TODAY’S S&P 500 SET-UP – May 29, 2012

As we look at today’s set up for the S&P 500, the range is 39 points or -1.66% downside to 1296 and 1.30% upside to 1335.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 05/25 NYSE 114

- Down from the prior day’s trading of 512

- VOLUME: on 05/25 NYSE 595.63

- Decrease versus prior day’s trading of -25.22%

- VIX: as of 05/25 was at 21.76

- Increase versus most recent day’s trading of 1.02%

- Year-to-date decrease of -7.01%

- SPX PUT/CALL RATIO: as of 05/25 closed at 2.03

- Up from the day prior at 1.24

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 39

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.72

- Decrease from prior day’s trading at 1.74

- YIELD CURVE: as of this morning 1.43

- Down from prior day’s trading at 1.45

MACRO DATA POINTS (Bloomberg Estimates):

- 9am: S&P/CS 20-city (M/m), Mar., est. 0.2%, prior 0.15%

- 9am: S&P/CS Home Price Index, Mar., est. 134.4, prior 134.2

- 10am: Consumer confidence, May, est. 69.5, prior 69.2

- 10:30am: Dallas Fed manuf. activity, May, est. 1.5, prior -3.4

- 11:30am: U.S. to sell $30b 3-mo., $27b 6-mo. bills

GOVERNMENT:

- 10am: Defense Secretary Panetta speaks at Naval Academy Commencement ceremony

- 3:25pm: President Obama to award Presidential Medals of Freedom to Bob Dylan, Toni Morrison, John Glenn, others

- Supreme Court issues opinions

- Texas Republican primaries; Romney may get enough votes to push him past the 1,144 needed to clinch nomination

WHAT TO WATCH:

- Marubeni to buy grain merchandiser Gavilon for $3.6b

- Dewey & LeBoeuf files Chapter 11 bankruptcy

- Vale sells Colombian coal assets to Goldman for $407m

- South Korean manufacturer confidence falls from 9-month high

- CP Railway strike may end in three days, Canada’s Raitt says

- Spain may use debt instead of cash to support Bankia Group

- Greek fund distributes EU18b to country’s 4 biggest banks

- Italy borrowing costs rise at 6-mo. bill auction

- Richard Li may be bidder for ING Asia insurance unit: WSJ

- TNK-BP’s Fridman quits as CEO, deepening dispute

- Moody’s says China growth collapse may hurt sovereign rating

- Weekly agendas for energy, real estate, media/entertainment, consumer, industrials, health, finance, tech, rates, Canada oil & gas, Canada mining

- U.S. Jobs, Chinese Output, Panetta: Week Ahead May 28-June 2

EARNINGS:

- Sanderson Farms (SAFM) 6:30am, $0.90

- Bank of Nova Scotia (BNS CN) 7:30am, C$1.15

- Copart (CPRT) After-mkt, $0.43

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

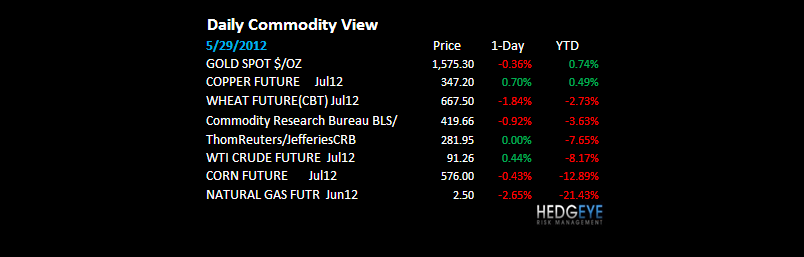

- Platinum Glut Diminishing as Bear Market Approaches: Commodities

- Copper Slips to $7,684 a Ton, Erasing Advance; Aluminum Drops

- China Agrees to Fund $3 Billion of Farming Projects in Ukraine

- Oil Advances for a Third Day on Outlook for U.S. Economic Growth

- Gold Declines as Investors Favor Dollar Amid European Crisis

- Wheat Drops as Rain From Russia to Australia Boosts Crop Outlook

- Gold Recycling in India to Jump as Near-Record Price Cuts Demand

- Sugar Seen Falling on Speculation Prices Have Climbed Too High

- Wheat Price Seen Having Potential to Jump on Exporter Stockpiles

- Marubeni Agrees to Buy Gavilon for Access to U.S. Grain Trade

- Rashnikov Paring MMK Debt Aided by Mystery Suit: Russia Credit

- Coal Use Set for 1984 Low Batters Global Prices: Energy Markets

- Seaway Oil Torrent Boosts Gas Cargoes as Scorpio Rises: Freight

- Copper Gains on China Stimulus Speculation

- Chinese Sugar Smuggling Seen Declining by Two-Thirds in Q2

- Gold Losing Allure for Biggest Buyers Spurs Bonds: India Credit

- Palm Oil Advances to Two-Week High on Ramadan Demand Outlook

CURRENCIES

US DOLLAR – after 4 consecutive up weeks, our Strong Dollar theme is getting some headline respect (Most Read on Bloomberg this morn = “Dollar Scarce”). In conjunction with the consensus headline, the USD weakens and commodities strengthen this morning; Gold looks like it could re-test $1601 if the USD down move has any follow through.

EUROPEAN MARKETS

SPAIN – Spanish Retail Sales get smoked (-11.3% y/y in April) and their stock market crash continues (down another -1.5% this morn, down -29% since March). Rajoy wants a Bankia bailout – he’ll probably get that, but lose the trust/flows of his stock/bond market in the meantime. That’s the other side of the trade. 10yr Spanish yields hitting new highs at 6.52% (higher than Nov 2011).

ASIAN MARKETS

CHINA – not an outright bailout plan from the Chinese overnight; they’ll go with stimulus plans first – that had the Shanghai Comp +1.3% (HK +1.4%) but we’d need to see follow through from these levels for the risk management setup to change from the bearish setup Asian Equity markets have been in since March.

MIDDLE EAST

The Hedgeye Macro Team