This note was originally published at 8am on April 23, 2012. INVESTOR and RISK MANAGER SUBSCRIBERS have access to the EARLY LOOK (published by 8am every trading day) and PORTFOLIO IDEAS in real-time.

“Currency devaluation as a path to increased exports is not a simple matter.”

-Jim Rickards, Currency Wars

My week of family vacation would not have been complete without thinking about Keynesians. Sadly, from the gas pumps in Fort Myers, Florida to those in New Haven, CT, centrally planned Policies To Inflate are now part of the cost of everyday American life.

If you didn’t know that the world’s markets are globally interconnected, you might actually believe the Academic Dogma that a “cheap currency” is going to provide you the yellow brick road to Export prosperity. If you’ve analyzed the last 5 years of US Export versus US Consumption growth data, you probably think otherwise. America is a Consumption economy. Period.

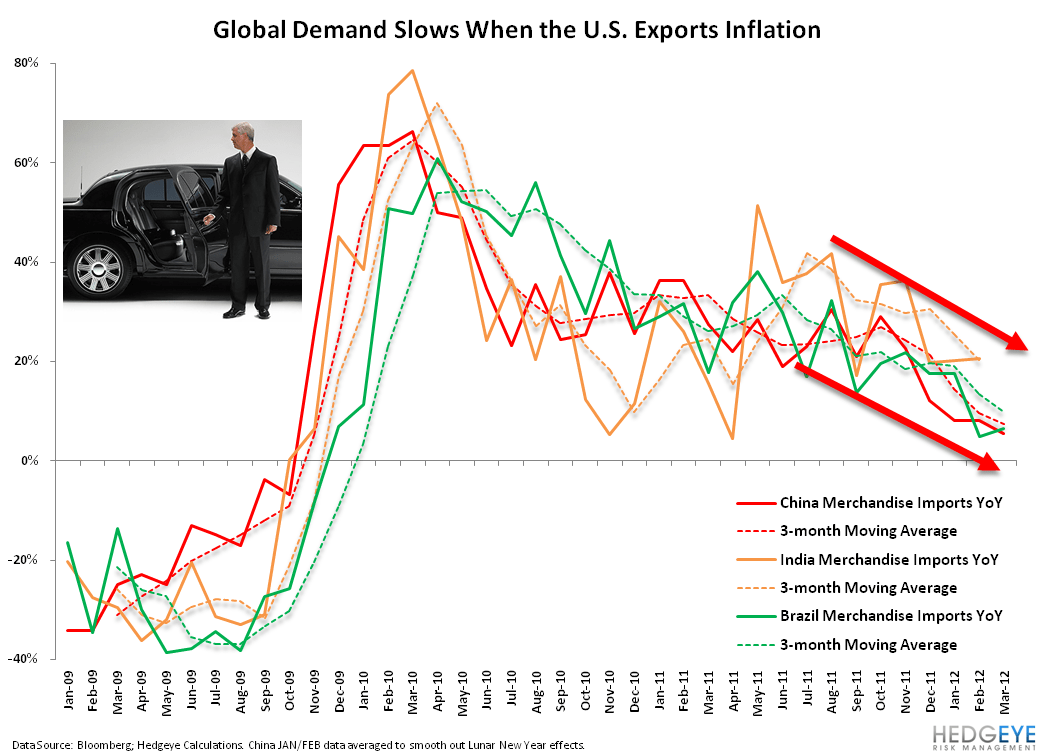

Debauching the US Dollar to all-time lows into the Spring of both 2008 and 2011 inspired bouts of global food and energy inflation like the world has never seen. With sovereign debt levels having crossed the Rubicon (structurally impairing long-term growth), Ben Bernanke had no business imposing another inflation policy on January 25th, 2012. Growth started slowing in February.

Back to the Global Macro Grind…

Growth Slowing in February? Yes, most major Asian and European stock markets stopped going up in February (Hong Kong, India, Spain, etc). This morning’s abruptly bearish reaction in global equity markets is simply a function of consensus catching up to where we’ve been. This isn’t our first rodeo calling for a sequential slowdown in growth. It won’t be our last.

What would change my view? I’ll give a free tank of natural gas to the first best guess.

Strong Dollar is the only way out. The best way to achieve that is to get these un-elected Keynesian policy makers out of the way.

A Strong Dollar will:

A) Deflate The Inflation

B) Strengthen (inflation adjusted) Consumption Growth

That’s the 71% of the US Economy that matters, not Exports.

Not seeing US Exports work drives the Keynesians right batty. It should - look at the US Export contribution to US GDP for the last 3 quarters:

- Q2 2011 = 0.48%

- Q3 2011 = 0.64%

- Q4 2011 = 0.37%

Oh, and by the way, you have to net out Imports from Exports to get to US GDP (calculating GDP = C + I + G + (EX-IM)), so Exports aren’t doing anything for US Growth where it matters most, on the margin.

The biggest concern that Keynesian politicians from Nixon/Carter to Bush/Obama have had is seeing the stock market go down. During periods of economic stagflation, stock markets get addicted to inflation inasmuch as the politicians do. If you Deflate The Inflation, stocks and commodities fall. So, in the short-term, they’re right.

But what’s right for the long-term prosperity of a country’s economy, attempting to centrally plan stock and commodity prices, or maintain price “stability” and “full” employment?

This is why The People are so upset. This is why US Equities in particular have zero inflows. The People don’t trust this game of gaming policy anymore – and they shouldn’t.

This morning’s Global Macro “news” is laden with stagflation – unless we see WTIC Oil prices snap and stay below $96/barrel, that’s just the way it’s going to be. Global Growth has never NOT slowed with Oil prices at these levels. Never is a long time.

Rather than have some Keynesian Economist who takes car service or a NYC cab to work tell you to put some natty gas in your truck and like it, look at what the rest of the world is reporting this morning:

- French Services PMI slows, big time, to 46.4 in April versus 50.1 in March

- Italian Consumer Confidence hits an all-time lows (all-time is a long time)

- Singapore Consumer Price Inflation for March accelerated to 5.2% versus 4.6% in February

That last data point is stale news now (March), and should start to ease in April/May if we see a continued Deflation of The Inflation. That’s the best news I can tell you this morning. But, like it was during the Q1 to Q3 stock market draw-downs of 2008, 2010, and 2011, this will be a process, not a point. Global Consumption doesn’t turn on a futures broker’s dime.

In the meantime, we’ll be using the same research and risk management process to monitor changes on the margin. While it’s alarming that Old Wall Street has not changed what it is that they do in the last 5 years, we don’t want to interrupt them as they continue to make the same mistakes, confusing short-term stock and commodity market inflations with real growth.

Our immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, and the SP500 are now $1623-1655, $116.95-119.41, $79.11-79.54, and 1356-1394, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer