Recent housing data bodes well for BYD’s local LV business.

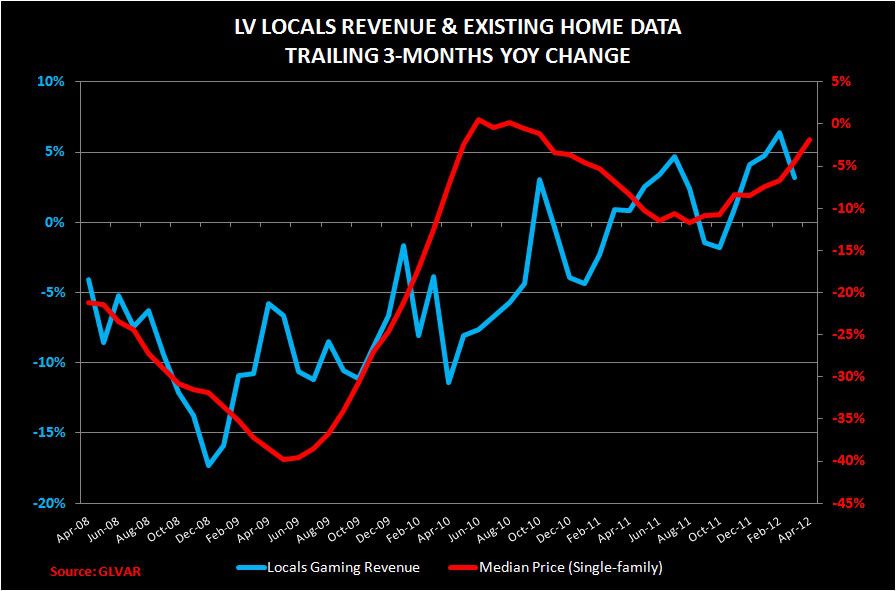

April housing data continued a positive recent trend in Las Vegas. We’ve shown in the past that housing prices were the number one driver of gaming revenues over the last 15 years both in the US and the locals Las Vegas market. Clearly, BYD would benefit immensely from home price inflation.

The median price of a single-family home sold in April gained 2% over the last year bringing the 3 month moving average to almost flat. Single-family home sales increased 3%, while new home sales jumped 35% in April. While those figures are important in terms of price stability reliability, actual pricing is the key variable. Case-Schiller pricing data is probably more reliable but we only have data through February 2012. Up to that point, the data showed similar trends to the Greater Las Vegas Association of REALTORS (GLVAR) data as seen below.

BYD’s net gaming revenues have been trending flattish in recent quarters, yet EBITDA has been substantially higher due to a smaller cost structure. If housing prices and thus gaming revenues continue the trend, the flow through should be high and BYD should continue beating estimates for the foreseeable future.