“For they have sown the wind, and they shall reap the whirlwind.”

-Hosea 8:7

It’s windy out there this morning. But, then again, if you look back at where Global Stock and Commodity markets all peaked in 2012, it’s been windy since March. Today is not a day to freak-out. It’s just another day to price in what’s been happening.

The tail ends of this morning’s Global Macro meltdown will have a lot more to do with Global Growth Slowing and hedge funds caught off-sides long oil than it does France. Friday’s US Employment report was a mess.

The aforementioned quote came from Seth Klarman’s year-end 2011 letter ($22B hedge fund, The Baupost Group). We were obviously not alone in realizing that crossing the Rubicon of sovereign deficit and debt ratios would structurally impair Global Growth. Klarman, Einhorn, Dalio – these are the new leaders of Wall Street 2.0 – they all nailed Growth Slowing too.

Back to the Global Macro Grind…

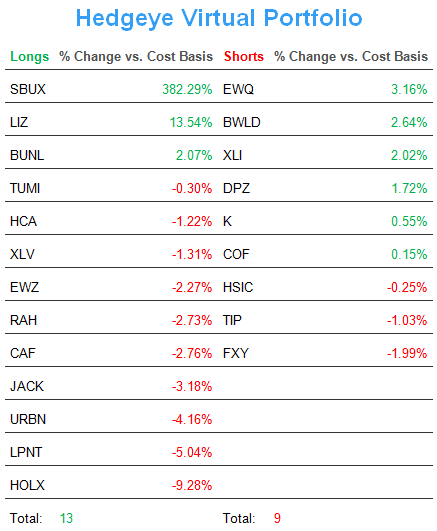

If you weren’t long US stocks or commodities last week, you probably had a very good week. Everything is relative while you are watching the whirlwind, I suppose. Our allocation to Commodities in the Hedgeye Asset Allocation Model remains 0%.

As Growth Slows and hopes for an iQe4 upgrade abate, we think the US Dollar stops going down and that, in turn, will provide a much needed break for American and Global Consumers of food and energy alike. We call it Deflating The Inflation.

Now, to be clear, this was only the 2ndweek of the last 8 where the US Dollar didn’t drop. And, as long as we have Ben Bernanke promising Qe as the elixir of a centrally planned life, America’s currency will continue to have headwinds. That all said, bullish is as bullish does, and the US Dollar has been up for 4 consecutive days. That’s a good thing.

Dollar up (in the immediate-term) means most things stocks and commodities go down. We call it the Correlation Risk. It’s what most perma-bulls got addicted to at the Q1 tops of 2008, 2010, 2011, and now, evidently, 2012. When the Dollar Debauchery stops, beta chasing anything inflation stops. Inflation and Growth are not the same thing.

Lets score that statement in real-time. With the US Dollar Index up +1.0% last week, here’s what everything else did:

- US STOCKS: SP500 -2.4%, Nasdaq -3.7%, Russell2000 -4.1%

- COMMODITIES: CRB Index -2.6, WTIC Oil -6.1%, Copper -2.6%

- BONDS: both German Bunds and US Treasuries hit YTD highs last week (UST 10yr = 1.83% today)

Another way to look at how perverse Old Wall Street has become when begging for Bernanke’s Policies To Inflate is that the US Dollar Index has developed an immediate-term positive correlation to US Equity Volatility of +0.93.

Think about that.

A credible currency costs this market a lot more than central planners think. With the USD up +1% last week, US Equity Volatility (VIX) spiked +17.8% week-over-week. That’s not “price stability”, Mr. Bernanke. That’s not good.

Volatility kills returns. Ask anyone who has successfully not lost money versus their 2007 high-water marks how hard it’s been to generate absolute returns and you’ll get the point.

One of the best strategies to not lose money has been not getting picked off ahead of any of these major stock and commodity market draw-downs (Q1 to Q3 SP500 draw-downs of -15-30% in 2008, 2010, 2011).

That’s why we’re so focused on the slope of growth as opposed to the level. As growth slows, “cheap” stocks get cheaper.

Valuation is not a catalyst until growth either slows at a slower rate or you have some sort of “event” whereby a cheap asset gets something like a management change or a takeout bid.

The best news I can give you this morning is that Deflating The Inflation at the pump has the highest probability of giving the US Consumer in particular a much needed tax break for Memorial Day Weekend.

I’m not suggesting our Growth Slowing call stops right here, right now. I’m just reminding you how our globally interconnected economic growth and inflation model works. Unlike most models that have failed you, ours goes both ways.

Long and short. All great teams play this game both ways (even when it’s windy).

Immediate-term support and resistance ranges for Gold, Oil (Brent), US Dollar Index, French Stocks (CAC40), and the SP500 are now $1, $112.45-118.18, $79.34-79.81, 3107-3279, and 1, respectively.

Best of luck out there this week,

KM

Keith R. McCullough

Chief Executive Officer