Conclusion: There is only one issue that matters here...and that's the trade off between operational execution and financial engineering. The latter is easy, but when you run out of net cash -- like GPS is doing -- execution is critical. We won't hang our hat there.

Before we get all excited about the GPS quarter (they were 'Congratulated' half a dozen times in the Q&A), lets consider the following. Yes, sales were up 6%.That's great for a company that has comped down for the better part of 4 US Presidential Terms. But a) it faced an easy compare vs last year, b) weather helped, c) the Easter shift was a factor, and what no one is talking about, d) JC Penney just printed a 21% decline in sales. If GPS garnered only 1/10th of that, it helped comps by over 2%.

But here's our favorite stat. Depite the boost in sales, net income was flat. But EPS was up 18%. Share count vs last year? Down 18%.

Make no mistake, this has been a financial engineering story over the past 8-years. $11bn in repo has taken down the share count by 47%. As recently as 3-years ago, GPS was sitting on a net bash position of $2.3bn. Now it is down to $400mm. In other words, this did not need to be an operational improvement story to grow earnings. Now the share repo angle is largely over. GPS absolutely NEEDS to show consistent comp and/or margin improvement.

Does it have the next quarter or two in the bag? Probably. It goes up against two very easy quarters, and JCP will continue to hemorrhage share for at least a few quarters. But GPS has already conceded that it will reinvest some of its Avg Unit Cost savings back into price and product in 2H. We think that it will have to invest much more than it plans.

We don't like this one.

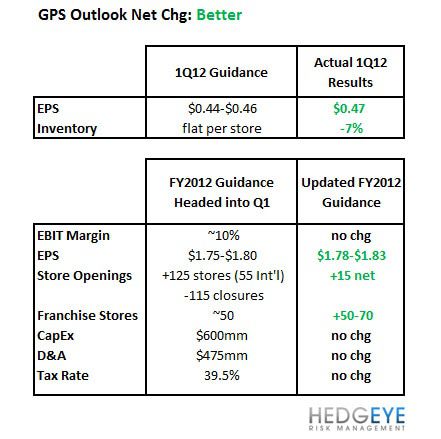

Outlook: In order to properly measure performance relative to original expectations, we look at management’s first quarter results relative to management guidance as well as any updates to previously provided full year 2013 outlook:

Highlights from the Call:

Domestic strength across all three concepts

In the process of making product corrections first highlighted back in Feb

Online up +18% - investing in online media, mobile tech, etc.

Believe they have a competitive advantage in online - gaining share

Growth initiatives:

Franchise business added 3 new markets & 22 new stores

China added 7 new stores - on track for 30+

Athleta on track to add 25 stores

Product:

Old Navy - redesigned t-shirt business in Q1

Gap - color bottoms and color denim big driver in Q1

Marketing Investments:

Five new creative platforms

Gap - Be Right received well

BR - work good execution through direct mail

New Hire: Stephan (from H&M) to run Old Navy

Joining in October

Global experience - key for expanding Old Navy's success domestically

Sales +6% on comps up +4%

Higher AUC

Margins down only -15bps

New stores and franchise business accounted for 2pt spread

GM: -15pbs

AUR up

Merchandise margin down 150bps driven by higher unit cost

Occupancy costs leveraged 130bps (cautioned against extrapolating this level of leverage due to timing of openings etc)

Inventory: Inventory /store -7%

OpEx:

Up $62mm to $980mm due to marketing spend and store payroll

Marketing up $20mm to $139mm

BS:

CapEx = $148mm (net sq. ft. down -2%)

FCF = $216mm vs 104 yy

Cash $2Bn

SRA = $1Bn (Minimal repo in Q1)

Outlook:

FY:

Weather was very favorable in Q1

Includes 53rd week

Modest top-line growth

Healthy merchandise margin

Expect AUC to improve yy in 2H

Saving to be offest in part by reinvestment in product

Expect leverage on positive comps

Will be investing more in domestic growth initiatives - don't expect operating leverage this year

Marketing investment step up to be similar in Q2 to Q1 = ~$20mm

With over 200mm shares repo'd in 2010-2011 at avg price of $19.60 comfortable with slower pace in 2012

Q&A:

Product Costs vs. Outlook:

- Feel good about AUC in 2H; It’s the AUR piece that will have to 'play out' as the year goes on

- Expect to cont. to increase store payroll and investment

- Minimal share repo will impact how EPS modeled

Avg. Unit Costs:

- Entire 2H up 20% including holiday

- Reinvesting some of those costs coming off into categories like suiting at BR, Denim at Gap

- More Gap Fit (i.e. athletic pants) are higher AUC than panties so less favorable mix shift

- Re units, as pressure on AUC eases - pulled back most units on Old Navy given AUC increases so plan to increase units this year as costs subside

Concept Callouts:

- Happy with new Gap Fit business

- Kids and baby business very strong - broad based strength at Gap

- At Old Navy new t-shirt initiative - wish they had more colored bottoms

Uses of Cash:

- Share repurchase has been 'lumpy - wouldn't read too much into it'

- Quick move in stock so program didn't keep pace / catch up

Inventory:

- Were up +10% last yr, down -7% in Q1

- A little lean in Old Navy headed into Q2

Marketing Spend:

- Seeing increased traffic and sell-through at Gap

- Ramping direct mail effort and online at BR

- More marketing behind Gap brand to showcase product (athletic fit & t-shirts)

- Expect a step up in traffic from spend

Operating Expense:

- Store growth will increase absolute rent investment

- Plan to make investments this year in the domestic business

- In 2008-2011 the expense base has stayed relatively flat despite int'l expansion

- Now that they are seeing product assortment improvements, they want to propel those initiatives

Old Navy:

- Final changes to value proposition will be in place by end of May = sharper pricing, assortments

- Merchandising and store team element key to success from June on when chgs should be reflected

Competitive Share Gain:

- Old Navy is not JCP's #1 competitor

- Sure everyone in value business got a little piece

Athleta:

- Productivity /ft is very impressive

- Team has brought a leading operating example to Gap Inc.

International - Old Navy Expansion:

- Japan had a +13% sales increase in the quarter

- China committed to 30 stores - did 7 in Q1

- Franchise business up 30%+

- Modeling after successful global model for Japan intro - push model, very little localization

Customer Demo:

- Opportunity for more customer in the mid 20s-30s

- Brand hasn't been as relevant to them in recent years

- New marketing pulling in broader consumer set

Piperlime Transition to Physical Store Model:

- Taking blue print from Athleta

- Have a central design team for the stores to bring the brand to light

Product & Price:

- 2011 didn’t stay true to value proposition that they offered in 2010, they just have to get back there - 'tweak it'

Operating Margin Cadence:

- More spend in 2H?

- No real chg to view

- Expect some top-line and margin expansion in 2H as deleverage expenses