TODAY’S S&P 500 SET-UP – May 10th, 2012

As we look at today’s set up for the S&P 500, the range is 21 points or -0.63% downside to 1346 and 0.92% upside to 1367.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 5/09 NYSE -1080

- Down from the prior day’s trading of -613

- VOLUME: on 5/09 NYSE 940.15

- Increase versus prior day’s trading of 4.2%

- VIX: as of 5/09 was at 20.08

- Increase versus most recent day’s trading of 5.4%

- Year-to-date decrease of -14.2%

- SPX PUT/CALL RATIO: as of 05/08 closed at 2.03

- Up from the day prior at 1.31

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 38.05

- 3-MONTH T-BILL YIELD: as of this morning 0.09%

- 10-Year: as of this morning 1.89

- Decrease from prior day’s trading at 1.82

- YIELD CURVE: as of this morning 1.65

- Down from prior day’s trading of 2.03

MACRO DATA POINTS (Bloomberg Estimates):

- 7am: Bank of England MPC rate decision, asset purchase target

- 8:30am: Import Price Index, Apr., est. -0.2% (prior 1.3)

- 8:30am: Trade Deficit, Mar., est. -$50.0b (prior -$46.0b)

- 8:30am: Initial Jobless Claims, week of May 5 (prior 365k)

- 8:30am: WASDE corn, cotton, soybean, wheat

- 9:30am: Fed’s Bernanke speaks on bank capital in Chicago

- 9:45am: Bloomberg Consumer Comfort, wk of May 6 (prior -37.6)

- 10am: Freddie Mac mortgage rates

- 10:30am: EIA natural gas storage change

- 11am: Fed to sell $8b-$8.75b note, 10/15/13 to 1/31/14 range

- 1pm: U.S. to sell $16b 30-yr bonds

- 1:20pm: Fed’s Kocherlakota speaks in Minneapolis

- 2pm: Monthly Budget Stmnt, Apr., est. $30.5b (prior -$40.4b)

WHAT TO WATCH:

- Bank of England expected to halt bond purchases at GBP325b

- Cisco forecast 4Q revenue, profit growth that missed ests.

- Euro diminished in poll showing more than 50% predicting an exit

- Intel hosts investor day; watch commments on capex, gross margin: Stifel

- Hong Kong Exchanges said to submit takeover bid for London Metals Exchange

- Spain takes over Bankia after chairman says he will step down

- ArcelorMittal beats estimates on U.S. steel-demand recovery

- Sony profit forecast misses estimates as TV sales decline

- Australia’s jobless rate falls to 1-year low, currency rises

- Yanzhou Coal among cos. in talks to buy Vale SA’s stake in an Australian coal mine for more than A$500m, people familiar said

- U.K. March manufacturing increases more-than-forecast 0.9%

- Japan posts current-account surplus for a second month

- Bernanke gets 75% approval rating in Bloomberg global poll

- Las Vegas, Atlantic City casino monthly figures may be released

ANALYST RATINGS

- Big Lots (BIG) raised to overweight at Barclays Capital

- General Growth (GGP) raised to buy vs neutral at UBS

- Highwoods Properties (HIW) cut to hold vs buy at Jefferies

- JDS Uniphase (JDSU) raised to buy vs neutral at UBS

- Macerich (MAC) cut to neutral vs buy at UBS

- Tanger Factory (SKT) raised to buy vs neutral at UBS

- Tesoro (TSO) raised to buy at BofA

- Tetra Tech (TTI) rated new at Roth, PT $35

- Vail Resorts (MTN) cut to market perform at Wells Fargo

- Vertex Pharmaceuticals (VRTX) cut to outperform at RBC Capital

- Vulcan Materials (VMC) raised to outperform at RBC Capital

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

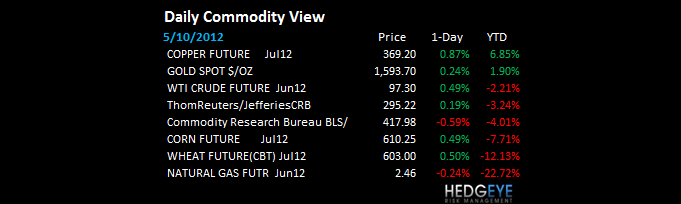

- Oil Snaps Longest Decline Since 2010 as U.S. Jobless Claims Fall

- Copper Rises as Chinese Trade Figures Spur Stimulus Speculation

- U.S. Soy Reserves May Fall 31% Before 2013 Harvest, USDA Says

- Brazil’s $2 Billion Sugar-Cane Revival Plan Fails: Commodities

- U.S. Corn Reserves May Double on Record Crops, USDA Says

- Soybeans Climb on Stockpile Speculation; Corn, Wheat Advance

- Gold Declines for Fourth Day in New York as Dollar Strengthens

- Cocoa Falls as Rain May Help Crop in Ivory Coast; Coffee Gains

- Cotton Drops After Government Report Shows Bigger U.S. Harvest

- Aluminum Buyers in Japan to Pay Record Fee as Supply Drops

- Cosan’s $2.4 Billion Acquisition Spree Hurts Debt: Brazil Credit

- London Oil Trades Beat New York for First Time: Chart of the Day

- Cooking-Oil Imports by India Seen Advancing for Third Month

- Florida Orange-Crop Estimate Little Changed, USDA Report Says

- Arch Coal Lures Lenders With Coal in Ground: Corporate Finance

- U.S. 2013 Wheat Stockpiles Seen Falling on Increased Exports

- U.S. Cotton Crop Will Climb 9.2% as Harvested Area Expands

CURRENCIES

US DOLLAR – forget Greece, get the US Dollar right and you’ll get a lot of other things right. US Dollar index up for 6 consecutive days and US Stocks down for 6 consecutive days – the USD Correlation Risk is screaming at -0.90 USD vs SPX right now and that’s why Gold and Oil refuse to bounce too. Correlation Risk isn’t perpetual, but when in the soup, it matters.

<CHART5>

EUROPEAN MARKETS

FRANCE – so you’re saying socialism is a ‘buy on the news’, eh? Non, non, mes amis – France flashing another negative divergence this morning, leading losers in Europe at -0.6%, taking the CAC’s draw-down from the March top (when European and US Growth Slowing accelerated on the downside0 to -14%.

ASIAN MARKETS

CHINA – trade balance out last night just tells us more about what we already know – Growth Slowing in Asia marked the highs for both the Hang Seng and the Sensex all the way back in February. This is not new and it’s primarily why China continues to act pretty well on bad economic “news” (+0.1% overnight and +10% for 2012 YTD – my favorite Global Equity market).

MIDDLE EAST

The Hedgeye Macro Team

Howard Penney

Managing Director