Conclusion:

KSS is finally taking steps to adjust its pricing strategy a full quarter after JCP implemented its new EDLP approach in February. We’re rarely (if ever) a fan of reactive strategies and this one is no different. KSS will now be more aggressively fighting for share – that’s great, but others have already been taking it for the last 3-months now such as Macy’s, the off-pricers (TJX/ROST), etc. Increased competition in the mid-tier that will ultimately drive increased margin pressure is here and officially heating up. This isn’t good for KSS, or the companies that rely heavily on this channel for distribution such as CRI, HBI, GIL to name a few.

What Drove the Beat?

KSS posted a very low quality SG&A driven beat for the quarter with both revenues and gross margins coming in soft. A few points of note here:

1) Revenues were light. We knew that last Thursday and now KSS is going to try to drive traffic with lower pricing. This didn’t work out so well for JCP. We expect an uphill battle ahead for KSS as well. Not good.

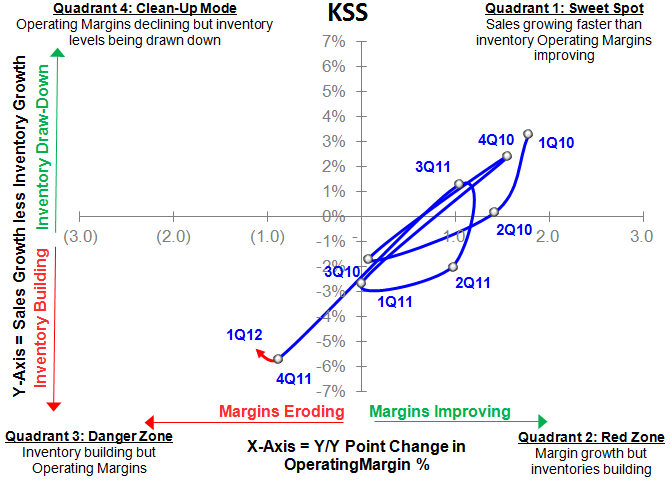

2) Gross margins also came in below expectations. While some portion of this degradation was due to the new pricing initiative, KSS’ sales/inventory spread is virtually unchanged and still among the worst in the mid-tier. That’s very gross margin bearish over the intermediate-term.

3) SG&A was the saving grace in the quarter coming in down (-0.2% adj) yy vs. guidance of +3.5%. We’d prefer to see KSS invest in remodeling some of its tired store base rather than pulling this lever so heavily to make EPS. It may indeed help manage earnings near-term, but that’s no good for F13 earnings growth sustainability.

Deltas in Forward Looking Commentary?

In order to properly measure performance relative to original expectations, we look at management’s 2012 guidance headed into the quarter as well as the key deltas in Q1 results vs. expectations :

Q1 FY2012

- We’re projecting a total sales increase of 3%, comparable sales increase of 1% MISS: Sales +2%, Comps +0.2%

- By month, we expect February to be slightly below the quarterly guidance, March to be higher than the quarter, and April to be slightly below the quarter INLINE: KSS missed consensus 2/3 months

- We’re projecting a gross margin rate decline of 160BPS MISS: Gross Margins down 220bps due primarily to increase promotional activity

- SG&A expense dollars are projected to increase 3.5%, depreciation expense of $205mm, interest expense of $81mm, a tax rate of 38%, share count of 245mm diluted shares LOWER: SG&A -0.2% (adj), tax rate of 36% added $0.01 to EPS

- And we’re also projecting share repurchases of about $305mm for the quarter, at an average price of approximately $53 per share

- Including these estimated share repurchases, we expect earnings per diluted share to be $0.60 for Q1 BEAT: $0.63 vs $0.60

Full Year 2012

- The following metrics are for FY2012: Total sales increase of 4.5% UNCHANGED

- Excluding the impact of the 53rd week, we expect total sales to increase 3.5% UNCHANGED

- A comparable sales increase of 2% UNCHANGED

- A gross margin rate decline of 70BPS. UNCHANGED though not reiterated due to incomplete fall spending; 2Q SG&A to be down 200-250bps with 2H SG&A down YoY

- SG&A is expected to increase about 3% for the FY, and 2% if you’re excluding the 53rd week UNCHANGED

- Including estimated share repurchases, we expect earnings per diluted share to be $4.75 for FY2012 UNCHANGED

