-- Below is a condensed version of our thinking on why Greece is shooting itself in the face if it decides to leave the Eurozone and why Eurocrats are motivated to keep it in the Union. For more specifics, please contact me at to set up a call.

No Current European Positions in the Hedgeye Virtual Portfolio

Asset Class Performance:

- Equities: The STOXX Europe 600 closed down -5.2% week-over-week vs -0.4% last week. Bottom performers: Cyprus -10.7%; Greece -10.1%; Ukraine -8.4%; Russia (RTSI) -8.3%; Portugal -8.1%; Finland -7.5%; Romania -7.4%; Austria -7.2%; Italy -7.1%. Top performers: Slovakia -0.5%; Denmark -2.0%; Switzerland -2.2%.

- FX: The EUR/USD is down -1.18% week-over-week vs -1.15% last week. W/W Divergences: HUF/EUR -3.09%, RUB/EUR -2.56%, PLN/EUR -2.10%, TRY/EUR -1.61%; SEK/EUR -1.52%, CHF/EUR +0.02%, DKK/EUR +0.02%, ISK/EUR +0.36%.

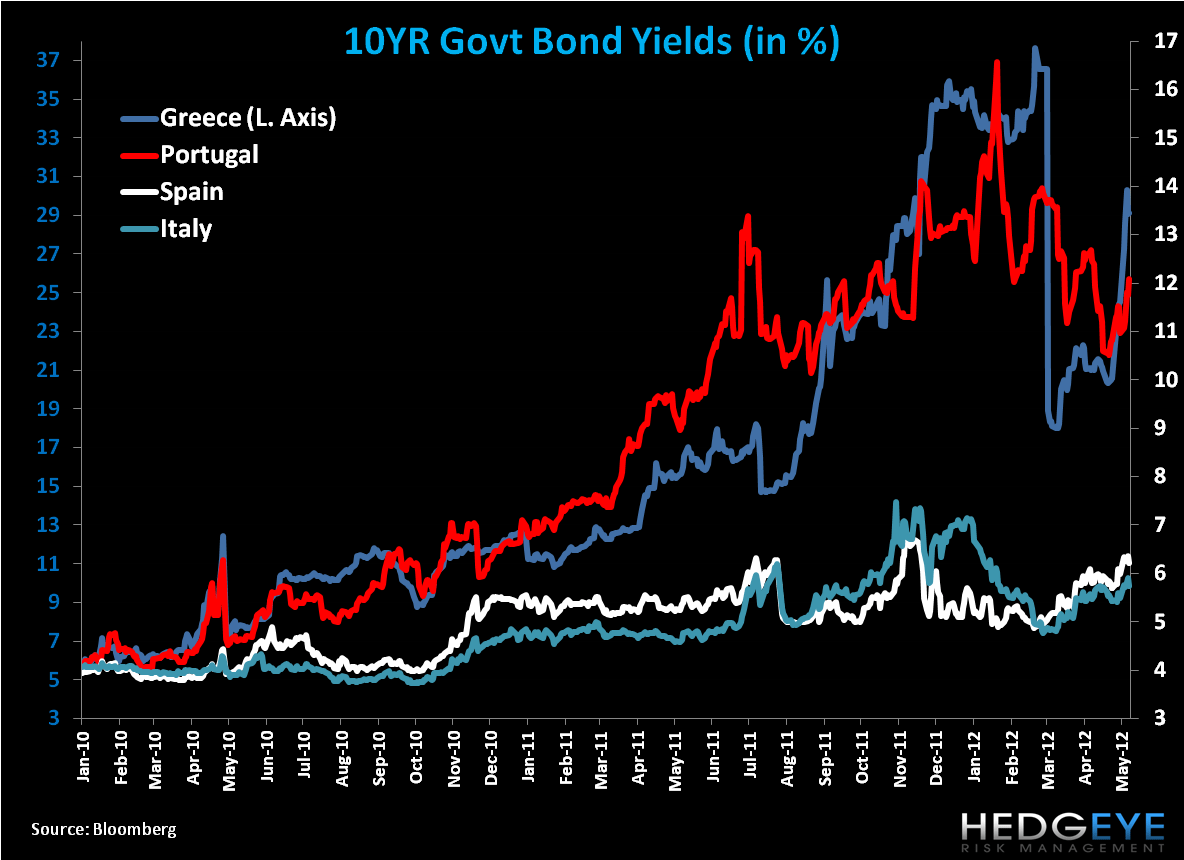

- Fixed Income: Greece’s 10YR government bond yield saw the biggest gain, at +461bps week-over-week to 29.14% after a gain of +396bps last week. Portugal followed at +112bps to 12.08%, then Italy +25bps to 5.74% and Spain +24bps to 6.22%. Germany fell -9bps to 1.42%. On a month-over-month basis, the Greek 10YR yield is up a monster +802bps!, while Germany fell -31bps over the period.

On Why Greeks Shouldn’t Leave the Eurozone/EU:

Below is a condensed version of our thinking on why Greece is shooting itself in the face if it decides to leave the Eurozone and why Eurocrats are motivated to keep it in the Union. As preface to the commentary below, importantly, we DO think that a currency union governing highly uneven economies and culturally divided populations with one monetary policy is a flawed structure. Additionally, we DO NOT think that states will give up their full fiscal sovereignty to Brussels and the region will run into the same flaws witness by the Growth and Stability pact. We DO think that fiscal consolidation targets across many of the PIIGS are unrealistic, and that the stronger states, Germany in particular, will continue to subsidize the weak to keep the exiting membership structure intact, as it’s to Germany’s benefit from a currency and export market perspective.

