TODAY’S S&P 500 SET-UP – June 1, 2012

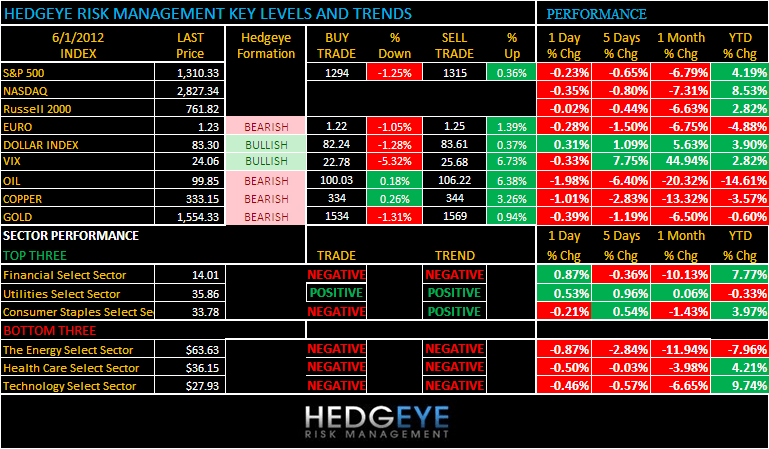

As we look at today’s set up for the S&P 500, the range is 21 points or -1.25% downside to 1294 and 0.36% upside to 1315.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 5/31 NYSE -124

- Up from the prior day’s trading of -2264

- VOLUME: on 5/31 NYSE 1327.72

- Increase versus prior day’s trading of 72.73%

- VIX: as of 5/31 was at 24.06

- Decrease versus most recent day’s trading of -0.33%%

- Year-to-date increase of 2.82%

- SPX PUT/CALL RATIO: as of 05/31 closed at 1.74

- Down from the day prior at 2.35

CREDIT/ECONOMIC MARKET LOOK:

#GrowthSlowing – pick your high-frequency data pt this week from the bomb of Pending US Home Sales (-5.5% Apr) to yesterday’s US PMI of 52 (down -7.4% vs last month) to South Korean exports being negative in May (3rd consecutive month of y/y declines) to UK PMI of 45.9 in May (vs 50.5 in April); the concept of “de-coupling” is as dead as Keynes in 2012.

- TED SPREAD: as of this morning 40

- 3-MONTH T-BILL YIELD: as of this morning 0.06%

- 10-Year: as of this morning 1.53

- Decrease from prior day’s trading at 1.56

- YIELD CURVE: as of this morning 1.28

- Down from prior day’s trading at 1.30

MACRO DATA POINTS (Bloomberg Estimates):

- 8:30am: Nonfarm Payrolls, May, est. 150k (prior 115k)

- 8:30am: Unemployment Rate, May, est. 8.1% (prior 8.1%)

- 8:30am: Avg Hourly Earning (M/m), May, est. 0.2% (prior 0.0%)

- 8:30am: Avg Weekly Hours, May, est. 34.5 (prior 34.5)

- 8:30am: Personal Income, Apr., est. 0.3% (prior 0.4%)

- 8:30am: Personal Spending, Apr., est. 0.3% (prior 0.3%)

- 8:30am: PCE Core (M/m), Apr., est. 0.2% (prior 0.2%)

- 8:58am: Markit US PMI (final), May, (prior 53.9)

- 10am: ISM Manufacturing, May, est. 53.8 (prior 54.8)

- 10am: ISM Prices Paid, May, est. 57 (prior 61)

- 10am: Construction Spending (M/m), Apr., est. 0.4% (prior 0.1%)

- 1pm: Baker Hughes rig count

GOVERNMENT:

- Senate not in session, House meets at 9am

- Former Fla. Gov. Jeb Bush testifies at House Budget hearing

- House Financial Svcs. panel holds hearing on cyber threats to capital markets, corporate accounts, 9:30am

WHAT TO WATCH:

- Payrolls in U.S. probably picked up from smallest gain in 6m

- Toyota, Honda may post biggest rises in monthly auto sales

- Euro-area unemployment reaches record 11% led by Spain, Italy

- China manufacturing expands at weakest pace since Dec.

