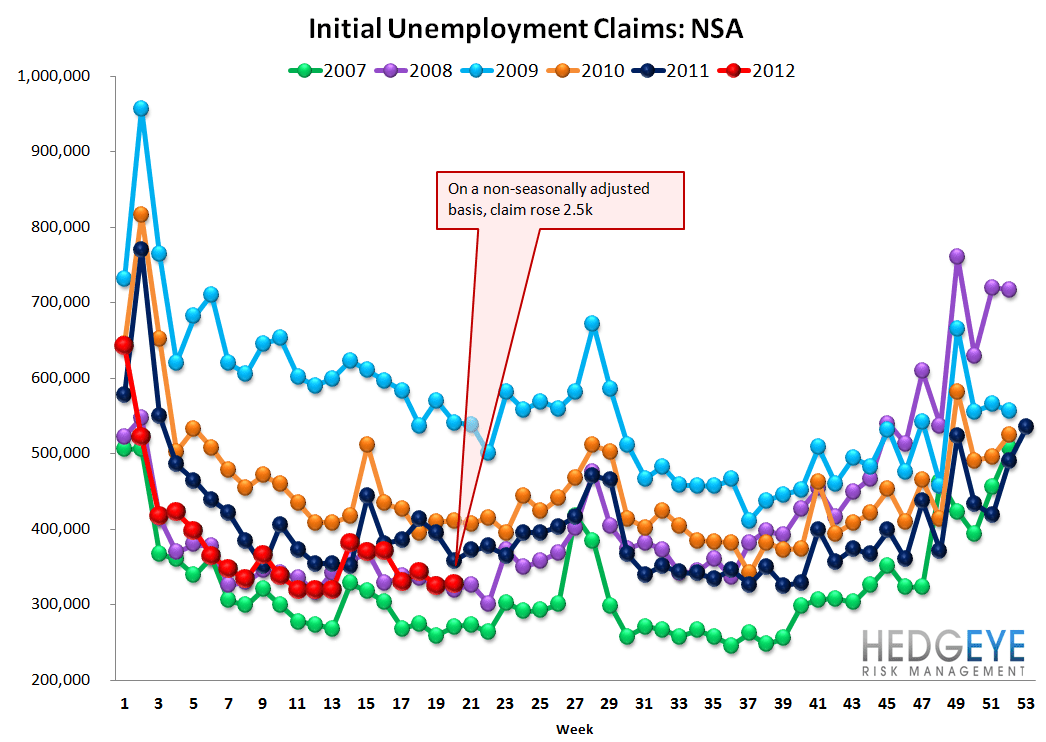

Initial Claims

Initial claims came in at 370k for the second week in a row. Incorporating the 2k upward revision to last week's print, claims fell by 2k. Rolling claims also declined, falling 5.5k to 370k. On a non-seasonally adjusted basis, claims rose 2.5k to 328k. Over the last few weeks, claims have been treading water, making only slight movements up or down. We expect to see claims rise in the summer months based on faulty seasonal adjustment factors.

2-10 Spread

The 2-10 spread tightened 3 bps versus last week to 145 bps as of yesterday. The ten-year bond yield decreased 3 bps to 174 bps.

Financial Subsector Performance

The table below shows the stock performance of each Financial subsector over four durations.

Joshua Steiner, CFA

Allison Kaptur

Robert Belsky

Having trouble viewing the charts in this email? Please click the link at the bottom of the note to view in your browser.