Confidence -19.3 MAY Final (-19.3 initial) vs -19.9 APR

Eurozone Economic Confidence 90.6 MAY (exp. 91.9) vs 92.9 APR

Eurozone Industrial Confidence -11.3 MAY (exp. -10.2) vs -9.0 APR

Eurozone Services Confidence -4.9 MAY (exp. -2.8) vs -2.4 APR

Eurozone CPI 2.4% MAY Y/Y (exp. 2.5%) vs 2.6% APR

Eurozone M3 2.5% APR Y/Y vs 3.1% MAR

Germany CPI 2.1% MAY Prelim. Y/Y (exp. 2.2%) vs 2.2% APR [-0.3% MAY Prelim. M/M (exp. 0.0%) vs 0.1%]

Germany Unemployment Rate 6.7% MAY vs 6.8% APR

Germany Unemployment Chg 0K MAY vs 18K APR

Germany Retail Sales -3.8% APR Y/Y (exp. 0.3%) vs 3.2% MAR [0.6% APR M/M (exp. 0.2%) vs 1.6% MAR [sales increased for second straight month]

Germany Import Price Index 2.3% APR Y/Y (exp. 2.6%) vs 3.1% MAR [-0.5% APR M/M vs 0.7% MAR]

France Producer Prices 2.7% APR Y/Y vs 3.7% MAR

France Consumer Spending 0.4% APR Y/Y vs -1.7% MAR

UK Nationwide House Prices -0.7% MAY Y/Y vs -0.9% APR [0.3% MAY M/M (exp. 0.1%) vs -0.3% APR (1st rise in 3 months)]

UK GfK Consumer Confidence -29 MAY (exp. -32) vs -31 APR (1st positive number in 4 months)

UK M4 Money Supply -3.8% APR Y/Y vs -4.8% MAR

Italy CPI 3.5% MAY Prelim. Y/Y vs 3.7% APR

Italy Unemployment Rate 10.2% APR Prelim (highest in 12 years!!) vs 10.1% MAR

Italy PPI 2.5% APR Y/Y vs 2.8% MAR

Italy Business Confidence 86.2 MAY vs 89.1 APR

Spain Total Housing Permits -27.8% MAR Y/Y vs -36.2% FEB

Spain CPI 1.9% MAY Prelim Y/Y vs 2.0% APR

Spain Retail Sales -11.3% APR Y/Y vs -4% MAR

Switzerland Retail Sales 0.1% APR Y/Y vs 4.7% MAR

Switzerland KOF Swiss Leading Indicator 0.81 MAY (exp. 0.40) vs 0.43 APR

Switzerland Q1 GDP 0.7% Q/Q (exp. 0.0%) vs 0.5% in Q4 [2.0% Y/Y (exp. 0.7%) vs 2.0% in Q4]

Sweden Q1 GDP 1.5% Y/Y (exp. 0.9%) vs 1.0% in Q4 [0.8% Q/Q vs -1.0% in Q4]

Sweden Consumer Confidence 5.9 MAY vs 4.7 APR

Sweden Manufacturing Confidence 0 MAY vs -1 APR

Sweden Economic Tendency Survey 100.9 MAY vs 101.5 APR

Sweden Household Lending 4.8% APR Y/Y vs

Sweden Retail Sales NSA 0.8% APR Y/Y vs 4.2% MAR

Norway Manufacturing Wage Index 0.7% in Q1 Q/Q vs 1.4% in Q4

Norway Unemployment Rate 2.3% MAY vs 2.6% APR

Norway Retail Sales -3.7% APR Y/Y vs 9.6% MAR

Norway Consumer Confidence 22.4 in Q2 vs 17 in Q1

Norway Unemployment Rate 3% MAR vs 3.2% FEB

Finland Business Confidence -12 MAY vs -2 APR

Finland Consumer Confidence 12 MAY vs 10.4 APR

Denmark Q1 GDP 0.3% Q/Q (exp. 0.0%0 vs -0.2% in Q4 [0.2% Y/Y (exp. 0.2%) vs 0.4% in Q4]

Austria PPI 1.1% APR Y/Y vs 1.4% MAR

Belgium Unemployment Rate 7.4% APR vs 7.3% MAR

Belgium CPI 2.81% MAY Y/Y vs 3.18% APR

Greece Retail Sales -15.1% MAR Y/Y vs -11% FEB

Ireland Retail Sales -2.7% APR Y/Y vs -0.9% MAR

Ireland Unemployment Rate 14.3% MAY vs 14.3% APR

Portugal Retail Sales -9.0% APR Y/Y vs -4.5% MAR

Portugal Industrial Production -7.4% APR Y/Y vs -4.7% MAR

Portugal Consumer Confidence -52.6 MAY vs -53.3 APR

Portugal Economic Climate Indicator -4.6 MAY vs -4.7 APR

Hungary Economic Sentiment -24.9 MAY vs -19.3 APR

Hungary Business Confidence -14 MAY vs -9 APR

Hungary Consumer Confidence -55.9 MAY vs -48.8 APR

Interest Rate Decisions:

(5/29) Turkey Benchmark Repo Rate UNCH at 5.75%

(5/29) Hungary Base Rate UNCH at 7.00%

The Week Ahead:

Sunday: Final Opinion Polls for the Greek Election

Monday: Apr. Eurozone PPI

Tuesday: May Eurozone PMI Composite and Services - Final; Apr. Eurozone Retail Sales; May Germany PMI Services - Final; Apr. Germany Factory Orders; May UK BRC Shop Price Index, Lloyds Business Barometer; May France PMI Services – Final; Spain PMI; Italy PMI Services;1Q Finland GDP

Wednesday: ECB Interest Rate Decision; 1Q Eurozone GDP, Household Consumption, Gross Fix Cap, Government Expenditure – Preliminary; Apr. Germany Industrial Production; May UK PMI Construction, BRC Sales Like-For-Like, Halifax House Prices (June 6-8); Apr. Spain Industrial Output

Thursday: UK BoE Asset Purchase Target and Announces Rate; May UK PMI Services, Official Reserves; 1Q France Unemployment Rate; Mar. Greece Unemployment Rate

Friday: Apr. Germany Exports, Imports, Current Account, Trade Balance; May UK BoE/GfK Inflation Expectation Survey, PPI Input and Output, New Car Registrations, Consumer Price Index; 1Q UK GDP – Final; Apr. France Central Government Balance, Trade Balance; Apr. Italy Industrial Production; Apr. Greece Industrial Production

Extended Calendar Call-Outs:

JUNE: Greece to Identify 5.5% of GDP in Austerity Measures

10 June: France – first round of parliamentary elections

14 June: Eurogroup Meeting

15 June: G20 Summit of Finance Ministers

17 June: Greece – probable date for next general election, France – second round of parliamentary election

18-19 June: G20 Summit in Los Cabos, Mexico

20-21 June: Eurogroup Meeting; Ecofin Meeting in Luxembourg

22 June: Greek T-Bill Redemption for 1.3 Billion EUR

28-29 June: EU Summit in Brussels, aim to formally sign off on growth proposals; EC meets to discuss Institutional Affairs

30 June: Deadline for EU Banks to meet €106B capital target/the 9% Tier 1 capital ratio, Iceland – Presidential election

JULY: France – extraordinary session of parliament in July is due to re-draft the 2013 budget

1 July: ESM to come into force

5 July: ECB governing council meeting

19 July: ECB governing council meeting

18-19 October: Summit of EU Leaders

Matthew Hedrick

Senior Analyst