- Disney names ex-Warner executive as film operation chairman

- Wal-Mart holds its annual meeting today

- ASCO conference this weekend; watch for data on J&J’s Zytiga

- Goldman CEO Blankfein to be witness at Gupta’s trial, U.S. says

- BP to pursue sale of $20b stake in Russian producer TNK-BP

- Thomas H. Lee Partners said to be in lead to buy Party City

- Acer, Toshiba said to unveil Windows 8 tablets to challenge IPad

- German note yield drops below zero for first time

- Liberty tells regulators it wants control of Sirius XM radio

- Google loses court case to dismiss claims over digital books

- Bernanke, China Inflation, Diamond Jubilee: Week Ahead June 2-9

EARNINGS:

- No major earnings reports scheduled for today

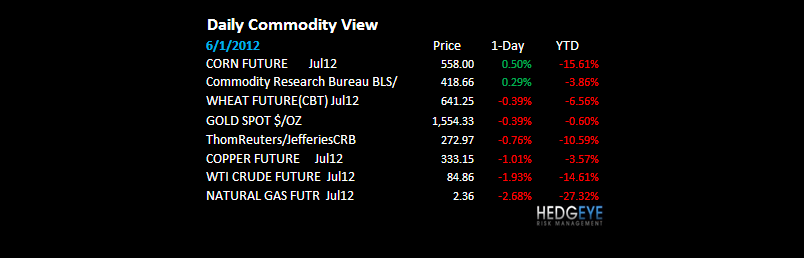

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

Bernanke’s Bubbles – this remains our short Commodities (long Dollar) call for Q2; oil is capitulating to immediate-term TRADE oversold this morning ($84.68 WTIC), but oil is also crashing (down -23% from the Feb high). There are plenty of large exposures to Oil, Gold, etc in the asset management community to be very aware of here.

- Mittal’s Price Squeezed in $960 Billion Steelmaking: Commodities

- Brent Oil Falls Below $100 a Barrel for First Time Since October

- Gold Falls in London as Stronger Dollar Curbs Investor Demand

- Copper Falls Amid Signs European Crisis Is Hurting Economies

- Commodities Drop to Lowest Level Since October on China, Europe

- Copper Bears Rise to Eight-Month High as Hedge Funds Bet on Drop

- Commodity Revenues at Top Banks Decline as Volatility Drops

- BP to Pursue Sale of TNK-BP Shares as Billionaire Partners Bid

- China’s Lead-Battery Exports May Fall as Output Capacity Cut

- Palm Oil Slumps to Five-Month Low as Chinese Demand Set to Fall

- LME Said to Get Assurance From Bidders on Keeping U.K. Base

- Barry Callebaut Says Cocoa Bean Processing May Decline in Europe

- Corn Futures to Extend Slump to 20-Month Low: Technical Analysis

- Commodities Extend Fall on China Slowdown

- China May Resume Nuclear Plant Approvals as Cabinet Passes Plan

- Rubber Falls to Six-Month Low as China’s Output Decelerates

- Thailand, Indonesia Agree Steps Needed to Halt Rubber Decline

CURRENCIES

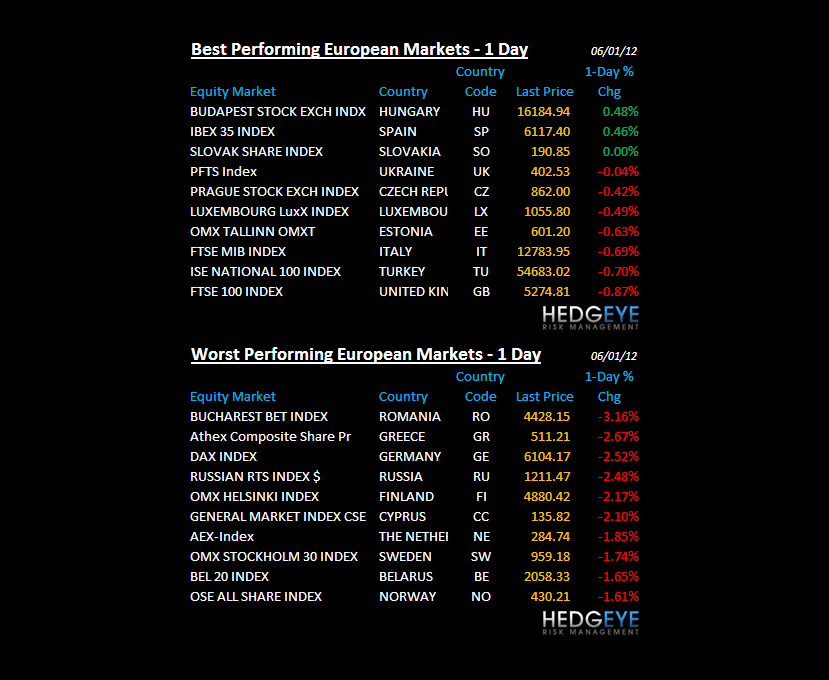

EUROPEAN MARKETS

ASIAN MARKETS

CHINA – we sold our China long position last month because our research was signaling an immediate-term acceleration in China’s growth slowing pattern; this morning’s PMI of 50.4 (vs 53.3 in April) confirms that – all of Asia was weak (has been since Feb/Mar), and consensus is now forced to agree.

MIDDLE EAST

The Hedgeye Macro Team