TODAY’S S&P 500 SET-UP – May 30, 2012

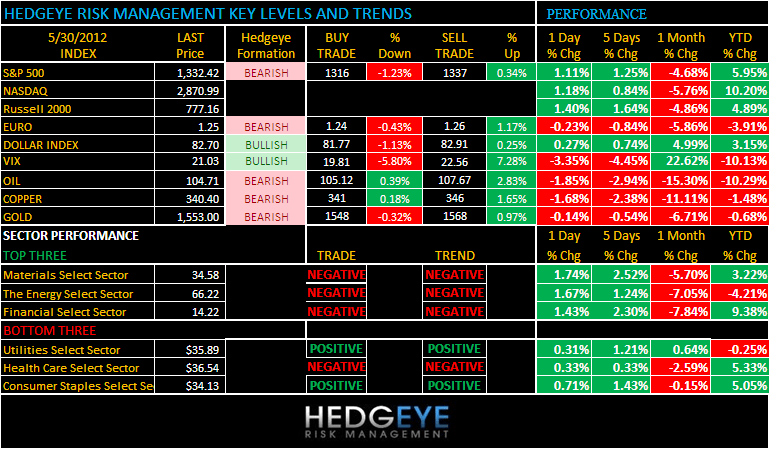

As we look at today’s set up for the S&P 500, the range is 21 points or -1.23% downside to 1316 and 0.34% upside to 1337.

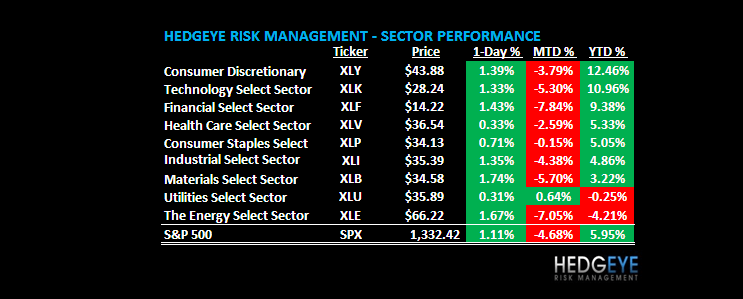

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 5/29 NYSE 1709

- Up from the prior day’s trading of 114

- VOLUME: on 5/29 NYSE 714.24

- Increase versus prior day’s trading of 19.91%

- VIX: as of 5/29 was at 21.03

- Decrease versus most recent day’s trading of -3.35%

- Year-to-date decrease of -10.13%

- SPX PUT/CALL RATIO: as of 05/29 closed at 1.71

- Down from the day prior at 2.03

CREDIT/ECONOMIC MARKET LOOK:

GROWTH – 1st Commodities, then Bonds, and now Stocks getting it; the Old Wall’s economists do not, yet – but they will; we’ve yet to see Hyman or Hatzius cut their US GDP Growth estimates to where we or the bond market has them (1.7-1.9% US GDP is our best case, for now). Looking for that consensus capitulation, blaming Europe.

- TED SPREAD: as of this morning 39

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.68

- Decrease from prior day’s trading at 1.74

- YIELD CURVE: as of this morning 1.40

- Down from prior day’s trading at 1.46

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Applications, week of May 25

- 7:45am/8:55am: ICSC/Redbook weekly sales

- 10am: Pending Home Sales (M/m), Apr., est. 0.0% (prior 4.1%)

- 10am: Pending Home Sales (Y/y), Apr., est. 22.0% (prior 10.8%)

- 11am: Fed to purchase $4.5b-$5.25b notes in 8/15/2020 to 5/15/2022 range

- 11:30am: U.S. to sell $25b 52-week bills

- 11:30am: U.S. to sell 4-week bills

- 1:20pm: Fed’s Fisher speaks on economy in San Antonio, Texas

- 1:30pm: Fed’s Dudley to speak on regional economy in New York

- 4:30pm: Fed’s Rosengren speaks in Worcester, Mass

- 5pm: API weekly petroleum inventories

GOVERNMENT:

- House returns to work following recess; Senate out until Jun 4

- President Obama signs U.S. Export-Import Bank reauthorization

- Commerce Dept. announces level of wind tower import tariffs

- Mitt Romney wins Texas, giving him enough delegates to clinch Republican nomination

WHAT TO WATCH:

- Euro-area economic confidence dropped more than est. in May

- America Movil discussed cooperation with KPN before offer

- Spain’s Ordonez says Bankia bailout terms still unknown

- Pep Boys terminates $1b merger with Gores Group

- Fiat to list in NY after CNH unit merger

- Apple’s CEO says focus is TV, sees closer Facebook ties

- Euro-area loans grew at slowest pace in 2 yrs. in April

- Atlantic Broadband said to seek $1.4b sale

- RIM shares plummet after surprise 1Q op loss

- BankAtlantic must face SEC disclosure fraud lawsuit

- Facebook’s Zuckerberg drops off Billionaires Index

EARNINGS:

- Fresh Market (TFM) 6am, $0.36

- Yingli Green (YGE) 6am, $(0.22)

- CorVel (CRVL) 6:15am

- Booz Allen Hamilton (BAH) 7am, $0.40

- Daktronics (DAKT) 7am, $0.03

- RBC Bearings (ROLL) Bef-mkt, $0.63

- TiVo (TIVO) Aft-mkt, $(0.16)

