Conclusion: There’s still wood to chop here, no doubt. But this is a sub $3bn company acting like a $10bn company. If we’re right, than URBN is trading at about 7.1x our next year EBITDA estimate. If you want to short that, knock yourself out.

We think URBN is headed higher. We like this one across all three of our durations, TRADE, TREND, and TAIL. The tone and cadence of management’s approach this quarter makes this a tough story to build a negative case against – particularly in a space where we think we need companies with asymmetric factors on the long side in order to take them higher.

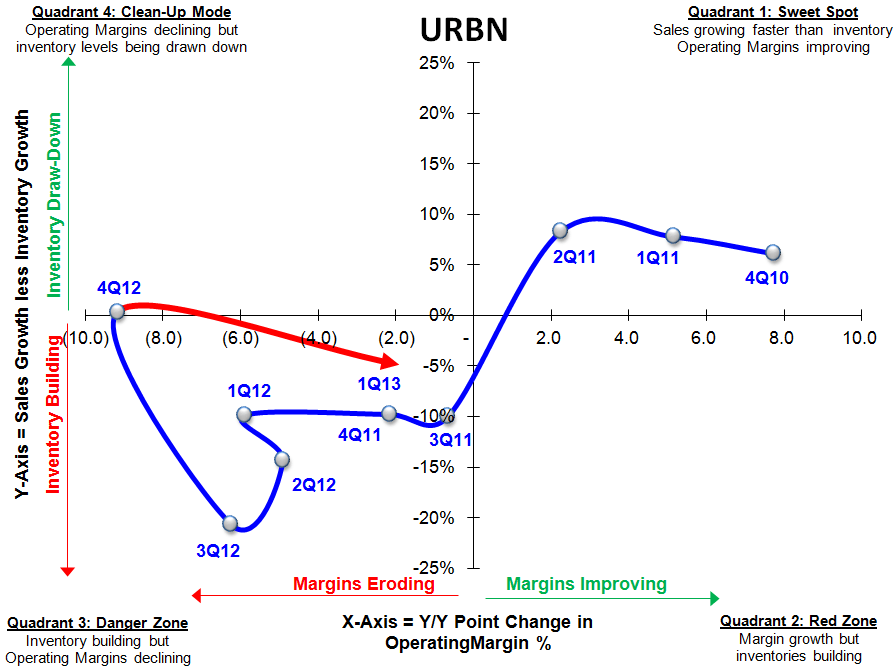

We went into the quarter thinking that URBN was one of the few names that had the luxury of a disproportionately favorable miss/beat balance (the market rewards a penny beat more than it penalizes a penny miss). Over the past six months URBN has had one of the most major management changes we’ve seen in a retailer relative to its size in a very long time. Our rather strong sense is that this team will be given a free pass to shake things up near-term, and that any upside (even if by accident) will be a bonus.

Let’s not bend any facts here. The quarter stunk. URBN took 8.6% sales growth and morphed it into a 10.1% EBIT decline. But relative to expectations, it was slightly better. One comped a comp (Urban), while the other (Anthro) comped down on the easiest compare of the year. There were definitely puts and takes. But the big take-away came from simply listening to this management team.

They sounded so extraordinarily focused – such a stark contrast to the URBN of six months ago. Seriously…go back and listen to the past two calls. Night and day. That’s what you get when you bring in the founders to save the day.

The message is simple.

- Hire all the right talent.

- Empower each of them to come up with a concise plan, to which they will be held accountable.

- Give them the financial and human resources to achieve the plan.

Along the way, they’ve got shared services initiatives (DC just going up for 3Q) that should allow URBN to leverage the back-end across concepts while investing in areas like mobile and digital to more efficiently flow product and reach new customers.

They don’t really give comp forecasts – which is great bc forecasting comps is ridiculous. They simply focus on the process to put up the numbers, and hold themselves accountable to execute. Anyone reading this knows that I (McGough) rarely throw out public kudos to management teams, but the bottom line is that listening to these guys is like listening to a company with $10bn in revenue, not $2.5bn.

