TODAY’S S&P 500 SET-UP – May 7, 2012

As we look at today’s set up for the S&P 500, the range is 25 points or -0.37% downside to 1364 and 1.45% upside to 1389.

SECTOR AND GLOBAL PERFORMANCE

EQUITY SENTIMENT:

- ADVANCE/DECLINE LINE: on 5/04 NYSE -1545

- Down from the prior day’s trading of -1194

- VOLUME: on 5/04 NYSE 825.24

- Decrease versus prior day’s trading of -2.24%

- VIX: as of 5/04 was at 19.16

- Increase versus most recent day’s trading of 9.11%

- Year-to-date decrease of -18.12%

- SPX PUT/CALL RATIO: as of 05/04 closed at 1.42

- Down from the day prior at 1.57

CREDIT/ECONOMIC MARKET LOOK:

- TED SPREAD: as of this morning 40

- 3-MONTH T-BILL YIELD: as of this morning 0.08%

- 10-Year: as of this morning 1.85

- Decrease from prior day’s trading at 1.88

- YIELD CURVE: as of this morning 1.60

- Down from prior day’s trading of 1.63

MACRO DATA POINTS (Bloomberg Estimates):

- 11:30am: U.S. to sell $30b 3-mo, $28b 6-mo bills

- 3pm: Consumer Credit, Mar., est. $9.75b (prior $8.735b)

- 7:15pm: Fed’s Lacker speaks in Greensboro, North Carolina

GOVERNMENT:

- President Obama officially started his re-election bid yesterday in the swing states of Ohio and Virginia

- Presidential nominee Mitt Romney campaigns in Cleveland

- House, Senate in session:

- House Budget Committee holds markup of sequester legislation. 2 p.m.

WHAT TO WATCH:

- Treasury Department to sell $5b of AIG stock at $30.5-shr

- Yahoo under pressure from Third Point to dismiss CEO

- Facebook gets first buy recommendation from Wedbush Securities

- Microsoft to claim Motorola is unfairly demanding $4b/year in patent royalties in federal court in Seattle today

- Avengers has record $200.3m in opening-wknd ticket sales

- Voters in France, Greece challenge austerity plans

- Falcone’s LightSquared gets another week from creditors

- Micron to invest 300b yen in Japan’s Elpida, Nikkei says

- Buffett says he’s focusing more on Asia to boost sales

- MLM blocked for 4 months from making hostile bid for rival Vulcan by judge ruling

- Preview of week’s U.S. economic reports

EARNINGS:

- Cognizant Technology Solutions (CTSH) 6 a.m., $0.79

- Dish Network (DISH) 6 a.m., $0.70

- EchoStar (SATS) 6 a.m., $0.02

- Towers Watson & Co (TW) 6 a.m., $1.35

- Cinemark Holdings (CNK) 6:36 a.m., $0.35

- Frontier Communications (FTR) 7 a.m., $0.06

- HollyFrontier (HFC) 7 a.m., $1.21

- Tyson Foods (TSN) 7:30 a.m., $0.39

- Louisiana-Pacific (LPX) 8 a.m., $(0.15)

- Sysco (SYY) 8 a.m., $0.43

- Coeur d’Alene Mines (CDE) 8 a.m., $0.43

- Dendreon (DNDN) 4 p.m., $(0.64)

- Rackspace Hosting (RAX) 4 p.m., $0.17

- Wesco Aircraft Holdings (WAIR) 4 p.m., $0.26

- Electronic Arts (EA) 4:01 p.m., $0.16

- Pitney Bowes (PBI) 4:01 p.m., $0.50

- Vivus (VVUS) 4:01 p.m., $(0.13)

- Clean Energy Fuels (CLNE) 4:05 p.m., $(0.18)

- ProAssurance (PRA) 4:05 p.m., $1.41

- Wynn Resorts (WYNN) 4:05 p.m., $1.41

- Plains All American Pipeline (PAA) 4:06 p.m., $1.51

- Dun & Bradstreet /The (DNB) 4:14 p.m., $1.32

- Avis Budget Group (CAR) 4:15 p.m., $(0.01)

- Hillenbrand (HI) 4:20 p.m., $0.50

- Federal Realty Investment Trust (FRT) 4:30 p.m., $1.02

- Vornado Realty Trust (VNO) 4:55 p.m., $1.77

- Uranium One (UUU CN) 5:01 p.m., $0.02

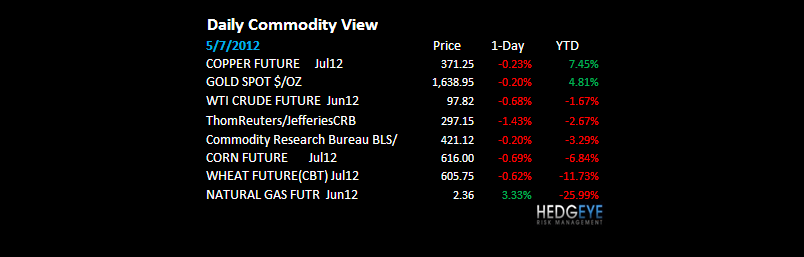

COMMODITY/GROWTH EXPECTATION (HEADLINES FROM BLOOMBERG)

