TODAY’S S&P 500 SET-UP – May 16, 2012

As we look at today’s set up for the S&P 500, the range is 34 points or -0.50% downside to 1324 and 2.05% upside to 1358.

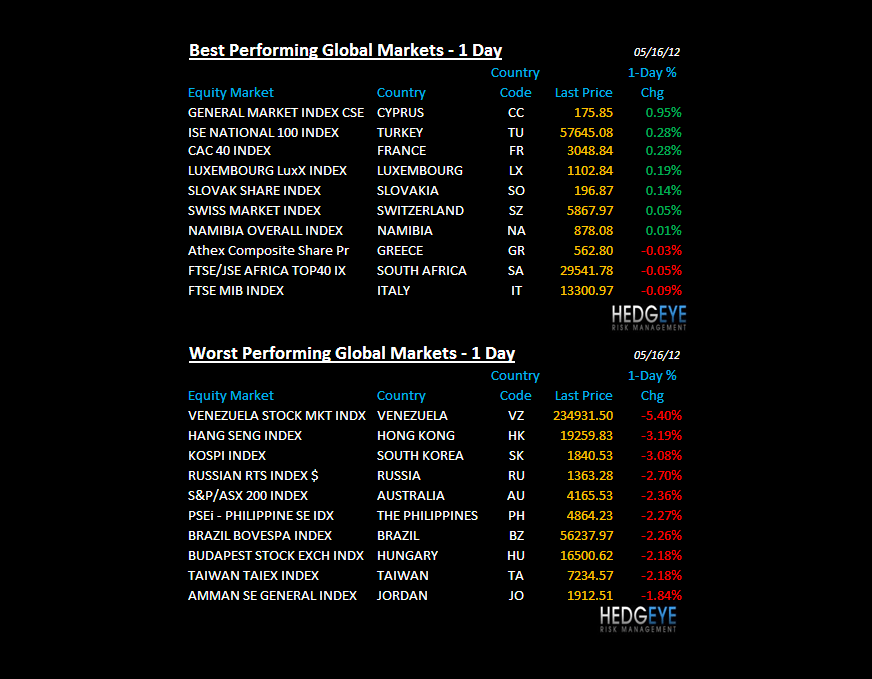

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 5/15 NYSE -926

- Up from the prior day’s trading of -2114

- VOLUME: on 5/15 NYSE 868.62

- Increase versus prior day’s trading of 8.20%

- VIX: as of 5/15 was at 21.97

- Increase versus most recent day’s trading of 0.46%

- Year-to-date decrease of -6.11%

- SPX PUT/CALL RATIO: as of 05/15 closed at 2.35

- Down from the day prior at 2.50

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 38

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.77

- Unchanged from prior day’s trading

- YIELD CURVE: as of this morning 1.50

- Unchanged from prior day’s trading

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: MBA Mortgage Apps., week of May 11 (prior 1.7%)

- 8:30am: Housing Starts, Apr., est. 685k (prior 654k)

- 8:30am: Housing Starts (M/m) Apr., est. 4.7% (prior -5.8%)

- 8:30am: Building Permits, Apr., est. 730k (prior 764k, revised)

- 8:30am: Building Permits (M/m) Apr., est. -4.5% (prior 4.5%)

- 8:30am: ECB monetary policy conference; participants include President Mario Draghi

- 9:15am: Industrial Prod., Apr., est. 0.6% (prior 0.0%)

- 9:15am: Capacity Util., Apr., est. 79.0% (prior 78.6%)

- 9:15am: Manufacturing (SIC) Production, Apr

- 10:30am: DOE Inventories

- 12:30pm: Fed’s Bullard speaks on economy in Kentucky

- 2pm: Minutes of April FOMC Meeting

GOVERNMENT:

- House, Senate in session:

- Senate Health holds hearing on health care delivery systems, with Coastal Medical, Humana officials, 10am

- Senate Commerce holds oversight hearing on FCC, with Chairman Julius Genachowski, 2:30pm

- House Financial Services subcommittee holds hearing on effects of Dodd-Frank Act, 10am

- House Ways and Means panel holds hearing on tax-exempt organizations, 10am

- House Financial Services subcommittee holds hearing on market access for U.S. financial firms in China, 2pm

- House Financial Services panel holds hearing on FDIC oversight with Lennar Corp. CEO Stuart Miller, 2pm

- House Small Business holds hearing on U.S. trade agenda, 1pm

- World Bank President Robert Zoellick speaks at Economic Club of Washington, 12pm

WHAT TO WATCH:

- FOMC releases minutes of April 24-25 meeting

- Facebook said to increase size of IPO to 421m shrs

- Housing starts in U.S. probably rebounded from five-month low

- Euro-region inflation slowed in April, March exports dropped

- U.K. unemployment unexpectedly falls in sign of stabilization

- Greek leaders meet on new election after European stocks fall

- Carlyle said to seek $3.5 billion for fourth Asia buyout fund

- Berkshire Hathaway took new stakes in Viacom, General Motors

- Verizon in $63 billion faceoff with AT&T over family plans

- Investor Whitworth holds $610m PepsiCo stake, meets w/ co.

