Conclusion:

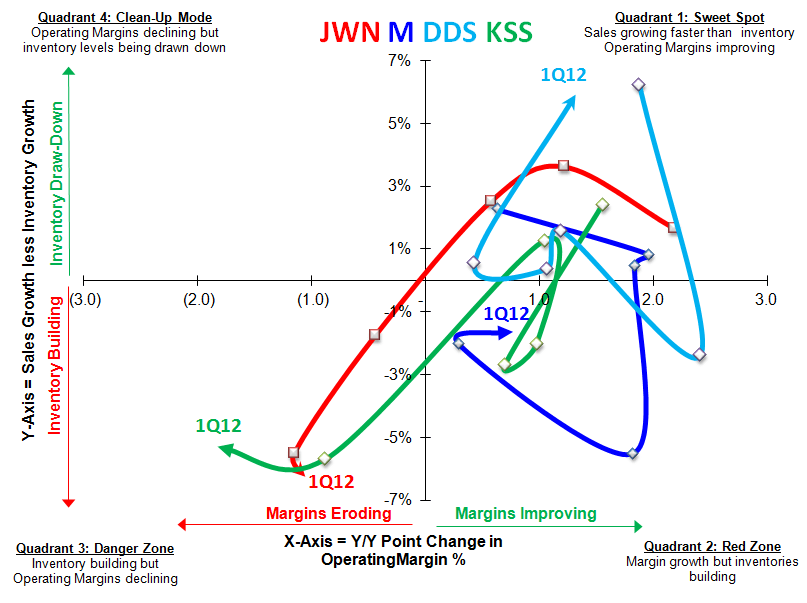

You have to be hiding under a rock not to know that things got worse on the margin in the department store space. First Macy’s, then Kohl’s…but high-quality Nordstrom should be immune, right? Hardly. The good news is that comps (known) were 8.5%, with total sales ringing in at 13.2%. The comp accelerated on both a 1yr & 2 yr basis with categories like high end hand bags as a key area of outperformance. This reaffirms strength we’re perennially seeing in the domestic luxury accessory market, marking a stark contrast to low end retail. The bad news is that with such impressive top line, the company only put up a 2.9% EBIT growth rate. Some people will chalk up the weak margins to one-off investments in e-commerce. But ecommerce is here to stay, and increased investments will need to as well. Also, Free Shipping hurt margins. Free shipping is like sticking a needle in the consumers’ arm – it’s very difficult to wean them off once they get a taste. Lastly, inventory per square foot was +16%, which the company made a noble effort to explain away as not being a concern. We’ll point to the -6% sales/Inventory Spread – just edging out Kohl’s as the worst in the department store space quarter to date, and a sequential decline from -5% last quarter. Then again…JCP has yet to report. Maybe then JWN can hold on to hope that Johnson and team will steal this prize.

What Drove the MISS?

Although credit sales came in slightly better than expectations (flat vs -14E) resulting in total revenues +13.2% vs +12.6E, gross margins came in light -31bps vs +33E resulting from free shipping to fashion rewards customers. With ramped up investment spending largely in line with consensus, operating margins were (-106bps) vs (-35E) driving the nickel miss. Despite strong top line trends with comps +8.5% driving a 100bps acceleration in underlying two years trends, JWN left full year EPS outlook unchanged at $4.30-$3.45 vs. $3.49. The only key delta in full year guidance was a $10mm pullback in credit SG&A to offset an incremental $10mm in retail investment in additional e-commerce enhancements.

Deltas in Forward Looking Commentary?

In order to properly measure performance relative to original expectations, we look at management’s 2012 guidance headed into the quarter as well as the key deltas in Q1 results vs. expectations :

FY2012 GUIDANCE

EPS

- We expect to achieve 2012 EPS of between $3.30 and $3.45, with same-store sales between 4% to 6% UNCHANGED

- Our plan for the 53rd week will increase our annual sales and EPS by approximately $160mm to $170mm and between $0.03 and $0.05, respectively UNCHANGED

Gross Profit

- Our 2012 gross profit rate will range from 5 to 35BPS lower than last year UNCHANGED

- This primarily is a function of the near-record performance of merchandise margin in 2011, along with the unfavorable gross profit impact from an increasing mix of Rack stores, the reduction of shipping revenue, and the introduction of our enhanced Fashion Rewards program

SG&A

- We anticipate retail SG&A to be $265mm to $330mm higher than last year INCREASED $10mm to support additional E-Commerce investment spend

- Credit card revenue is expected to be flat to up $10mm, with no anticipated growth in credit card receivables, due to increased sales volume being offset by higher payment rates UNCHANGED

- Our Credit SG&A expense is expected to be $10mm to $20mm higher compared to last year, primarily due to the absence of planned reductions in our reserve for bad debt REDUCED as an offset to $10mm increase in retail SG&A

EBIT

- EBIT as a percent of sales is planned to be in the range of 11.4% to 11.6% for the year UNCHANGED

- This is a slight decrease from last year and is a function of the increased level of investments we’ve described

- Interest expense is anticipated to increase $25mm to $30mm, largely due to increased borrowings and a higher interest rate relative to last year UNCHANGED

- FCF is planned to be approximately $400mm for 2012 UNCHANGED

Highlights from the Call:

Investment Highlights:

- In E-commerce, made enhancements to the website to improve navigation/checkout and increased the selection of merchandise, added to functionality of apps, improved fulfillment

- Announced partnership with online Men's retailer Bonobos in April

- In March, re-entered Salt lake city market with a store that had 100+ mobile POS devices, 3X the devices as cash registers.