CAPITAL SPENDING, NEW STORES OPENINGS AND REMODELS

- From a capital spending perspective, we expect CapExs to be approximately $825mm in 2012 UNCHANGED

- We expect to open 20 new stores in 2012, eight in March and 12 in October REDUCED- Opened 9 stores in Q1 with 10 planned for the fall

- We’re temporarily reducing the number of remodels to approximately 50 stores in 2012, as we look to potential changes to our stores to increase sales productivity as well as provide more efficiency UNCHANGED- remodeled 40 in Q1 with 10 planned for the Fall

Highlights from the Call:

Revenues:

- Sales +1.9%, Comps +0.2%

- AUR +4.9%, UPT -3.3%=average trans +1.6%

- Transactions/store down (-1.4%)

- E-Commerce: +34% ~$250mm

- Private/Exclusive brands were 53% of sales

- Growth was hindered by lack of inventory units in stores (entered quarter down 6% in units and 9% in seasonal categories)

- Seasonal category unit inventory was down as much as 20% in the quarter

- Planning unit inventory flat at the end of Q2 to drive sales demand though levels will continue to hinder 2Q top line

Category Performance

- Men's, Children's & Accessories outperformed the company average

- Men's strength in casual sportswear, basics, dress shirts and young men's

- Children's led by boys & girls

- Accessories strength in fashion, handbags, sterling silver & watches

- Women's essentially flat- active and updated sportswear strongest +LDD

- Footwear slightly negative despite LDD growth in women's shoes

- Home down LSD; strongest performance in tabletop, bath & towels

- Sales in Rock & Republic exceeded expectations

Regional Performance:

- Cold regions outperformed warm (Mid Atlantic, Midwest, Northeast vs. South Central, Southeast, West)

- Midwest & Northeast +LSD

- Southeast and South Central down (-LSD)

- West down (-MSD)

Store Productivity Testing:

- Testing 50 store in Houston, Atlanta, Salt Lake City

- Test includes expanded home selection

- Expect to add 2 additional markets with 20 stores for back to school

- Will make changes to remodels based on results of testing

Credit:

- Credit share 56%, +270bps

Gross Margin:

- GM (-220bps; had guided to -160bps)

- Difference between actual -220 vs expectations -160 primarily due to promotional markdowns

- Clearance levels similar to expectations

- Gross margin guidance reflects customer response to new reduced pricing strategy

SG&A

- SG&A -0.2% adjusted (had guided to -3.5%)

- Credit business generated leverage in the quarter which is expected to moderate

- Most all stores reported lower costs as percent of sales

- Strongest improvement in store payroll

- Advertising did not leverage due to support of new brand launches

D&A: $201 vs. $191 last year

- Increase due to new stores & additional e-commerce fulfillment centers

Interest Expense: +$6mm YoY

- Due to $650mm of long term debt issued in October 2011

Stores:

- Currently 1134 stores, opened 9 stores, relocated 1, closed 1 in 1Q12

Inventory: +7%

- Inventory/store +3.7%

Capex: $177mm vs. down $44mm YoY

- Decrease reflecting lower spending on remodels/new stores/e-comm fulfillment partially offset by higher technology spending.

- Opened 9 stores this year & last year; planning 10 stores this fall vs. 31 last fall.

- Also reduced remodel plans from 100 last year to 50 this year.

- Remodeled 40 stores in Q1 with 10 planned for the fall

- Spending on 4th e-commerce facility ramping now

Guidance

2Q Guidance:

- Sales +2-3%, comp sales flat to +1%

- Expect May below, June in line and July well above quarterly comp

- GM decline of 200-250bps

- SG&A will be flat to +1.5%

- Depreciation of $206mm

- Interest Expense of $80mm

- Tax rate of 38%

- Share count 241mm diluted shares (repurchasing $250mm at an avg price of $50/share

- Expecting EPS of $0.96-$1.02

Full year

- EPS remains at $4.75/share

- Expect Gross margin to improve in the fall season but remain down YoY

- Apparel costs are down for the Fall season in the MSD range which will help gross margins

Q&A

Marketing Program:

- Advertising expenses deleveraged in 1Q, would not expect leverage in 2Q

- Expect to do better on the comp with more units in 2H and hope to leverage marketing in the back half

- Lapping launch spend for Jlo in 2H which should create leverage

- Customers will see price points very clearly in new ads and in the store

- Message will be that it is exciting to shop value in stores

Operating Expense Control:

