A new quarterly record

Singapore gross gaming revenues rose 11% YoY and 9% QoQ to a new quarterly high in Q1 2012. GGR crossed the S$2 billion mark to S$2.093 billion. For comparison, Macau GGR grew 1% QoQ and 27% YoY in Q1. Singapore property EBITDA rose 3% QoQ to S$985MM, also setting a new record.

VIP RC grew QoQ by 22%, but was down slightly YoY at S$31.7BN and 14% below the market high set in 3Q11. Mass drop and slot handle were up YoY by 4% and 31%, respectively to S$2.8BN and S$6.8BN, however, both categories were down QoQ. YoY we have seen the number of slots and ETG's expand by 20% to 4,919 and the number of VIP tables expand 15% to 315, while Mass table growth has only been 2% to 855.

Q1 hold was 3.49%, slightly lower than Q4’s 3.58% but higher than Q1 2011's hold of 3.25%. Average hold for the 2 IR’s since 1Q10 has been close to 3.09%.

Q1 MARKET SHARES

GGR:

- MBS: 52.3%

- RWS: 47.7%

Net Revenue:

- MBS: 57.5%

- RWS: 42.5%

Property EBITDA:

- MBS: 60.7%

- RWS: 39.3%

Mass Table Revenue:

- MBS: 52.7%

- RWS: 47.3%

Mass Table Drop:

- MBS: 53.4%

- RWS: 46.6%

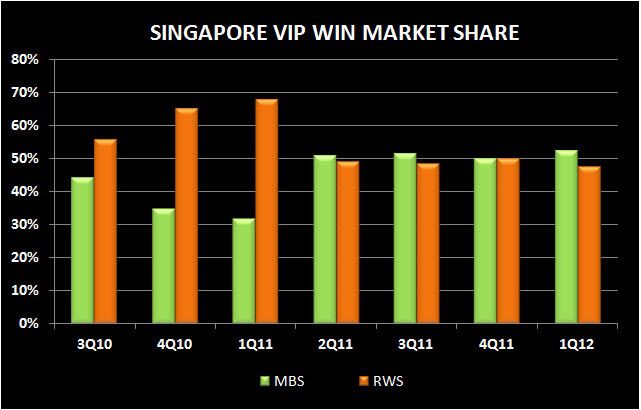

VIP Table Revenue:

- MBS: 52.3%

- RWS: 47.7%

VIP RC:

- MBS: 51.1%

- RWS: 48.9%

Slot Revenue:

- MBS: 51.2%

- RWS: 48.8%

Slot Handle:

- MBS: 45.7%

- RWS: 54.3%