Conclusion: We’re the low on the Street and are calling for the first miss since VRA went public. But the reality is that a company at VRA’s stage in its lifecycle can print what it wants to. Sentiment is poor, and the stock is off 44% over 2 months. If they pull one out of a hat after the close, it will allow us to get heavier on one of our favorite shorts.

We remain very negative on VRA. We’re We’re the low on the Street at $0.27 vs. the consensus at $0.29E for Q1, suggesting the first miss in the six quarters it has been public. That said, the stock is down 44% in 2 months, and though the Sell-side uniformly likes it with a 73% buy ratio, short interest is still sitting at 47% of the float. In other words, our model BETTER be right, otherwise this stock is going up on the print. A company at this stage in its growth cycle has so many moving parts, and the reality is that it can print (for a short time) pretty much what it wants to print. If the results are ‘in-line’ or better, this stock probably goes up. That’s when we get heavier again on one of our key shorts.

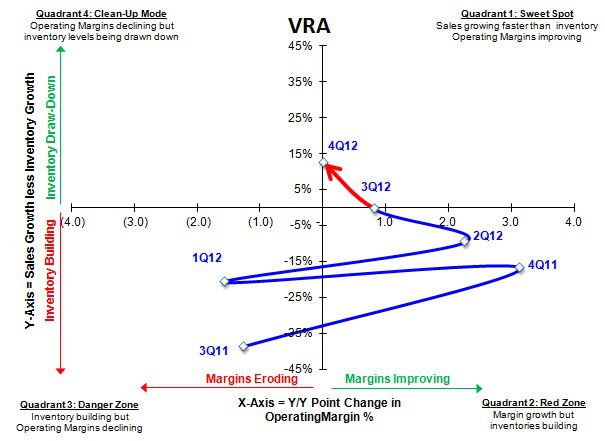

Our TAIL view (3-Years or Less) on VRA is that the company is that it is overextending the reach of its brand as it executes its growth strategy the wrong way. There’s nothing wrong with growing by any means. But the focus is too heavy on channel distribution as opposed to coming up with ‘must have’ product and brand messaging that will make the consumer claw over one another to get that product come hell or high water. Today VRA is sitting at nearly a 21% EBIT margin, and the consensus is looking for that to be up 100bps over the next two years. Call us perma-cynics, but we have yet to see any brand – ever – that has invested heavily in channel distribution above all else (as opposed to R&D and marketing) and has not seen severe swings in its margin structure. It’s easy to sit there and tweak a model thinking that maybe the Street is high or low by 25 or 50bps. But the real call is if margins are 10% in 2 years. Think that can’t happen? Pull up margin charts for TRLG, ANF, AEO, COLM, CROX…heck, even look at VRA. It is up nearly 2x from 11% just 3 years ago. Margins move in big steps in this space, my friends.

While the company simultaneously grows wholesale and retail with product that is largely like for like (a retail no no) it is also looking to expand into Japan, land another national department store account (they are partnered only with DDS). VRA is also doubling the size of its DC, which requires incremental investment. That’s great…we’ll never beat a company up for investing. But it will need to work out the kinks, and will ultimately need to grow into this new capacity.

It’s unlikely these efforts are enough to offset the declining core wholesale business as it becomes cannibalized by VRA’s own retail stores. Moreover, we need to remember that when retail and wholesale growth coincide – and in a way that is not prudent – it is not a pleasant process. We’re not talking about a slow ebb/flow of product orders at wholesale. The timing of these events is impossible to forecast. But we think we’ll see it. With a higher expense base, we expect margin contraction ahead for VRA and are 20% below Street expectations next year (F13). Our bias on our numbers is to the downside.

One risk to a short, and a very big one at that, is if VRA strikes a deal with Ron Johnson and team at JC Penney to do a shop in shop for the Vera Bradley brand in the 700 JCP stores that are being refurbished. That would be such a meaningful channel fill event that it would take up earnings – and margins – presuming the company let it flow through. That does not change the fact that there are 3,400 small wholesale accounts that probably be miffed that the brand is now in JCP. Managing that at a local level would be ‘less than pleasant’ for VRA. It would be one of those near-term positives that turns into a very large longer-term problem.