- Saved on electricity spending in the quarter, spending down 4-5% in 1Q

- Majority of savings came from store payroll

- Saved on snow control in the quarter from more mild winter

Market Share Opportunities:

- Biggest opportunity remains internal, a lot of changes taking place in the industry

- Generating store to store success that has been seen in the past will be a result of better pricing, better product

- Understand the changes that need to be made to the merchandising assortment

Result of Pricing Strategy:

- Reduced a lot of opening price points in private brands which resulted in an acceleration in unit demand

- Dramatic change in sell through as pricing was adjusted

- Did not have the depth of inventory to support the unit growth which translated into the top line

- Did well with newer brands in the portfolio (Rock n republic, J Lo, Marc Anthony)

- Changing the value is making a difference in how customers view the product

- Majority of gross margin pressure was in the private brands where prices were taken down the most but costs increased the most

Inventory:

- Starting to see cost reductions so units might be up but costs down

- Inventory up 3.7% on a per store basis

- Units were down 6% in stores, expect to end the store on a unit basis as flattish

- Expect 2Q inventory to be up MSD-HSD on a per store basis

- Will be less aggressive on classic inventories on the missy side

- Inventory growth will not be across the board- being smart about unit opportunity

- Private brands were definitely hurt by the lack of units

Merchandising Opportunity:

- Biggest opportunity is holiday

- Really underperformed in 4Q11 in particular around more gift related categories- focus of 2012

- Opening price point was an area of underperformance which was a function of more inventory support

- 30% plus of the business is opening price point private brands

- Need to continue to introduce news brands and will have announcements to share later in the Q but its more important to have new styles and new colors

Credit Uptick

- Not coming from approval rates, new approval requirements have made this more difficult

- Making changes from the scorecard perspective in June/July that should help approval

- Really showing that you can get additional value by signing up for a Kohl's card

- Expect the credit rate to continue to increase over time

- Credit increase near $20mm- will continue to be a benefit throughout the year but not as good

- Credit built into the guidance

JC Penney:

- Difficult to quantify without knowing sales

- If sales were up YoY, KSS most likely lost share to JCP

Comp cadence:

- Missed a great deal of business in July last year resulting in this year's July comp above the quarter

- Ran 2 credit events in June last year so comp expected to be in line with the quarter

- Feel the company will be better positioned to drive sales later in the quarter

New store prototype/store remodels

- Testing the expansion of home

- Looking at other areas that aren't as productive as the overall stores but tests wont be done in 2013

- Expectation for new stores in 2013 continues to be ~20

- Remodels- will most likely stick to 50 remodels in 2013 based on test results

SG&A- Online infrastructure spend:

- Guiding to an SG&A leverage point of 2%

- Undergoing a profit improvement project throughout the entire company (5 total)

- Expect to finish 2/5 projects by the end of year

Fashion Trend Response:

- Experience in fall/holiday caused the company to rethink the entire buying process

- Not dissimilar to 9 years ago when the company required a full rethink

- There have been a tremendous amount of changes primarily in the buying and planning organizations

- Focus around exclusive brands and the need to be more trend right has caused changes in the product development area as well

- Working to buy more product on trend- merchants are chasing sales

New Prototype

- Driven by e-commerce, recognition that online which continues to grow at a high rate is a potentially cannibalization of brick and mortar retail

- Thinking long term in terms of sustained high growth in e-commerce and what it means for brick and more locations

Elasticity in Kid's

- 2 areas where it was clear pricing would change trajectory of demand were children's apparel and broadly across the store in great value/key items (not in one particular category)

- Saw acceleration in sell through rate as pricing was adjusted

- Solid basis backing pricing decisions being made for the Fall

Full year Gross Margin:

- Have not complete fall plans but expect margins to be down in the fall though improved over 1H

- SG&A could be better than Fall guidance

- Full year unchanged but not reiterated

- Stock buyback of 250 in 2Q could be conservative, considering additional debt in 2H to buy back more stock

Executive changes:

- New executive team will be driving the e-commerce business

- Could accelerate growth even further in Fall Winter

- Have made changes that could have major impact in juniors business during back to school

- Certain areas will be impacted faster than others

Store Growth

- Will continue to open stores which is largely above the rate of competitors

- Objective about the need to solve some internal issues and will be in a position to consider new opportunities to grow

- New stores have not been hitting the pro forma over the past couple of years due to the economy being different than it was when initial plans were in place

- Could accelerate the 20 store growth as new store productivity improves