There’s still wood to chop here, no doubt. But we’re coming up with estimates about 20% above consensus. If we’re right, then URBN is trading at about 7.1x our next year EBITDA estimate. If you want to short that, knock yourself out.

Brian McGough

Managing Director

Highlights from the Call

Revenues +9%

- $34mm increase in net new stores sales (14 new stores)

- 2% increase in Retail comps (incl. DTC)

- Urban: +6% vs. +2.3E

- Positive comps across all categories

- Free People: +2% vs. +6.1E

- Opened largest store to date with full floor of intimate apparel ("Intimately Free")

- Anthropologie: -2% vs. +0.3E

- Positive regular price comps in women's apparel

- Catalog showed significant aesthetic improvement throughout the Q

- Retail Store Segment Sales +7.5%

- Comparable Store net sales (-1%)

- Transactions (-1%)

- Avg Units per Transaction (-2%)

- Partially offset by AUR +2%

- Terrain: Excellent Spring season from weather; opened 2nd store in Westport, CT

- DTC net sales +15%

- All brands posted healthy DTC growth

- Wholesale +2%

-

- 19% increase in Free people wholesale; 30% increase in sales to specialty accounts

- Offset by transition of Leifsdottir to Anthropologie Brand

International:

- All of the UK stores were challenged

- Urban stores in Germany tracking above sales plan

- Urban/Anthro DTC Europe sales gains in excess of 30%

GM: (-131 bps)

- Store occupancy deleverage related to increased store openings

- Increase in new and non comparable European stores

- Slightly higher markdowns on some women's categories across all brands

SG&A +11% (+62bps as % of sales)

- Primarily due to deleveraging of direct controllable expenses due to negative comps

Inventories +13%

- Increase in comparable retail inventories + 11% at cost, +5% in units

- Total comp store inventories +8% at cost

- Remaining due to acquisition of new store inventory and wholesale inventory

Dick Hayne CEO Goals:

- Fill management roles with top talent- met quickly with a solid team of merchants leading the brands

- Strategy to reignite top line growth - Emphasizing growth through 4 initiatives

- Increase productivity in current channels through marketing, improved product and tech

- Acquire more customers by expanding distribution channels- more robust presence in Europe and Asia

- Expanding product offerings (i.e web exclusives, Free People intimates)

- Acquire new concepts to compliment current brands- nothing currently in the pipeline but reviewing opportunities

- Ensure Brand leaders have tools, talent, capital to succeed

Shared Services Initiatives:

Technology

- Special focus on supporting e-commerce and international growth initiatives

- Rolled out mobile POS to store last year- continue to expand number of devices

- Capabilities will be expanded to fulfill store or online out of stock from any store in the US

- Launching IPAD POS device later this year

Fulfillment

- Expect West coast fulfillment center to be open in 3Q13

- Will substantially reduce delivery times to west coast customers

- Will help reach service goal of US of 2 days or less

Talent

- Focused on customer facing talent

- Improving the scope of digital recruiting

- Enhancing merchant development program

Outlook for the Remainder of the Year:

2Q

- Weather may have been a pull forward of sales into Q1

- Planning 14 stores in Q2

- Gross Margin Rate (absolute rate of 35.6%) will be similar to Q1

Full Year

- Sales exceeded conservative plans but benefitted from favorable weather in March- full year plans unchanged

- 55-60 stores

- 21 URBN

- 16 Free People

- 21 Urban Outfitters

- 16 Anthropologie

- 1 Terrain

- 1 BHLDN

- Planning 2H margin improvement based on product content and lower mark down rates

- Planning mid teens increase in SG&A for the remainder in the year due to DTC investments, ramp in marketing and further investments in people

- Capex: $190-$200mm driven by new stores, fulfillment center and home office expansion

