Conclusion: As we expected, DKS is firing on all cylinders (FW, Apparel, Team Sports & Golf) for the first time in a long while. Improvement in hardlines were driven by baseball bats and golf equipment as expected with the later coming in even more robust than even we expected. While some of the outperformance can be attributed to a pull forward in sales, the product cycle continues to improve while DKS’ compares are relatively easy. In addition, there were several developments during the quarter (Top-Flight acquisition, JJB stake, Bubba’s Pink Ping Driver in June, etc.) that represent a series of positive intermediate-term drivers. Expectations for the balance of the year continue to look flat out conservative to us.

What Drove the Beat?

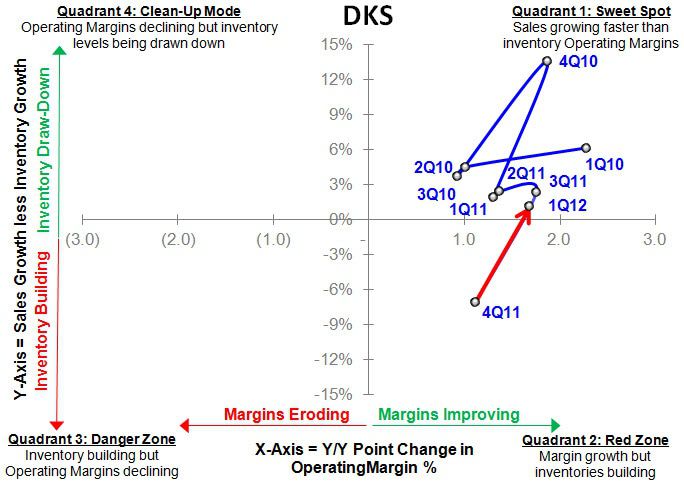

Solid quarter from DKS coming in $0.07 above the top end of its range and consensus expectations driven by higher sales and gross margins. Revenues came in strong up +15% a little better than our expectation for +14%E and the consensus of +10.5%E, but the real callout in the quarter is inventory management reflected in better than expected gross margins, which were up +112bps on stronger sales despite clearance activity and higher equipment sales mix.

Deltas in Forward Looking Commentary?

In order to properly measure performance relative to original expectations, we look at management’s first quarter results relative to management guidance as well as any updates to previously provided full year 2013 outlook:

Highlights from the Call:

- Aggregate comps up +8.4%

- Comps at Dicks up +7.3%

- FW, App, and hardlines all positive

- +4% sales per transaction

- +3.3% in traffic

- GolfGalaxy +12.6%

- E-Commerce +33.4% (~3% of total sales)

- Expect to open 38-40 stores in 2012; 50/50 new vs. existing markets

- Continue to shift product mix to higher margin private label (acq. Top-Flight) and key brands via shop-in-shops (NKE, UA, The North Face)

- Price, size, and packaging optimization starting to bear fruit

- New store productivity up +105.8%

- Opening 4th DC in Jan ’13, 600k sq. ft. facility in AZ; w/DC in DC can support 750 stores

- Targeting ship-from-store capability in 2012

Q2 Outlook:

- Comps up +2-3%

- GM: modest increase

- SG&A: modest leverage

- EPS $0.62-$0.63

GM: +112bps due to:

- Occupancy leverage (+120bps)

- Merch margin down modestly (-8bps)

- Cold weather apparel inventory clearance now complete

- Some due to clearance of fitness equipment

SG&A: up +12%; -58bps due to:

- Payroll leverage

- Lower advertising

BS:

- Cash = $521mm

- Share repo = 2.1mm shares at $49.39/sh = $104mm

- Completed SRA yesterday purchased total 4.1mm shares

- Purchased store-support center for $133mm

Q&A:

Bat replacement cycle contribution:

- Less than 1pt to comp

- Isolated benefit to Q1

Occupancy Leverage:

- Need +3% to lever

Lease Duration:

- 10yr term lease structure preferred going forward

Private label

- Top-Flight margins 2bps higher than other brands

Competitive Pricing Environment

- Seeing rational pricing in the space

- 'think we did better than most'

Cold Weather Overhang Impact:

- Primary impact on merch margin in Q1

- NFL jerseys for Q4 should be very helpful to margin rate

Store Opportunities:

- Cont to look at big box opportunities - ex BBY, KMart, SHLD, Linens space

- Planning on ~40 stores/yr, maybe 45

Footwear:

- One of better performing categories in the qtr

- New product expectations positive

- Expect positive momentum to continue

JJB Investment:

- 'this is a high risk, very high reward investment'

- JJB has only 6%-7% of ~$9.5Bn UK market - 'see a big opportunity' for share gain

Shop-in-Shops:

- NKE ~50 this year

- UA ~80 add'n stores

- Adding North Face shops as well