Our conviction remains high on this one. Keith taking advantage of today's low-volume pop to add to our short position.

We've included additional detail on our short thesis below as outlined in our 5/9 report "CRI: Short It."

5/9/2012 11:29 pm

CRI: Short it

Nearly all the factors that kept this stock grinding higher while estimates came down last year are either slowing, or flat-out reversing, on the margin. We really like the 3/1 odds on the short side.

We think Carter’s is shaping up as a short again. After nearly a year of perceived positive factors at its back, we think that opacity related to organic earnings power will be gone, and competitive challenges will emerge at a time when it is shifting away from harvesting its prior investments, and will need to put capital in to its model that will put a ceiling on margin improvement at a minimum, and likely create meaningful downside if our industry call for increased competition and margin pressure comes to fruition. With that, sales deceleration is a near certainty barring another acquisition, and valuation is sitting near the seven-year peak.

We say ‘shaping up as a short again’ with full awareness that it did not do what we thought it should have done in 2011. In fact, we went into 2011 with estimates for the year at $1.75 and the consensus at $2.40. By year’s end, the Street came down, and down and down by 21%, and CRI earned an adjusted $1.94 (before $0.15 Bonnie Togs accretion). Yet the stock literally defied gravity and went the exact opposite direction – gaining 35% for the year (vs. virtually flat performance for S&P, RTH and the MVRX).

If there’s one rule of retail investing that we’ve learned over time, it’s that earnings revision is the key factor in determining the direction of a stock. Pull up thefunction on your bloomberg. With 9 stocks out of 10, you’re going to see that the stock price tracks (or leads) earnings in a very tight band. Take a look at NKE, AAPL, GIL earnings revisions vs. the stock (all courtesy of Bloomberg).

NKE...Check

<chart2>

AAPL...Check

GIL...Check

Now look at CRI. HUH?

Whenever we talked to people about this name, we were given the same bull factors ad nauseam:

1) The company had the toughest COGS comps in 2H11, in advance of which it took up prices by 10%. In doing the math, a 10% increase on a $10 product at retail almost entirely outweighs a 25% increase in a $3-4 product cost.

2) At the same time, CRI was boosting its off-price sales from 1% of total in 2010 to 4% in 2011, and while this would ordinarily be dilutive to margins, it was enough to help leverage SG&A.

3) While both of these two factors played out, CRI benefitted from the addition of the Bonnie Togs acquisition, which boosted sales by an average of 6% per quarter – again, a factor that (with some minor cuts to acquired SG&A) helped leverage SG&A at the greatest rate in nearly a decade.

4) And how could we forget the ultimate response? “The market is flat, I’m clawing to hang on to my return/loss for the year, and you expect me to short the stock of a company that Berkshire Partners is not-so-slowly taking private?

Now what have we got?

1) The good news is that CRI starts to anniversary its higher product costs (that’s the bull case), but unfortunately, it starts to anniversary its pricing initiatives as well. It’s all too often that people adjust one without the other. There are, after all, two components to gross margin. Costs are forecastable. But prices to consumers – especially for a company where 40% of sales come from vertically-owned-retail – are DEFINITELY not.

2) Off price sales should come down from 4% of sales last year, to about 2% this year. Yes, that’s good for gross margin. But on top of other factors impacting top line, it will make any form of SG&A leverage very difficult.

3) Bonnie Togs is still there. But it is officially anniversaried. Now it and Carter’s each need to grow on their own without the benefit of basic acquisition accounting helping the situation.

4) Expectations are lofty – at or above company guidance for sales and EPS.

- Revenue: Consensus at $2,370mm – ABOVE guidance of $2,300mm – $2,342mm.

- EPS: 2012 Consensus at $2.61 – ABOVE guidance of $2.51-$2.61

- Consensus EPS of $3.28 for 2013, and $3.63 for 2014. We’re at $2.70 and $3.00, respectively.

- With all these other factors no longer in CRI’s favor, we have a tough time stomaching the premise that thechart on bloomberg maintains its scant correlation under these circumstances with a 20% earnings reduction.

- If our estimates prove right, there’s no reason this stock can’t see the low-mid $30s. But under the most bullish consensus expectations, we still have a tough time getting this name in the upper $50s. We like the 3/1 odds of a short here.

