“Sometimes I am two people. Johnny is the nice one. Cash causes all the trouble. They fight.”

-Johnny Cash

Maybe an educated Ivy League man like myself shouldn’t admit it, but I’m a fan of Johnny Cash. But to be fair, even if he isn’t representative of elite American culture, Cash probably represents the contradictions of American life as much as any entertainer of the 20thcentury.

On one hand, he was certainly well known for his sins and bouts with alcohol. On the other hand, he was a devout Christian who served his religion in many positive ways. Perhaps the most positive way was in his willingness to give free concerts inside prisons. The most famous of which was his performance at Folsom Prison in California from which the namesake song Folsom Prison Blues was produced.

In many ways, the contradictory nature of a personality like Johnny Cash (incidentally that was his birth name) very much represents the nature of the current global economy and, as a derivative, the global equity markets.

In Europe the key upcoming catalysts on the political calendar are the elections. The European elections also represent the current contradictory nature of popular sentiment in Europe. France, in particular, typifies this notion. In France, both the extreme left and the extreme right gained substantial ground in the first round of elections. Ultimately, though, it does look like the extreme left, the Socialists, will prevail and that Francois Hollande will succeed Nicolas Sarkozy as the next President of France.

The outcome of this election is meaningful and, in particular, will influence relations between Germany and France, two of the key decision makers in the European Union. As well, make no mistake about it, a shift to the left in Europe will have implications for European growth and equities. This is a point highlighted in the Chart of the Day today and an issue to keep front and center related to your European exposure. That is, even as French equities are broken on all of our durations, they are still well above the lows reached in December of 2011.

Even if the results of French elections appear certain to some, the Greek elections appear to be much less certain. Due to Greek electoral laws, no polls have been published since April 20th, but the most recent information from our contacts on the ground in Europe suggests that a majority between Pasok and New Democracy is increasingly unlikely. This potentially puts the bailout package at risk and implies that Greek elections may be called again as early as this fall.

In the United States, the key upcoming catalyst is the labor report which is out this morning. It is likely no surprise that Hedgeye is expecting a number that is more bearish than the expected 160,000 additions to non-farm payrolls. As I wrote in a note yesterday:

- Our Financials Team noted this morning that initial claims over the past few weeks have been coming in even worse than they would have suspected, even as last week’s claim, as reported this morning, fell 23K to 365K.

- The recent Challenger job report appears to support our view that the job market may decelerate. Specifically, planned job cuts increased by 7.1% from March to April and 11.2% on year-over-year basis.

As always though, trying to front-run government statistics is a fool’s errand; rather, you should just be ready to embrace the uncertainty that will result after the labor report this morning.

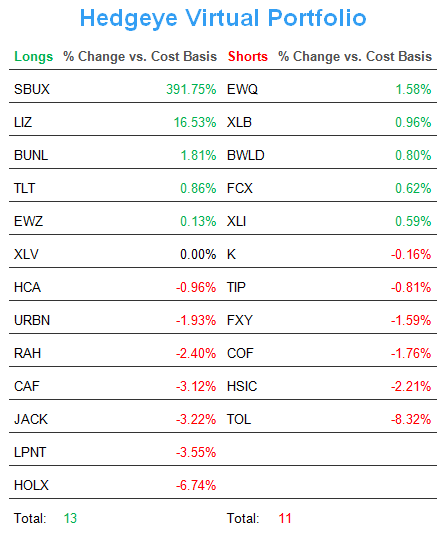

To that end, I wanted to highlight a couple of recent additions to the Hedgeye Virtual Portfolio on the global macro front:

1. Shorted French equities via the etf EWQ on May 1st– Our track record shorting France has been solid over the last two years as we have made money all ten times that we have shorted French equities. With the upcoming shift to the left in France’s economy, we obviously don’t think this time will be different.

2. Bought the U.S. healthcare sector via the etf XLV on May 3rd– On a basic level, the U.S. economy obviously looks pretty compelling vis-à-vis Europe, but as well we think there are some interesting potentially positive drivers in the healthcare sector. To that end, our healthcare team led by Tom Tobin is hosting a call on physician utilization next Friday. I’d recommend contacting our sales team at to get access to the call.

3. Bought Brazilian equities via the etf EWZ on May 3rd– Just when everyone thought Hedgeye was bearish on all things emerging markets, we are getting long of Brazil. A key driver of this position is that we expect commodity prices to decline. As an example Brent oil is bearish on TRADE and TREND durations. Declining commodity inflation is positive for emerging growth economies like China and Brazil.

One of my favorite Johnny Cash songs is The Highwaymen and in particular this excerpt:

“I was a sailor. I was born upon the tide

And with the sea I did abide.

I sailed a schooner round the Horn to Mexico

I went aloft and furled the mainsail in a blow

And when the yards broke off they said that I got killed

But I am living still.”

As it relates to being a stock market operator staying alive to trade another day is, figuratively, likely some of the best risk management you can heed.

Keep your head up and stick on the ice,

Daryl G. Jones

Director of Research