This note was originally published at 8am on April 26, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“The failure of the Knickerbocker Trust was just the beginning of a more general loss of confidence.”

-Jim Rickards

Anyone who has been in this business for more than the last 5 years knows what the biggest problem is for the US stock market – confidence. The People do not trust the financial system and all of its central planning puppetry. Therefore, The People are not giving the asset management community the number one thing they want – fund flows.

No Confidence. No Flows. No Volume.

That’s not new this morning. Neither is the world’s reaction to the US Federal Reserve’s un-elected Central Planner in Chief’s Policy to debauch the US Dollar in a repeated, but fleeting, attempt to inflate stock and commodity prices.

Sure, the price of Oil and Gold are up on the Dollar Down move. But they are up less than they were on Bernanke’s moves to Qe1, Qe2, and Qe3 (Bernanke’s latest war on the American Consumer (and Saver), pushing 0% interest rates on fixed income savings accounts to 2014 was a hybrid Qe3). We don’t think he has an iQe4 upgrade in his bailout bag during the General Election debate.

The reason why I used another one of Jim Rickards’ quotes (page 49 of Currency Wars) this morning is that it’s a critical one to consider in terms of why the US Federal Reserve Act of 1913 was established in the first place.

I’ll let you read Rickards book to form your own opinion on this, but the upshot of the problem was that NYC bankers, traders, etc. have always had the same problem – at a point, they take on too much risk with other people’s money, and they blow up.

In any other business, you’d be accountable for those losses and your business would go away. Post the 1907 Crisis, when banks like Knickerbocker literally blew up, banking and capital markets related companies have worked very hard at making sure that they have an un-elected man at the Fed that they can both appoint and politicize for their own compensation purposes.

The Fed was created to bailout banks, not American consumers.

Back to the Global Macro Grind…

While it’s both shocking and sad (but expected), Ben Bernanke was able to get through an entire press conference yesterday without mentioning the words “US DOLLAR.” What might be an even more glaring national embarrassment was that not 1 American journalist asked him about it either.

For those of us who aren’t paid to be willfully blind, here’s how real-time market expectations work:

- The Fed’s Monetary Policy drives the direction of the US Dollar

- The US Dollar, since it’s the world’s reserve currency, drives real Dollar adjusted expectations in liquid asset prices

- The inflation or deflation of asset prices (commodities in particular) drives the slope of Global Consumption Growth

I have my B.A. in Keynesian Economics from Yale. I don’t need a Ph.d in that dogma to explain to me how obvious the relationship is between the US Dollar and its purchasing power. Try it with your own money at home – you’ll get the point.

Despite Spain crashing again (Spanish stocks down -22% since February), even the Euro is strong versus the US Dollar this morning. The #1 Most Read Headline on Bloomberg: “Bernanke Prepared To Do More.” And the US Dollar Index is down for the 6th out of the last 7 weeks.

Our models show that Global Consumption Growth has never NOT slowed with oil above $96/barrel. Pick your vintage, Brent or WTIC, last I checked nothing happened in Iran overnight either. Prices of $104 and $119 per barrel, respectively, don’t lie; politicians do.

Does money printing matter? Does the amount of Dollars (World Reserve Currency) matter relative to World Oil Reserves? Of course they do. In 1990 the ratio of US Money Supply (M3)/Proved Oil Reserves = 4.1x. Today, that ratio = 10.7x. Reversing this factor alone would get you $75-80 oil, and the 99% would love that.

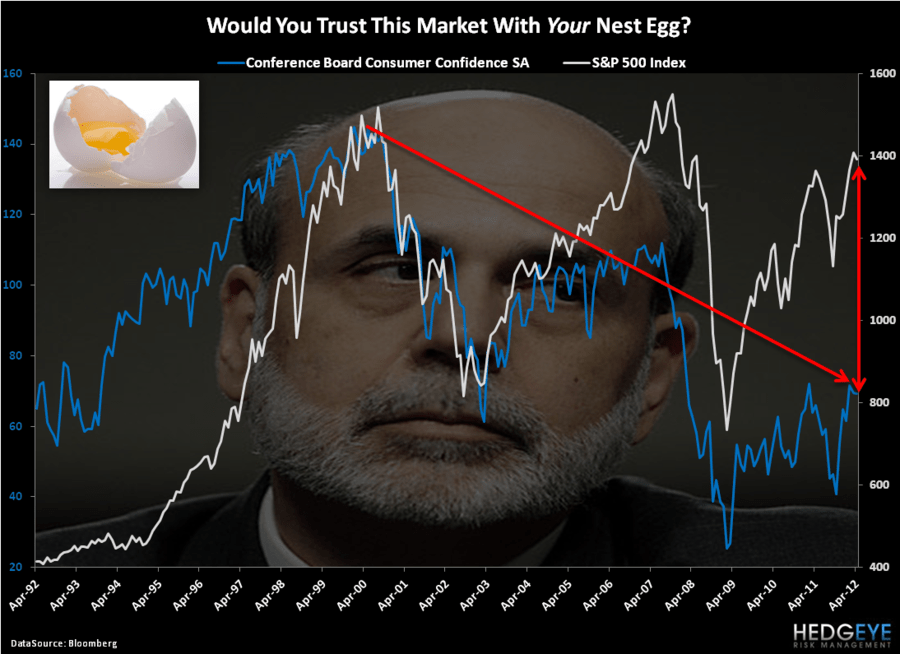

Got 1990s? Look at our Chart of The Day, then pull up a long-term chart of Oil – and you’ll see what I mean by Loss of Confidence:

- US Consumer Confidence tracked between 80 and 140 during the 1990s (this week it hit 69.2 for April)

- US Dollar Index Averaged $92.93 during the 1993-1999 expansion (avg GDP was 3.84%, so demand did what to oil?)

- Average price per barrel of WTIC Oil during 1993-1999 expansion = $18.63/barrel (not a typo)

It’s the US Dollar Stupid. That’s what real people use when they buy gas at the pump. So, if you’re part of a Keynesian crack house in Washington that’s addicted to devaluing the credibility and currency of the American people, shame on you.

If you want to try the “counter factual”, get your conflicted and compromised Fed friends to raise interest rates on Sunday night and tell me how many call options on oil you want to buy in front of that.

If you want to tell me Oil is up because of Iran, show me something going on in Iran. If you want to tell me Oil is up because global demand is up, show me where growth isn’t slowing.

Show me something. But don’t show me another complete embarrassment like yesterday’s Fed Press Conference. The concept of “price stability” (Fed mandate) does include the currency in which prices are paid. The Loss of Confidence in this country is rightly placed.

My immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, and the SP500 are now $1633-1655, $118.64-120.77, $78.97-79.44, and 1377-1394, respectively.

Best of luck out there today,

KM

Keith R. McCullough

Chief Executive Officer