5) And lastly…the “Berkshire is Buying” argument is pretty much dead in the water. Yes, they’re selling on the margin.

Historical context is important here...

We were asked a couple of weeks ago by a top client as to why CRI traded at such a high EV/Sales ratio (2.1x) circa 2005. Our answer sounded something like this:

This was when CRI achieved cult stock status. There were several factors, all related to post IPO action.

The pitch on the IPO was…

a) Shift away from basics into playwear

b) Shift from traditional dept store biz to serving 1) mass channels, and 2) company-owned retail.

c) CRI had new arrangements with Li&Fung – through which it cut its sourcing costs by nearly 1/3 and passed right through to consumers in the form of lower prices to gain share.

d) Remember that this period (ending April 2007 when LIZ went Ka-Boom) was easy for apparel retail. You could be an average brand and run at peak margins without much effort. The environment allowed CRI to sell into three completely distinct channels with like product without stepping on each other’s toes – and the Street was not only oblivious, but it also gave CRI’s multiple credit for this as a big positive.

e) Then in 2005 CRI bought Osh Kosh. In the ensuing 2-years, they cut employee count from 400 to less than 100. Margins went up temporarily, before growth slowed and the story became outwardly and visibly broken.

f) Pretty soon thereafter, people realized that this name was not infallible – that it can’t sell the same stuff through Target, Kohl’s, Macy’s and its own stores -- and that it can’t cut costs to keep margins high in the face of slowing growth.

g) Fred Rowan (CEO) got fired in 2008, and since then, the Mike Casey era has taken hold. Definitely a better regime. But there was just as much financial engineering as anything else (he was former CFO). CRI had to button up policies due to a markdown irregularity accounting issue w KSS, as well as an exec being charged with fraud and insider trading by SEC in 2010. Nonetheless, it’s got a long way to go before it’s worthy of ‘cult stock’ status again. Our point is that today it is sitting at 1.25x EV/Sales. That’s well below the prior peak of 2.1x, but the old peak is just that…the OLD peak. It need not apply any more.

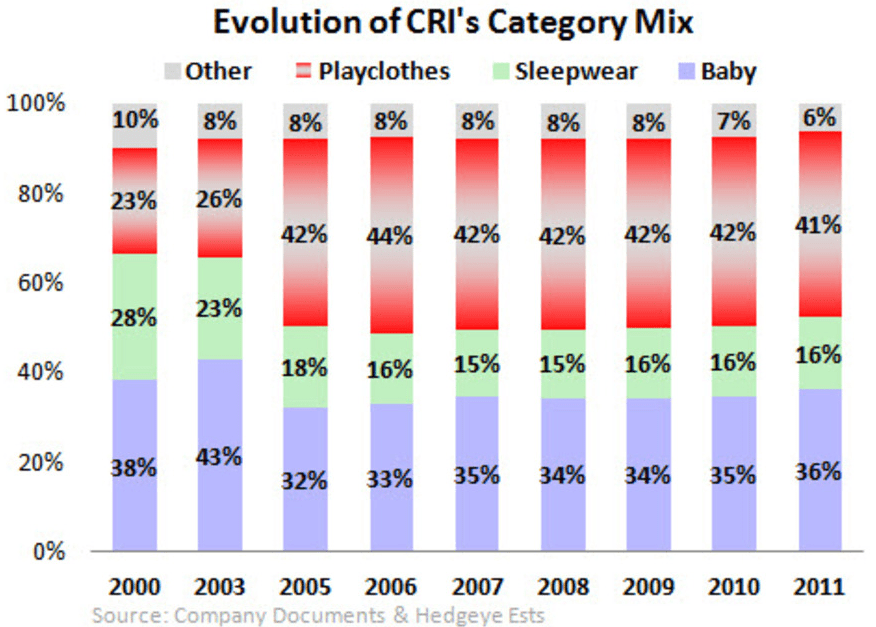

Playwear has nearly doubled as a percent of CRI’s total over the past ten years. ‘Baby’ is a very defendable business – the Carter’s brand goes a long way with a new Mom swaddling her newborn. But in the Playwear category, it competes with everything from Children’s place, to Old Navy, to JC Penney and Wal-Mart private label. Not a place to hang your hat on.