- Lions Gate Entertainment (LGF) Aft-mkt, $0.22

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Marubeni Follows Glencore to Boost Grain Trading: Commodities

- Brent Falls to 5-Month Low as U.S. Supplies Seen at 22-Year High

- Gold Falls a Second Day as Europe’s Debt Crisis Boosts Dollar

- Copper Drops as Spain’s Credit Rating Revives Crisis Concern

- Wheat Slides as U.S. Harvest Accelerates While Soybeans Decline

- Cocoa Falls as Ivory Coast’s Mid-Crop Harvesting Gathers Pace

- Felda Said to Seek $3.2 Billion in Year’s Second-Biggest IPO

- Iraq Begins First Oil, Gas Exploration Auction Since Saddam Era

- Japan Aluminum Buyers Said to Agree to Record Quarterly Fee

- Standard & Poor’s GSCI Index Drops to Lowest Since October

- Dollar’s Gold Backing Drops With Metal’s Price: Chart of the Day

- Pakistan Seen Shipping 100,000 Tons Sugar by September on Prices

- ONGC Plans Shale, Deepwater Strategy in Bid to Double Production

- Oil Drops as U.S. Stockpiles Seen Rising

- Rubber Inventory Climbing in China as Slowdown Cuts Demand

- Rubber Drops as Rising Thai Supply Adds to Chinese Stockpiles

- Palm Oil Set for Worst Monthly Loss Since 2009 on China Outlook

CURRENCIES

EUROPEAN MARKETS

SPAIN – still crashing. IBEX down another -1.4% (immediate-term TRADE oversold) to a fresh new low (down -31% from the Feb top when Global Growth Slowing became readily apparent in our models); Russia down -27% from the March top and Italian bond yields ripping a move > 6.00% this morning; there is no “de-coupling” from this.

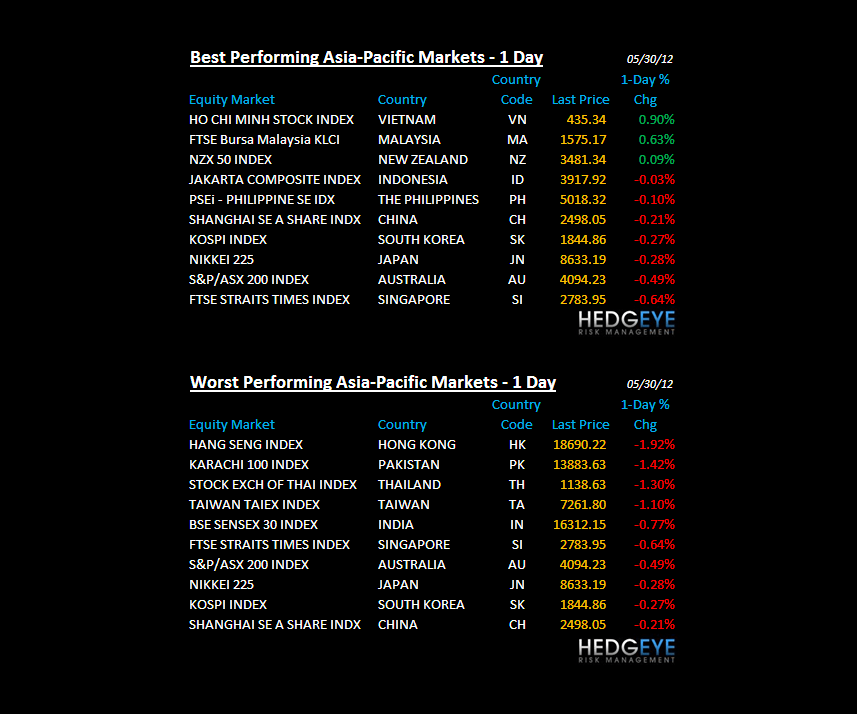

ASIAN MARKETS

CHINA – but the rumors of Chinese stimulus have, at least for today; the Shanghai Comp backed off at an important TRADE line of resistance (2393) last night and the Hang Seng got crushed again, down -1.9% - no follow through from the USA day of no volume US Equity buying (US volumes down -26% vs our composite avg of the down days in May).

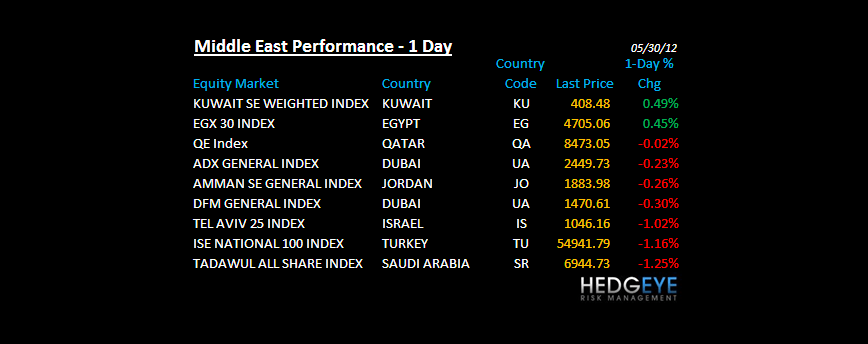

MIDDLE EAST

The Hedgeye Macro Team