Below are key European banking risk monitors, which are included as part of Josh Steiner and the Financial team's "Monday Morning Risk Monitor". If you'd like to receive the work of the Financials team or request a trial please email .

Key Takeaways:

* French Bank Swaps tightened slightly WoW going into Sunday's French presidential election, which saw Francois Hollande, the socialist party candidate, win the presidency. French sovereign swaps widened by 3% this morning compared to last Friday, highlighting an increased risk of default stemming from Hollande's likely rejection of certain austerity policies.

* Spanish Bank CDS tightened over the week while Spanish sovereign CDS widened.

If you’d like to discuss the implications of election results across Europe please let me know and we can set up a call.

Matthew Hedrick

Senior Analyst

(o)

-------------

European Financials CDS Monitor – Bank swaps were tighter in Europe last week for 29 of the 39 reference entities. The average tightening was 3.9% while the median tightening was 3.3%.

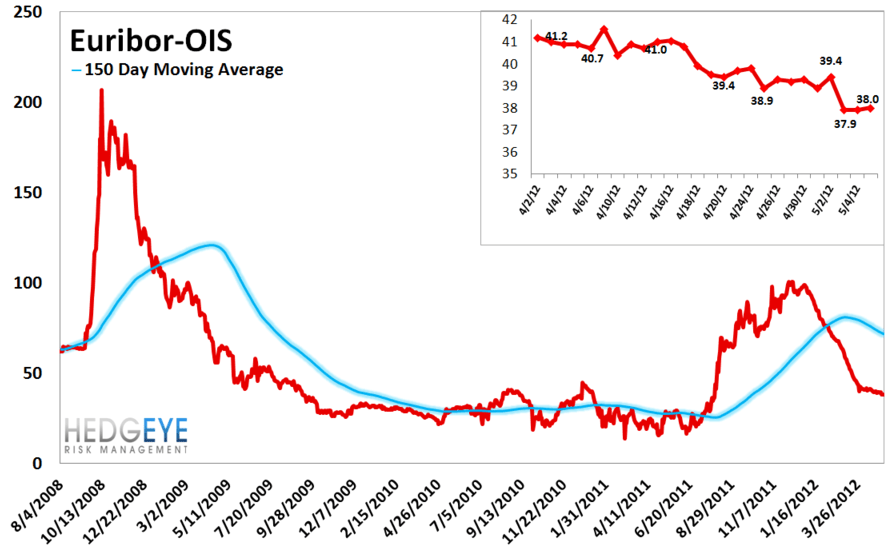

Euribor-OIS spread – The Euribor-OIS spread (the difference between the euro interbank lending rate and overnight indexed swaps) measures bank counterparty risk in the Eurozone. The OIS is analogous to the effective Fed Funds rate in the United States. Banks lending at the OIS do not swap principal, so counterparty risk in the OIS is minimal. By contrast, the Euribor rate is the rate offered for unsecured interbank lending. Thus, the spread between the two isolates counterparty risk. The Euribor-OIS spread tightened by 1 bps this morning over last Monday to 38 bps. We have noted previously that the correlation between Euribor-OIS and other risk measures (such as bank CDS or even bank stock prices) was very tight in the fall, but has disintegrated since mid-March. Thus, at the moment, we are not focused on Euribor-OIS as a key risk indicator.

ECB Liquidity Recourse to the Deposit Facility – The ECB Liquidity Recourse to the Deposit Facility measures banks’ overnight deposits with the ECB. Taken in conjunction with excess reserves, the ECB deposit facility measures excess liquidity in the Euro banking system. An increase in this metric shows that banks are borrowing from the ECB. In other words, the deposit facility measures one element of the ECB response to the crisis. The latest overnight reading is €801.49B.

Security Market Program – For an eighth straight week the ECB's secondary sovereign bond purchasing program, the Securities Market Program (SMP), purchased no sovereign paper for the latest week ended 5/4, to take the total program to €214 Billion.