This note was originally published at 8am on May 08, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Some are ugly and some are beautiful.”

-Ray Dalio

That’s what Bridgewater’s Ray Dalio wrote recently about Deleveragings. Spell (and box) checkers take note: the plural of deleveraging doesn’t yet register on Wikipedia as a word. By the time this Sovereign Debt Cycle is over with, it will.

I was flying back to New York from Toronto last night and Dalio bubbled up to the top of my Research Pile alongside another one of the most credible Global Macro Risk Management sources to emerge from 2007’s top, Eclectica’s Hugh Hendry.

Not surprisingly, both Dalio and Hendry are talking about the same risk to asset prices (stocks, bonds, commodities, etc. ) that have been supported by Policies To Inflate – deflation. But both have different views on the pace and timing of what asset price inflations and deflations could look like.

Back to the Global Macro Grind…

If your risk management process doesn’t embrace the uncertainties associated with a Globally Interconnected Marketplace of colliding factors, it’s more difficult to apply the principles of Chaos (or Complexity) Theory to what it is that you do every day.

People get whipped around by questioning what is “causality versus correlation” all of the time. Our process embraces the idea that both can occur at the same time.

In Chaos Theory you have Emergent Properties and Phase Transitions. The Correlation Risk born out of an emergent property like the World’s Reserve Currency (USD) and asset prices is very real. So are the phase transitions (crashes) born out of that Correlation Risk.

The US Dollar Index is up for the 5thconsecutive day to $79.58 this morning. Look at the immediate-term TRADE correlations that our model is spitting up versus the USD:

- WTIC Oil = -0.72

- Brent Oil = -0.64

- Gold = -0.77

- Copper = -0.76

- Wheat = -0.71

- Soybeans = -0.81

In other words, that’s how I can show you, in real-time, the answer to both Dalio and Hendry’s question on timing asset price inflations and deflations. US Dollar driven Correlation Risk doesn’t matter all of the time. Neither is it perpetual. But some of the time, it matters big time. And that’s when you get paid to be long or short beta.

If you believe (like I do), in the causal relationship between Monetary Policy and Currency moves, you’ll absolutely love learning about this. It forces us to Re-Think and Re-Learn, every day. If you believe, like a dogmatic Keynesian (Bernanke) does, that monetary policy doesn’t infect currency prices which then, in turn, affect inflations/deflations, this will drive you right batty.

Chaos Theory is not part of the current Western Academic Curriculum in Economics. By the time I am dead, it will be. It’s math. And the math will ultimately trump the social science of studying the 1930’s depression in a vacuum.

Don’t take my word for it on this. Read economic history. Overlay Reinhart & Rogoff teachings about the relationships between deficits, debts, and inflation/deflation with what modern day practitioners are writing about. It’s all out there. Educate yourself.

Dalio’s February 2012 research note is titled “An In-Depth Look at Deleveragings” and in it he does exactly what Professor Robert Shiller taught me to do here at Yale – study the long-term cycles, across countries, so that you can begin to understand the scenarios, probabilities, and mean reversion risks.

Dalio considers both the “Ugly” (1920’s Germany) and the “Beautiful” Deleveragings. The most relevant scenarios I thought he nailed down to the risk management board were:

- UK Deleveraging 1947-1969

- Japan Deleveraging 1990-Present

- US Delevergaing 2008-Present

Not one of these deleveragings were the same in terms of numbers of years and/or asset price % moves, but the monetary policies that were engaged in by central planners during all 3 certainly rhyme.

Dalio calls the UK and US Deleveragings of 1947-1969 and 2008-Present “beautiful.” I’ll call what happened in the UK thereafter (1970s) and what is about to happen in the US (if we abuse the US Dollar through debt monetization further), his version of “ugly.”

Hendry said he was long asset price inflation (Equities and Agricultural Commodities) in February. That’s was a good call until the end of February and early March when Global Equity and Commodity price inflations stopped.

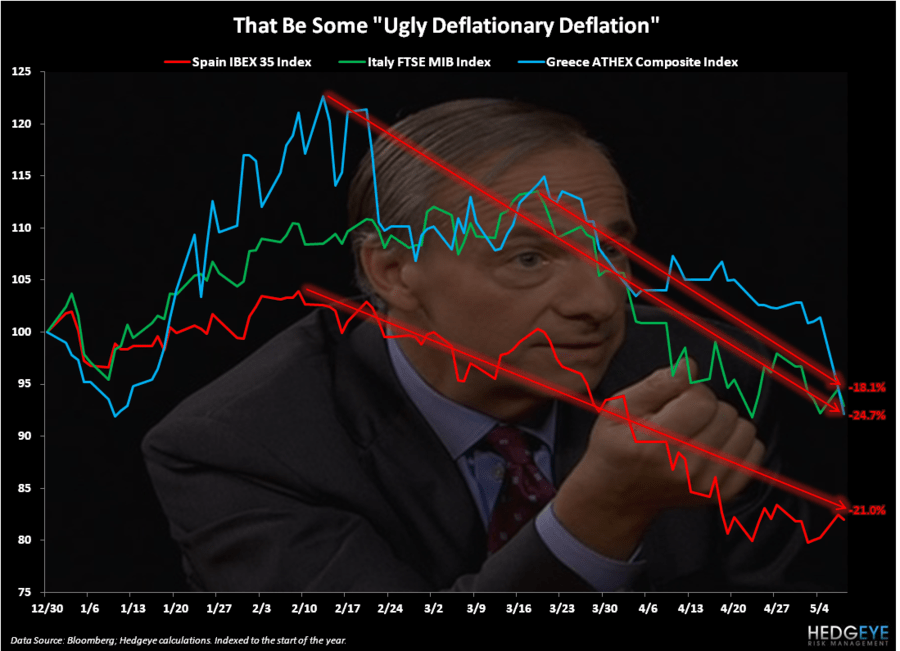

Now what you see is what we call Deflating The Inflation. It’s not what Hendry calls “hyper-deflation”, yet. Neither is it the “ugly deflationary deflation” that Dalio warns of. Unless you are long of anything Spanish, Italian, or Greek Equities, that is…

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, EUR/USD, and the SP500 are now $1627-1651, $112.42-113.87, $79.36-79.68, $1.30-1.32, and 1364-1388, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer