The Macau Metro Monitor, May 23, 2012

BASIS POINT-WYNN MACAU LAUNCHES $1.5 BLN SYNDICATED LOAN Reuters

Wynn Macau Ltd launched a US$1.5 billion two-tranche syndicated financing for a new project on Macau's Cotai Strip. According to sources, the deal consists of a US$1 billion five-year revolving credit and a US$500 million six-year term loan. Deutsche Bank AG and JP Morgan had joined with US$200 million each prior to syndication. Sources said Wynn Macau will be issuing a bond and the two banks could be involved.

Sources said the margin on both tranches opens at 250bp over LIBOR for the first two quarters after which they will be based on a leverage ratio grid. The margin will be 250bp for 4.5 times or more, 225bp for 4-4.5 times, 200bp for 3-4 times, or 175bp for less than 3 times. Banks are invited to join at a top-level upfront fee of 200bp for commitments of US$200 million and the global coordinating lead arranger title; a 150bp fee for US$150 million and the lead arranger title; a 100bp fee for US$100 million and the arranger title; and a 75bp fee for US$50 million and the lead manager title.

Banks that join before June 8 or 9 will get an additional 12.5bp early bird fee. The revolver comes with a 75bp commitment fee. The term loan tranche repays in 16 unequal instalments after a two-year grace period. Banks can choose to join in US$ or HK$. Responses are due end of June.

CHINA BIG FOUR BANKS ISSUE CNY 34 BILLION NEW YUAN LOANS IN MAY Dow Jones, Reuters

China's biggest four banks issued only CNY34BN ($5.4BN) in new yuan loans in the first three weeks of May, and their deposits declined by CNY270BN over the same period, the 21st Century Business Herald reported on Tuesday, citing unidentified banking sources.

The four banks--Industrial & Commercial Bank of China Ltd, China Construction Bank Corp, Bank of China Ltd., and Agricultural Bank of China Ltd.--were previously reported by local media to have barely issued any new yuan loans in the first two weeks of May. These banks usually account for 30% of new yuan loans issued by China's whole banking system.

New loans issued by Chinese financial institutions fell to CNY681BN in April, down from CNY1.010 trillion in March and posting the lowest monthly level so far this year. China loans in May 2011 reached CNY 551.6BN.

RUSSIA EYES VLADIVOSTOK CASINO ZONE TO WOO ASIAN MONEY Reuters

Russia's state-owned Nash Dom Primorye said it is seeking private investors and/or companies to build casino resorts in a six square kilometre area near Vladivostok. The masterplan includes luxury hotels, a yacht club, shopping malls as well as outdoor sports such as golf. As it stands now, the zone is 2.6 square kilometers, but can be extended to six square kilometers. Known as the Integrated Entertainment Zone, the project has space for roughly five large resorts.

Marina Lomakina, general director of Nash Dom, said she hoped the zone would be fully completed within five years. "We want companies who are well known and will help create amenities that are more than just casino gaming," she said, adding that the zone would require a total minimum investment of $2BN from private investors looking to develop properties.

Vladivostok is one of four official Russian government zones where casino gambling is legal but is the only one that has formally initiated plans to lure foreign investors.

Nash Dom Primorye has appointed Las Vegas-based Galaviz & Co as lead strategic adviser for the tender. The tender will be initiated in June, giving potential international operators 60 days to send in a pitch and budget estimates. The Russian government will then enter into discussions with potential investors by the end of October.

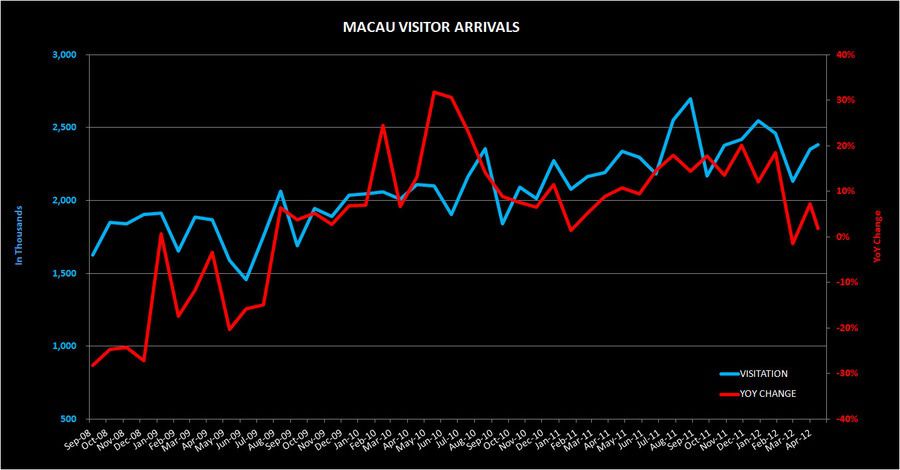

APRIL 2012 MACAU VISITOR ARRIVALS DSEC

Visitor arrivals totaled 2,382,156 in April 2012, up 1.9% YoY. The average length of stay of visitors increased by 0.1 day YoY to 1.1 days. Visitors from Mainland China increased by 9.5% YoY to 1,391,119, with those traveling under the Individual Visit Scheme rising by 9.3% to 541,551.

SINGAPORE'S INFLATION RISES TO 5.4% IN APRIL Channel News Asia

Singapore's inflation rate accelerated in April to 5.4% YoY, from March's 5.2% rise.