As it relates to Greece specifically, we expect Eurocrats to rhetorically take a hard line on the real possibility of a Greek default as to encourage the future leadership of Greece (and the Greek people themselves) that bailout funds are contingent on upholding austerity. While we view it highly likely that terms on austerity could be reduced (and not just for Greece), ahead of June 17th elections in Greece, Eurocrats must signal to the Greeks that their fate is tied to their vote: for or against austerity, which will impact if it stays or leaves the Union. Germany’s Finance Minister Wolfgang Schaeuble nicely states this point:

“If Greece decides not to stay in the Eurozone, we cannot force Greece. They will decide whether to stay in the euro zone or not.”

Here’s a taste of the hard line put forward this week from key Eurocrats:

- IMF's Christine Lagarde: A Greek exit from euro would be "extremely expensive", still the IMF must be technically prepared (Dutch public tv).

- ECB President Mario Draghi: "Our strong preference is that Greece will continue to stay in the euro area," and suggested the ECB won't go to extraordinary lengths just to prop up Athens.

We are NOT of the camp that there will be an imminent exit of Greece from the Eurozone and EUR, despite recent headlines and even polls like one recently released from Bloomberg that recorded a 50% chance Greece exits the Eurozone this year. The main points that support our position are:

- The resolve of Eurocrats to keep their jobs and preserve the “idea” of the collective benefit from bound states.

- The Fear of the Unknown: snowball effect of a Greece default precipitates Portugal leaving and then the much more serious threats of a Spain or Italy, far larger economies, defaulting.

- Greeks want to stay: A poll suggests 78% of Greeks want to stay in the Eurozone and with EUR.

- Returning to the Drachma would not be a competitive advantage in the near to long term (more below).

- There are no provisions in the relevant European Treaties (Lisbon Treaty or Maastricht Treaty) for a country to exit the Euro, nor any provisions for a country to be expelled from the Euro.

However, we’re well aware that Greece teeters with one foot in the Eurozone (surviving on bailouts from Troika) and one foot out (by most measures the country has defaulted), and we can’t rule out that a catalytic force like a massive run on the banks (beyond what’s already left the country) could come in a matter of days. Such an event, short of the ECB backing Greek deposits, would spell a swift exit.

Why Greece Leaving the Eurozone/EUR is NOT to its competitive advantage:

- A return to the Drachma (or “New” Drachma) would result in an immediate and sharp depreciation versus the EUR, with a few of the main outcomes being:

- An immediate run on Greek banks = destruction of Greek banking system

- High inflation, pushing up labor costs (and therefore negating “competitiveness” argument)

- A “cheap” currency is a tax for Greece because it is a heavy importer of its energy and food

- Borrowing costs to raise debt under the Drachma would be very costly

- Does not have an export base, like an Argentina (which defaulted in 2001) to export its way to growth

From a cultural and economic perspective, it is also worth noting that Greeks have witnessed a relative prosperity in the 2000s under the EUR. Although this prosperity was propped up by fudged government books and cheap loans from European banks, nevertheless it’s worth consideration that Greeks still identify prosperity with the EUR. Therefore, the poll suggesting 78% of Greeks want to stay in the Eurozone and with the EUR, is not surprising. Further, it’s our view that Greeks view the financial health of the country tied to Troika’s handouts. If the line of funding is severed, we do not expect this to be viewed positively by the populous, a position which politicians will be forced to address in elections.

The latest poll from MARC/Alpha survey, conducted on May 15-17, showed that New Democracy would win 26.1% of the vote compared with 23.7% for Syriza (the anti-austerity party). It added that based on this result, New Democracy would win 123 seats. Combined with the 41 seats projected to be won by Pasok, Greece's two major bailout parties would have a 14-seat majority in the 300-seat parliament. You’ll note that in a previous poll conducted before talks to form a government collapsed, Syriza led with 27.7%, up seven points over New Democracy. We think the shift is representative of a populous that understands it needs to play ball with Brussels despite its resistance to austerity.

CDS Risk Monitor:

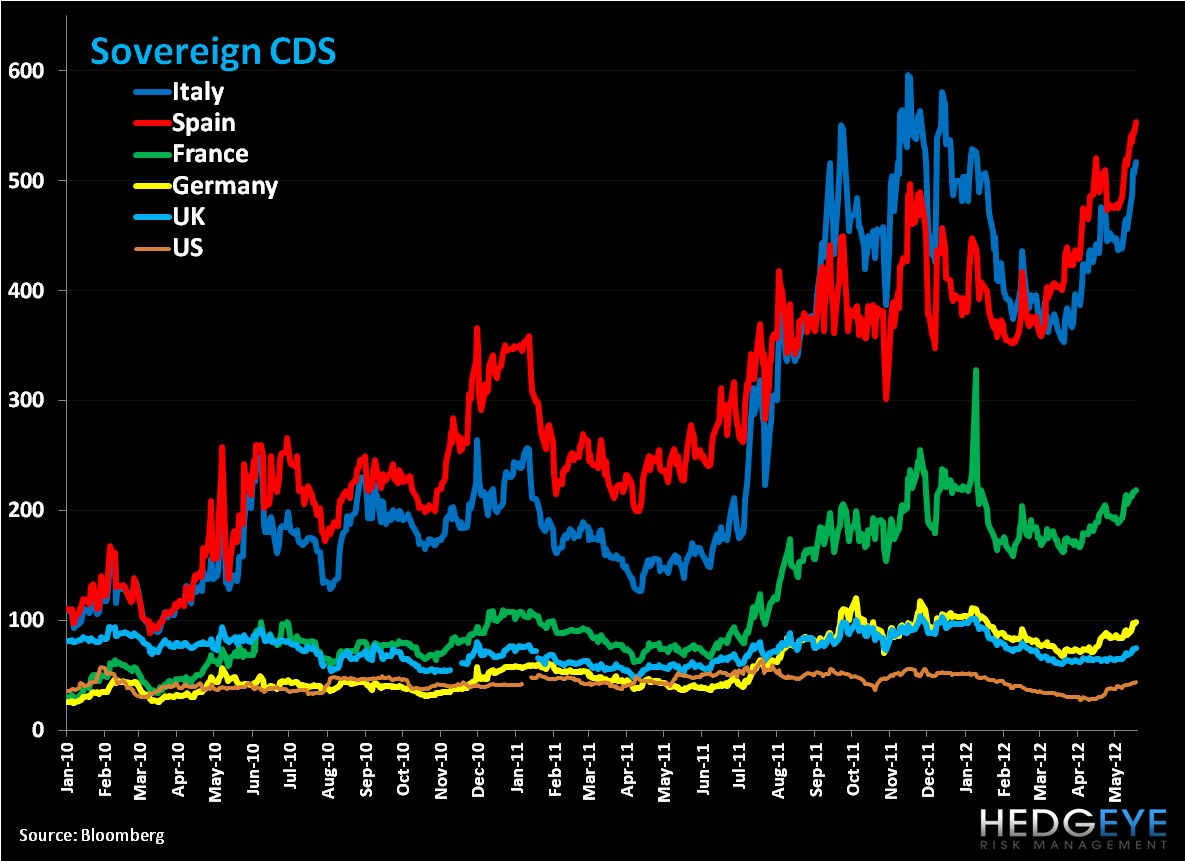

Week-over-week CDS was up across the main countries we track. Portugal saw the largest gain in CDS w/w for a second straight week, +109bps to 1184bps, followed by Ireland +90bps to 683bps, Italy +61bps to 517bps, and Spain +39bps to 553bps.

Data Dump:

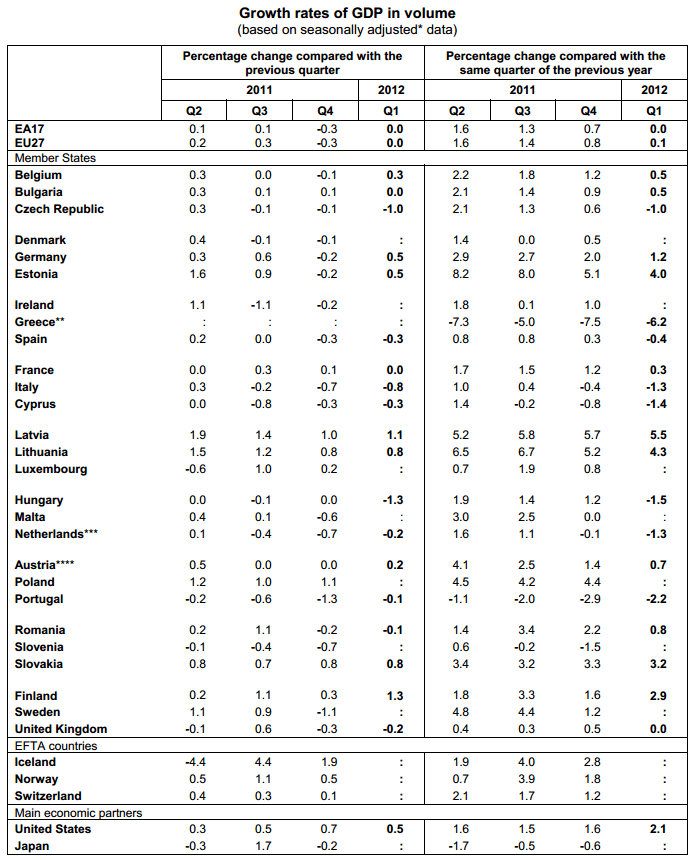

Q1 GDP:

Eurozone CPI 2.6% APR Y/Y

Eurozone Industrial Production -2.2% MAR Y/Y (exp. -1.4%) vs -1.5% FEB

-0.3% MAR M/M (exp. 0.4%) vs 0.8% FEB

Eurozone ZEW Economic Sentiment -2.4 MAY vs 13.1 APR

EU 25 New Car Registrations -6.9% APR Y/Y vs -7% MAR

- Volkswagen (VOW.GR) 261.571, (5.2%)

- PSA (UG.FP) 132,466 (0.2%)

- GM (GM) 85,493 (11.2%)

- Renault (RNO.FP) 89,724 (15.1%)

- Fiat (F.IM) 75,462 (11.3%)

- Daimler (DAI.GR) 56,677 +1.1%

- Toyota (TM) 41,259 (13.2%)

- BMW (BMW.GR) 68,334, +2.6%

- Nissan (NSANY) 29,719 (19.5%)

- Honda (HMC) 10,310 +2.5%

- Ford (F) 79,223 (8.3%)

Eurozone Trade Balance SA 4.3B EUR MAR vs 4B EUR FEB

Germany ZEW Current Situation 44.1 MAY (exp. 39) vs 40.7 APR

Germany ZEW Economic Sentiment 10.8 MAY (exp. 19) vs 23.4 APR

Germany Wholesale Price Index 2.4% APR Y/Y vs 2.2% MAR

Germany Producer Prices 2.4% APR Y/Y (exp. 2.5%) vs 3.3% MAR

0.2% APR M/M (exp. 0.3%) vs 0.6% MAR

UK Jobless Claims Change -13.7K APR vs -5.4K

UK ILO Unemployment Rate 8.2% MAR Y/Y (exp. 8.4%) vs 8.3% FEB

France CPI 2.4% APR Y/Y vs 2.6% MAR

Italy CPI 3.7% APR Final Y/Y vs 3.8% MAR

Italy Industrial Orders -14.3% MAR Y/Y vs -13.2% FEB

Spain Q1 GDP Final -0.3% Q/Q vs -0.3% in Q4

Spain Q1 GDP Final -0.4% Y/Y vs +0.3% in Q4

Austria CPI 2.3% APR Y/Y vs 2.4% MAR

Switzerland Credit Suisse ZEW Survey -4 MAY vs 2.1 APR

Switzerland Producer and Import Prices -2.3% APR Y/Y vs -2.0% MAR

Portugal Unemployment Rate 14.9% in 1Q vs 14% in Q4

Portugal Producer Prices 3.6% APR Y/Y vs 3.7% MAR

Finland CPI 3.1% APR Y/Y vs 2.9% MAR

Netherlands Retail Sales 2.2% MAR Y/Y vs 1.1% FEB

Slovakia CPI 3.6% APR Y/Y vs 3.8% MAR

Slovakia Industrial Orders 13.5% MAR Y/Y vs 10.6% FEB

Interest Rate Decisions:

(5/16) Iceland Sedlabanki Interest Rate HIKE 50bps to 5.50%

The European Week Ahead:

Sunday: NATO Summit in Chicago

Monday: European Parliament Plenary (May 21-24); Mar. Eurozone Construction Output; Mar. Eurozone Current Account

Tuesday: Eurozone OECD Economic Outlook; May Eurozone Consumer Confidence – Advance; Apr. UK Public Finances, Public Sector Net Borrowing, CPI, Retail Price Index; Mar. UK ONS House Price

Wednesday: Summit of EU leaders to Discuss Growth; Mar. Eurozone Current Account; May UK CBI Trends Total Orders and Selling Prices; Apr. UK Retail Sales; May Italy Consumer Confidence; Mar. Greece Current Account

Thursday: May Eurozone PMI Composite, Manufacturing, and Services – Advance; May Germany PMI Manufacturing and Services – Advance, IFO Business Climate, Current Assessment, and Expectations; 1Q Germany GDP – Final, Domestic Demand, Exports, Capital Investment, Govt Spending, Construction Spending, Imports, Private Consumption; Apr. UK BBA Loans for House Purchase; 1Q UK GDP, Private Consumption, Govt Spending, Gross Fixed Capital Formation, Exports, Imports, Total Business Investment, Index of Services – Preliminary; May France PMI Manufacturing and Services – Preliminary, Production Outlook and Business Confidence Indicator; Mar. Spain Mortgages-capital loaned; Mortgages on Houses

Friday: Jun. Germany GfK Consumer Confidence Survey; May France Consumer Confidence Indicator; Apr. Spain Producer Prices; Apr. Italy Hourly Wages, Retail Sales

Matthew Hedrick

Senior Analyst