- Can see significant increase in speed of POS which provides better service in full line & Rack

- Saw a favorable response to changes to fashion rewards which were focused on convenience- enrollment in new fashion rewards increase 50% YoY

1Q12 Highlights

- EPS $0.70 +8% YoY

- EBIT $280mm +2.9% YoY

- Total sales +13.7%, Comps +8.5%

- Nordstrom full line & direct comp +9.3% driven by handbags, women's shoe and men's shoes

- Full line Comp +5.6% driven by the South and Midwest

- Direct growth +44.2% YoY

- Rack total sales grew 19.6% with comps +6.8%

- Percentage of regular price sales continued to increase in the quarter

Gross Margin: -31 bps due primarily to enhanced customer loyalty program and the impact of free shipping

Retail SG&A: +110mm YoY

- Half of the increase due to e-commerce growth investments focused on improved selection, convenience and overall service

- Remaining SG&A attributable to sales growth in new/existing stores

Inventory:

- Ending inventory per square foot +16% which are aligned with merchandise plans

- Inventory turn of 5.4X slowed slightly from 2011 inline with expectations but expect improvement throughout the year

Credit Performance

- Rate of decline improved to 4.7% from 7% a year ago

- Reduced the reserve for bad debt by $10mm (percent of total 5.2%, down from 6.7% LY)

Share Repurchase:

- 800K shares in Q1 at avg price of $50.79 for total of $40mm

- $1.1bn remains in authorization

Outlook:

- EPS outlook remains unchanged

- Increase Retail SG&A by $10mm due to increase e-commerce investment spend

Comps:

- 2Q: +LSD

- 3Q: +HSD

- Full year : +4-6%

Gross Margin:

- 2Q: -70-90bps

- 2H: -10 to +10bps

- Full year: -5-35bps

Q&A:

Expenses:

- Half of the $110 in expense increase due to stores which achieved percent to sales leverage

- Retail SG&A deleveraged in the Q

Fashion Rewards:

- Roughly 1/3 of overall volume done on various tenders

- Started offering rewards in the rack

- Still have same program as last year with the anniversary sale (rewards customers can shop early)

Guidance:

- Guidance implies stronger GM in 2H

- Believe back half earnings will be stronger than 1H

E-commerce Growth:

- Strong DD comp increase last year relative to 44% growth in 1Q12

Investment Spending:

- 2012 saw a step change and accelerating moment in investment spending

- Expect these investments will help achieve long term goals

Women's

- Always looking to be most effective with space

- Continue to find ways to add energy to second and third floors

- Still working on hiring executive role to head up women's

- Performance on the whole has been challenging- more modern casual side has been improving

Hautelook

- Expect to do 50-60% sales increase

- Company is currently on plan with very good momentum

- Will continue to be JWN's primary online offset concept

53rd week impact

- $0.03-$0.05 impact

Brooks Brothers Partnership

- Big part is them understanding the JWN customer

- Great relationship so far with promising early read

Anniversary Sale:

- Always want to start the event on a Friday

- Eventually the event gets pulled back a week due to timing

- Nothing unusual driving the move

Inventory turns:

- Slowdown was built into the plan as it relates to new stores and growth in direct

- Position last year had greater turns

POS device Functionality

- Functionality is currently at ~75%, will reach 100% by the end of the year

- Will rollout more in 4Q

- Planning an additional larger rollout in 1Q13 once POS devices hit full functionality

Amazon:

- JWN focused on serving customers on their terms

- Now and going forward, how customers define service, continues to change

- Making a lot of investments in capabilities around those areas and see good opportunity to build on capabilities and serve customers on their terms

Rack Profitability:

- Rack continues to be a terrific opportunity to deploy capital

- Will continue to grow at 15 stores a year

- Are seeing no deterioration in the stores that have been opened

E-commerce:

- Growth of 44%

- If growth remains on track, could increased SG&A spend continue into 2013

- Opportunity capture a lot more customers and continue to grow

- A lot of the capabilities needed to enhance e-commerce requires more of the right people which is happening now

- SG&A beyond 1H12 should be a slow growth rate than current due to hiring happening no

1Q Gross margin -30bps

- Merchandise margin was roughly flat to last year

- Predominantly related to fashion rewards and free shipping

Rack Concept:

- Synergy between rack and full line stores

- Continue to see a healthy relationship between the two formats- beneficial to both

- Continues to be customer movement back and fourth between full line and nearby rack

Inventory on hand

- Inventories will be slightly higher coming out of Q2 because there will be one additional week at the start of Q3 for the anniversary sale