- Hedge Funds Bet Wrong Before Biggest Slump in 2012: Commodities

- Copper Declines on French Election Outcome, U.S. Payroll Figures

- Malaysian Palm-Oil Output Probably Rose Most in Seven Months

- Commodities Close to Erasing 2012’s Gains on Europe, U.S. Data

- Corn Buying by China Seen Rising 35% on Chicken, Pork Demand

- Soybeans Decline on Forecast U.S. Farmers May Expand Planting

- Gold Imports by China From Hong Kong Post Increase in March

- China Needs U.S. Corn to Meet Rising Shortage, Shanghai JC Says

- Dalian Commodity Exchange Starts Options Trading Simulation

- Gold Declines as French, Greek Election Results Weaken the Euro

- Record Gas Use by U.S. Utilities Fails to Drive Up Price: Energy

- Oil Slumps to Four-Month Low on European Elections, U.S. Jobs

- NYSE Euronext Said Willing to Maintain LME Ring in Takeover Bid

- UN Sees Risk of Unrest From Food Costs Above 10-Year Average

- Malaysia Seen Countering Indonesia’s Palm-Oil Export Tax Reform

- South African Gold Mine Deaths Fall to a Record Low in April

CURRENCIES

US DOLLAR – get the USD and the slope of US Growth (slowing) right, and you’ll get a lot of other things right. USD up for the 4th consecutive day on Friday and the SP500 fell for its 3rd consecutive day. The immediate-term Correlation Risk to Strong Dollar vs SPX remains north of -0.8, so that has left a mark. Ultimately its take down oil prices, which is bullish for Consumers, globally.

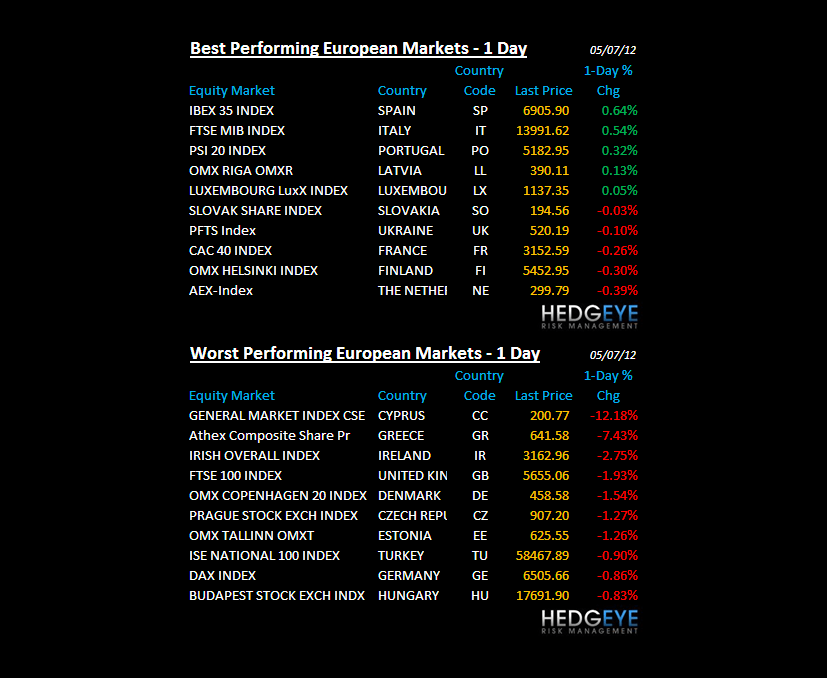

EUROPEAN MARKETS

FRANCE – no need for a consensus check here; France down another -1.3% this morning isn’t as much the story as the CAC being down -13% now from its YTD high on March 16th. Mean reversion matters, and now you’re seeing Spain, France, and Greece drag German stocks down with them (DAX down -10% from the same March 16th high; Spain and Greece crashing, again).

ASIAN MARKETS

JAPAN – Japanese stocks continue to get rocked, down hard last night (-2.8%) and down for the 16th trading day out of the last 21. The interconnected risk associated with Japan’s fiscal/debt crisis remains well under the consensus radar.

MIDDLE EAST

The Hedgeye Macro Team