- GE to buy U.S., Australian mining-equipment cos.

- Australian consumer confidence stagnates near year’s lows

- Soros, Eton Park raised gold ETP holdings before price drops

- House Financial Services subcommittee holds hearing on effects of Dodd-Frank Act

- NYSE Euronext removed from bidding for London Metals Exchange

- EADS 1Q profit misses est.; raises 2012 EPS outlook

EARNINGS:

- Staples (SPLS) 6am, $0.30

- ValueVision (VVTV) 6:30am, ($0.19)

- Chico’s FAS (CHS) 6:55am, $0.30

- Deere & Co (DE) 7am, $2.53

- Abercrombie & Fitch Co (ANF) 7am, $0.01

- Sears Canada (SCC CN) 7am, C$0.03

- Target (TGT) 7:30, $1.01

- Brady (BRC) 8am, $0.57

- Eagle Materials (EXP) 8:30am, $0.24

- Hot Topic (HOTT) 4pm, $0.08

- Ltd Brands (LTD) 4:30pm, $0.40

- Ctrip.com (CTRP) 5pm, $0.17

- Netease.com (NTES) 6pm, $1.01

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

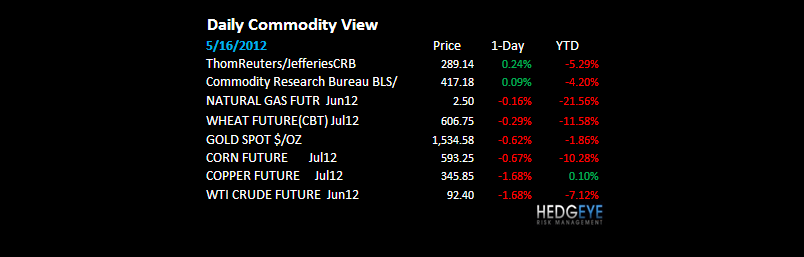

COMMODITIES – definitely seeing some capitulation in Bernanke’s Bubbles (our Top Macro Theme issued in April) – Gold finally oversold at -14% from its YTD high; Copper getting spanked -1.7% to immediate-term oversold (-12% from its Feb Growth Slowing high).

- Commodities Drop Near Five-Month Low on Greek Euro Exit Concern

- Gold Eclipsed by Dollar Haven as Goldman Sees Rally: Commodities

- Palm Oil Slumps Most in 14 Months in Record Volume on Euro Debt

- BHP Won’t Meet $80 Billion Spending Target as Minerals Fall

- Gold Tumbles Into Bear Market on Concern Greece May Leave Euro

- Copper Drops for Fourth Day as Greece Remains Without Government

- Corn Declines as U.S. Planting Nears Completion, Lowering Risks

- Sugar Falls as Brazil’s Weaker Currency May Accelerate Exports

- NYSE Euronexit Is Removed From Bidding for London Metal Exchange

- Crude Palm-Oil Futures Volume Reaches Record 63,019 Contracts

- Soros, Eton Park Raised Gold ETP Holdings Before Price Drop

- Seaway No Guarantee for Goldman’s WTI-Brent Bet: Energy Markets

- Eni Follows BG, Anadarko With More Gas Finds off Eastern Africa

- Inmet Capitalizes on Junk Demand for Copper Mine: Canada Credit

- GSCI Index Decline to Near Five-Month Low

- Oil Drops to Six-Month Low on Rising Stockpiles, Greek Crisis

- Rubber Falls to Four-Month Low as Greek Woes May Cut Demand

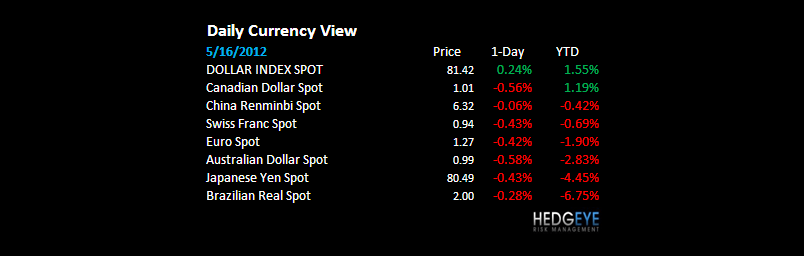

CURRENCIES

EUROPEAN MARKETS

EUROPE – we don’t see Greece “leaving the Euro” anytime soon (pundits might, but the market doesn’t either or the Euro would catch a bid – weakest stores (countries) stay in the currency base and Euro goes to $1.22); what we do see is capitulation (immediate-term) to oversold lows in Spain and Russia this morning (crashing markets, down -26% and -22% from their YTD tops).

ASIAN MARKETS

JAPAN – probably the most misunderstood and under-reported situation in the world right now is Japan (Nikkei down 21 of the last 28 days = -14.2% draw-down) and the BOJ just saw the lowest demand (1st shortfall vs the 600B they wanted to issue) for JGBs since Oct 2010. Greece is nothing compared to this.

MIDDLE EAST

The Hedgeye Macro Team