- 2013 Effective tax rate 36.5%

Q&A:

Inventory Fullfillment:

- Will satisfy customer demand & Reduce out of stock

- Will focus on fulfilling from locations where demand is weakest

- Some exclusive items are being returned to stores, with new system, items can be shipped back without mark down potential

Anthropologie

- Substantial improvement in aesthetic & product content in Catalog- better customer focused product

- Seeing progress in merchandising assortment

- Will be awhile before reaching rhythm of Anthropologie from years ago

- Expecting to take some markdowns but seeing strong fundamental signs

- Anthropoloie working on complete overhaul of website- it has gotten stale just like calendar was stale before recent refresh

- Working on rightsizing the Home size based on market

- Still working towards desirable pricing/product mix

- UK requiring localization- Will develop and source product specific to certain markets (both brand and designers); brand remains scalable

Urban Outfitters:

- Website- approach to visual can be improved

- Plan to do some additional cross referencing across channels (recently referenced in store sales online which yielded a productive week)

Free People:

- Have added new components to intimates site

- Expanding other categories beyond Free People Intimates

- Continue to work on social media aspect of site and blog- getting new reader with updated blog and look books

Loyalty programs

- Urban and free people in process of launching loyalty program

- Anthropologie in the process of reinvigorating loyalty brand

- See nice lift in traffic as a result

Inventories

- Category mix shift driving 11% cost increase in inventories as opposed to cost inflation

- Inventories were relatively clean at the end of Q4

- All buyers make mistakes- in the process of clearing some excess through markdowns

- 90 day ownership better than the prior year

- Expect to make incremental progress as the year develops on markdowns

- Change in mix driving shift in AUR with weather increasing amount of inventory

- Expecting to return to desired inventory levels but will remain slightly elevated due to mix change

Top Line Guidance

- Remain optimistic and believe inventory is well positioned

- Expecting to take fewer mark downs as the year progresses

- There MAY have been a pull forward in sales but not guaranteed

Fashion Shift

- Seeing Fashion shift towards bottoms

- Traditionally impacts women who want to go out and invest in new wardrobe items

- Duration of trend is unpredictable but typically last for some time

- Merchants are in touch with demand and are planning inventories accordingly

- Shift implies tops are less desirable, though some remain strong

- Will be additional mark downs in some top categories that aren't selling as well as last year

New Store Productivity:

- New stores opened in Q1 are performing at or above plan

Europe

- Great deal of strength in European DTC in Q1 at Urban Outfitters

- Businesses on the continent performed stronger than the UK in stores (issues with cold wet weather)

- Saw an over penetration in outerwear with seasonal product sales soft from cold weather

- Women's apparel most challenged business in the UK though it has been performing well in DTC and Continent

- All 3 brands have significant opportunity to expand presence in Europe and Asia

- Free People will be launching wholesale into the UK over the next

- Launching Free People DTC into Asia over the next 18 months

- Urban will also be launching presence in Asia over the next 18 months

- Ran a Spring season sale focused in the UK to keep inventory levels in check

- Anthropologie requiring localized assortment similar to Urban Outfitters

Gross Margin Guidance:

- Implies sequential deterioration in YoY margin rate change

- Planning occupancy deleverage in 2Q

- Opening 8 new stores above new stores opened in 2H12 as well as non comparable European stores

- There are markdowns anticipated in certain women's categories

- Planning for 200-250bps of improvement in annual GM rate

North America:

- East Coast followed by Midwest and South saw greatest growth in the US

- Some European stores suffered from cold/rainy weather- seeing direct correlation with weather

- Major Malls performing the best

DTC Mix Shift:

- Investing in the DTC business

- Have only been in DTC business for 10-12 years- already captured 20% of sales

- Expect the business to continue to grow at current rates if not accelerate

- Expect DTC penetration to reach 40% relatively quickly and anticipate rate going up