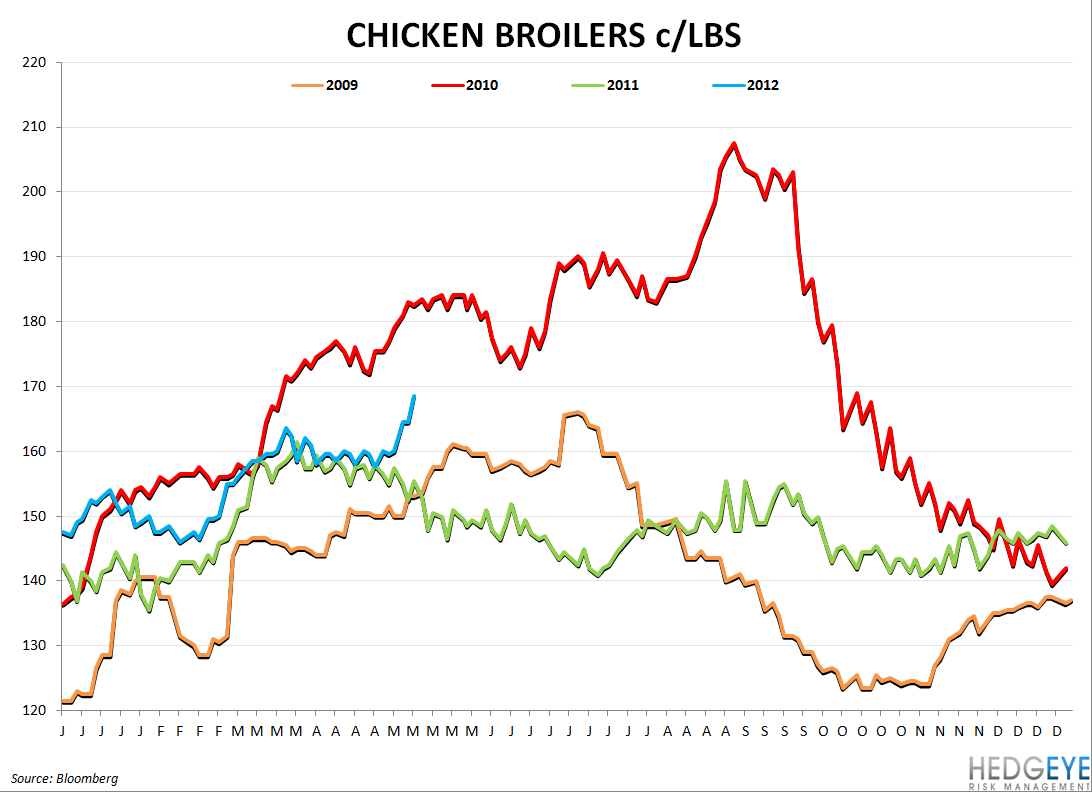

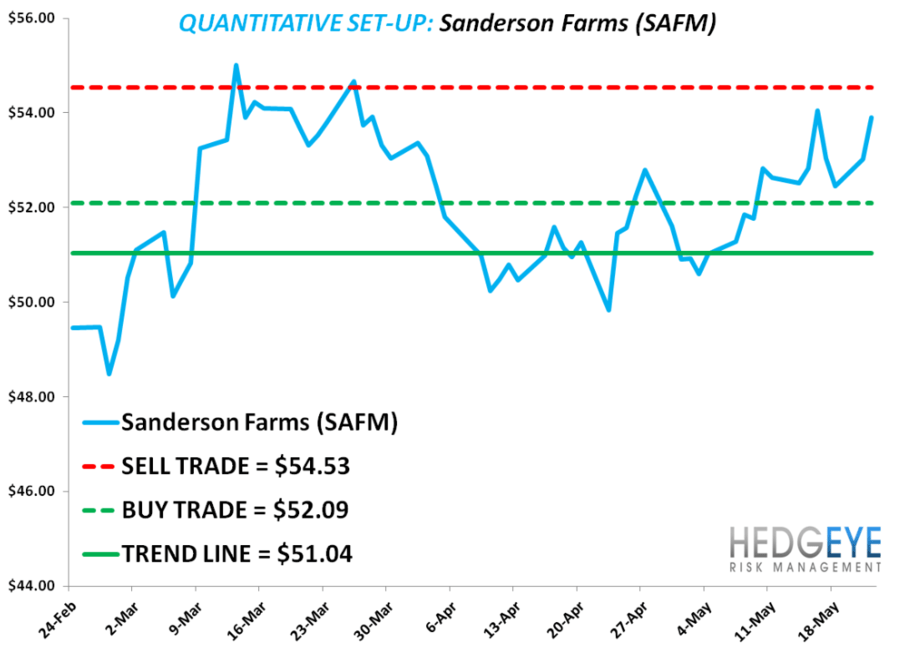

We contintue to like SAFM on the the LONG side of the "chicken trade" and BWLD SHORT!

SAFM: While the tone from management has been cautious, we see declining corn prices and tight chicken supply over the next 18 months as strong positives for the stock. SAFM’s superior balance sheet, versus its peers, helps its position as the industry turns. Intermediate term risk is seasonality in the stock Jul-Sep.